Short stay visa insurance is a mandatory requirement for many countries when you apply for a tourist or short-term visa. Without proof of valid travel health insurance, your visa application may be denied. Understanding the exact coverage, duration, and provider standards ensures a smooth entry and peace of mind during your trip.

Key Takeaways

- Mandatory Coverage: Most countries require short stay visa applicants to show proof of comprehensive travel insurance that covers medical emergencies, hospitalization, and repatriation.

- Minimum Coverage Amounts: Requirements vary—some countries demand at least €30,000 in medical coverage, while others may require up to €100,000 or more depending on the destination and visa type.

- Validity Period: Your insurance policy must be valid for the entire duration of your intended stay, and sometimes for an additional 30 days after departure.

- Approved Providers: Not all insurance companies are accepted. Some countries only recognize policies from specific providers or those meeting certain EU standards.

- Documentation Matters: You’ll need a formal insurance certificate or letter to submit with your visa application—digital copies are usually acceptable but must be clear and legible.

- Common Mistakes to Avoid: Don’t assume your home country’s travel insurance will work abroad. Always verify the policy meets the host country’s exact requirements.

- Cost vs. Coverage: While cheap policies may seem appealing, they often lack critical coverage like emergency dental, trip cancellation, or evacuation—features required by many visa authorities.

📑 Table of Contents

Introduction: Why Short Stay Visa Insurance Matters

Planning a trip abroad is exciting—whether you’re visiting family, exploring a new city, or diving into a cultural adventure. But before you pack your bags, there’s one crucial step many travelers overlook: securing the right travel insurance to meet visa requirements. For short stay visas—such as those for tourism, business visits, or short-term study—many countries make travel health insurance a non-negotiable part of the application process.

Why? Because governments want to protect themselves from the financial burden of medical emergencies, hospitalizations, or unexpected evacuations that could occur during your stay. Without proof of adequate coverage, your visa application can be rejected outright. This isn’t just a bureaucratic formality—it’s a real safeguard for both you and the country you’re visiting.

In this article, we’ll walk you through everything you need to know about short stay visa insurance requirements. From understanding what coverage is mandatory to choosing the right policy and avoiding common pitfalls, we’ve got you covered. Whether you’re heading to Europe, Asia, or beyond, knowing the rules ahead of time will save you time, stress, and potentially thousands of dollars in the long run.

Understanding Short Stay Visa Insurance

Visual guide about Short Stay Visa Insurance Requirements

Image source: img.yumpu.com

What Is Short Stay Visa Insurance?

Short stay visa insurance, also known as travel medical insurance or visitor health insurance, is a type of policy designed specifically for tourists, business travelers, and short-term visitors. Unlike long-term travel insurance or international health plans, these policies are tailored to cover brief trips—usually up to 90 days, though some allow extensions.

These policies typically include:

– Emergency medical expenses

– Hospitalization and surgery

– Repatriation or medical evacuation

– Coverage for pre-existing conditions (in some cases)

– Accidental death and dismemberment

The key thing to remember is that short stay visa insurance is not the same as your regular health insurance. While your home plan might offer limited coverage abroad or none at all, visa-required insurance ensures you meet the host country’s legal standards.

Why Is It Required?

Countries require short stay visa insurance to reduce the risk of becoming a public charge. If you fall seriously ill or get into an accident while visiting, hospitals and emergency services can’t turn you away—but they also can’t bill your home country if you have no insurance. By mandating proof of coverage, governments ensure that visitors can access care without leaving taxpayers to foot the bill.

For example, if you’re injured in a car crash in France or suffer a heart attack in Japan, the local hospital will treat you immediately. But without proper insurance, you could end up with a bill in the hundreds of thousands—or even millions—of dollars. That’s why many countries, especially in Europe, Asia, and the Middle East, treat travel insurance as a visa condition.

Who Needs It?

Almost every traveler heading abroad for a short stay may need this type of insurance, including:

– Tourists visiting for leisure or sightseeing

– Business travelers attending meetings or conferences

– Students on short-term exchange programs

– Spouses or partners accompanying a visa holder

– Digital nomads on short-term work assignments

Even if you’re from a country with strong healthcare, you still need this insurance. Domestic health systems don’t cover foreigners, and emergency care can be prohibitively expensive without insurance.

Key Requirements by Region

Visual guide about Short Stay Visa Insurance Requirements

Image source: campusfrance.org

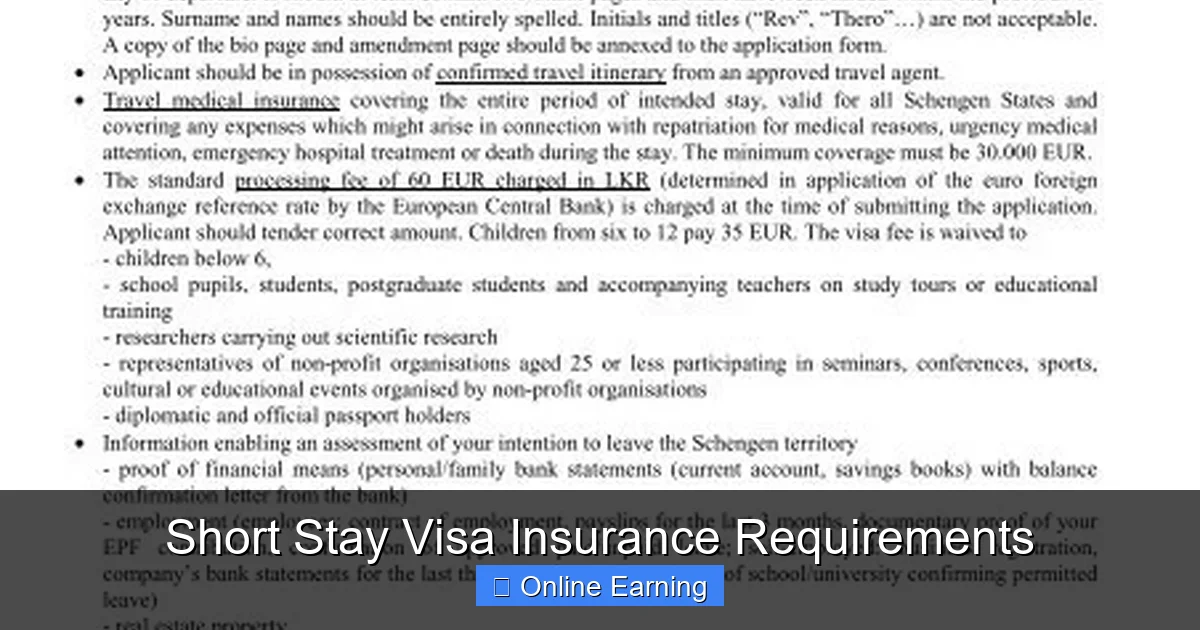

European Union (Schengen Visa)

If you’re applying for a Schengen visa to travel across Europe, you’ll need travel insurance that meets specific EU standards. The most important requirement is **minimum coverage of €30,000** for medical emergencies, including emergency treatment, hospitalization, and repatriation.

Your policy must:

– Be valid for the entire duration of your stay

– Cover the entire Schengen Area

– Be issued by an EU-approved insurance company or one recognized under the Schengen Visa Code

– Include coverage for medical evacuation and repatriation

For example, if you’re visiting France, Germany, and Italy for two weeks, your insurance must cover all three countries and be active during those 14 days—plus, some embassies recommend extending coverage by 30 days post-trip for added security.

United Kingdom (Standard Visitor Visa)

While the UK is no longer part of the EU, it still requires visitors to have travel insurance. The standard visitor visa (for tourism, business, or family visits) mandates coverage for:

– Emergency medical treatment

– Repatriation

– Personal liability

There’s no fixed minimum amount, but it should be sufficient to cover a serious medical event. Most travel insurance providers offer policies starting at £1 million in coverage, which is more than enough. However, you’ll need to provide proof of insurance when applying.

Canada (Visitor Visa)

Canada requires short-term visitors to have medical coverage that applies within its borders. The policy must:

– Cover at least **CAD $50,000** for hospitalization and emergency treatment

– Be valid for the entire stay

– Include coverage for repatriation and emergency medical evacuation

Many Canadian consulates accept insurance from providers like Allianz, AXA, or World Nomads, but it’s best to check with your local embassy to confirm.

Australia (ETA and Visitor Visa)

Australia requires visitors to have travel insurance that covers:

– Emergency medical treatment

– Hospitalization

– Medical evacuation

There’s no official minimum amount, but most embassies recommend at least AUD $100,000 in coverage. Policies from providers like Allianz, IATI, or Cover-More are commonly accepted.

Japan (Tourist Visa)

Japan does not always require travel insurance for short-term tourists, but it’s strongly recommended—and some embassies may request proof during the visa application process. If required, the policy should cover:

– Emergency medical treatment

– Hospitalization

– Repatriation

Minimum coverage is typically around ¥5 million (about $35,000 USD), but it’s best to aim higher for peace of mind.

United States (B-2 Visa)

The U.S. does not legally require travel insurance for short-term visitors, but it’s highly advisable. While your home country’s health insurance may offer limited coverage, it often excludes emergency care in the U.S. Without insurance, a single ER visit can cost thousands of dollars.

Many travelers choose to buy short-term visitor insurance from providers like IMG or Seven Corners to meet this need. While not mandatory, having coverage can prevent financial disaster.

What to Look for in a Policy

Visual guide about Short Stay Visa Insurance Requirements

Image source: schengenvisa.ae

Essential Coverage Features

Not all short stay visa insurance policies are created equal. To meet visa requirements and protect yourself, look for these key features:

- Medical Emergency Coverage: This should include doctor visits, hospital stays, surgery, and prescription drugs. Make sure it covers both sudden illness and accidents.

- Repatriation and Evacuation: In case of serious injury or illness, you may need to be flown home or to a better-equipped medical facility. This is often the most expensive part of a claim.

- Pre-Existing Condition Waiver: Some policies allow coverage for pre-existing conditions if you purchase the policy within a certain time frame (usually 10–20 days) of your trip and meet other criteria.

- Trip Cancellation or Interruption: While not always required, this adds extra protection if your trip is canceled due to illness, natural disasters, or other unforeseen events.

- 24/7 Assistance: A helpline available around the clock can help you find doctors, arrange evacuations, or handle emergencies in another language.

Validity and Duration

Your policy must be active for the entire duration of your planned stay. For example, if you’re visiting Spain for 21 days, your insurance must be valid from your arrival date to your departure date. Some countries also require coverage for an additional 30 days after your trip ends—this is known as “return travel coverage” and ensures you’re protected if you need medical care after leaving.

When purchasing, double-check the “effective date” and “expiration date” on your certificate. Don’t assume the policy starts the day you book it—many providers require a waiting period.

Geographic Coverage

Make sure your policy covers the specific countries you’re visiting. Some plans are limited to certain regions or exclude high-risk areas. For instance, if you’re traveling from the U.S. to Europe, your policy should explicitly include the Schengen Area.

If you’re visiting multiple countries, confirm that your plan covers all of them. Don’t assume “international” means “everywhere”—some policies cap coverage at $50,000 or exclude certain nations.

Approved Insurance Providers

Not every insurer is accepted by visa authorities. Some countries only recognize policies from providers licensed in the EU or those meeting specific regulatory standards. For example:

– Schengen visa applicants may need insurance from an EU-based company

– Canadian visitors may prefer providers like Allianz or AXA

– Australian travelers often use Cover-More or IATI

Before purchasing, check the list of approved providers on your country’s embassy website or contact the consulate directly.

How to Apply for a Visa with Insurance

Step-by-Step Process

Applying for a visa with travel insurance is straightforward if you follow these steps:

- Gather Required Documents: This typically includes your passport, application form, photos, flight itinerary, accommodation proof, and financial documents.

- Purchase Insurance: Buy a policy that meets the host country’s requirements. Ensure it’s active for your entire stay.

- Obtain a Certificate: Most providers issue a digital insurance certificate or letter. Save this as a PDF and print a copy.

- Submit with Application: Attach the insurance certificate to your visa application. Some embassies require it to be submitted in person or via mail.

- Keep Copies: Carry both digital and printed copies of your insurance during your trip. Some countries may ask to see it at border control.

Common Mistakes to Avoid

- Buying Insurance Too Late: Some policies have a waiting period (e.g., 10 days) before coverage begins. Apply for insurance well before your trip.

- Assuming Home Insurance Covers You: Most domestic health plans offer limited or no coverage abroad. Always verify with your provider.

- Overlooking Policy Limits: A cheap policy with $10,000 in coverage won’t suffice for a major emergency. Aim for at least €30,000–€50,000.

- Not Checking Exclusions: Read the fine print. Many policies exclude high-risk activities like skiing, scuba diving, or adventure sports.

- Failing to Renew or Extend: If your trip is extended, update your insurance to avoid a coverage gap.

Tips for a Smooth Application

– Start your visa application early—don’t wait until the last minute.

– Contact the embassy or consulate to confirm their insurance requirements.

– Use a policy that offers instant digital delivery so you can print the certificate immediately.

– Keep your insurance provider’s contact details handy in case of emergencies.

Top Insurance Providers for Short Stay Visas

Allianz Global Assistance

Allianz is one of the most trusted names in travel insurance. Their visitor insurance plans are accepted by many countries, including Canada, the UK, and parts of Europe. They offer flexible coverage options and 24/7 multilingual support.

World Nomads

Popular among digital nomads and adventure travelers, World Nomads provides coverage for high-risk activities and is accepted by some embassies. Their policies are ideal for short-term trips and include emergency medical and evacuation coverage.

AXA Travel Insurance

AXA offers comprehensive visitor insurance with options for single-trip or multi-trip coverage. Their plans are widely accepted, especially in Canada and Europe, and include coverage for pre-existing conditions in some cases.

Seven Corners

Seven Corners specializes in visitor insurance and is known for its competitive pricing and global coverage. Their plans are accepted by many embassies and include emergency medical, evacuation, and repatriation benefits.

IMGs (International Medical Group)

IMGs offers flexible visitor insurance plans with options for long-term and short-term stays. Their policies are accepted in several countries and include coverage for pre-existing conditions with proper underwriting.

Cover-More (Australia)

If you’re heading to Australia, Cover-More is a top choice. Their visitor insurance is widely accepted and includes coverage for emergency medical treatment, hospitalization, and evacuation.

Conclusion: Don’t Risk It—Get the Right Insurance

Traveling abroad is a wonderful opportunity to explore new cultures, create lasting memories, and grow personally. But without the right short stay visa insurance, that dream trip could turn into a financial nightmare. From visa rejections to exorbitant medical bills, the risks are real—and the consequences can be devastating.

By understanding the requirements, choosing the right policy, and submitting the correct documentation, you can ensure a smooth application process and a worry-free journey. Remember, short stay visa insurance isn’t just a formality—it’s your safety net, your peace of mind, and your gateway to a protected adventure.

Take the time to research, compare providers, and read the fine print. Investing in the right insurance today could save you thousands tomorrow. So don’t skip this step—your health, your wallet, and your visa depend on it.

Frequently Asked Questions

Do I really need travel insurance for a short stay visa?

Yes, many countries require proof of travel insurance as a condition for issuing a short stay visa. Without it, your application may be denied. Always check the specific requirements for your destination.

What’s the minimum coverage amount needed?

Most countries require at least €30,000 in medical coverage. Some, like Canada, require up to CAD $50,000 or more. Always verify the exact amount with your embassy or consulate.

Can I use my regular health insurance for a visa?

Most domestic health plans offer limited or no coverage abroad. Even if they do cover international care, it often doesn’t meet visa requirements. It’s safer to purchase a dedicated short stay visa insurance policy.

How far in advance should I buy insurance?

It’s best to buy insurance as soon as you apply for your visa. Some policies have a waiting period (e.g., 10–20 days) before coverage begins, so don’t wait until the last minute.

Is insurance required for a U.S. B-2 visa?

The U.S. doesn’t legally require travel insurance, but it’s highly recommended. Without coverage, a single ER visit could cost thousands of dollars. Many travelers choose to buy visitor insurance for added protection.

Can I extend my insurance if I stay longer?

Yes, most providers allow you to extend your policy online. Contact your insurer as soon as you realize your trip will be extended to avoid a coverage gap.