Short-term health insurance offers a budget-friendly way to bridge coverage gaps when you’re between jobs or waiting for major medical insurance to kick in. While it’s not a long-term solution, it can provide essential protection during transitions. However, it lacks key benefits like pre-existing condition coverage and preventive care, so weigh the pros and cons carefully.

Key Takeaways

- Short-term plans are temporary: They typically last 3-12 months and are not intended to replace major medical insurance.

- Lower premiums: These plans cost significantly less than ACA-compliant plans, making them attractive for budget-conscious individuals.

- Limited benefits: Coverage is often restricted—no maternity care, mental health, or prescription drugs in many cases.

- No pre-existing condition coverage: If you have a medical history, you may be denied coverage or receive limited benefits.

- Ideal for specific situations: Great for young, healthy individuals between jobs or waiting for employer coverage.

- Not for everyone: If you need comprehensive care, short-term insurance may leave you exposed to high out-of-pocket costs.

- Check state regulations: Availability and rules vary by state—some have strict limits on short-term plans.

📑 Table of Contents

What Is Short-Term Health Insurance?

Imagine you’ve just left your job and are waiting for your new employer’s health plan to start. Or maybe you’re a recent graduate who hasn’t found full-time work yet and needs coverage while you search. In moments like these, short-term health insurance can seem like a quick and easy solution. But what exactly is it, and how does it work?

Short-term health insurance is a type of temporary health plan designed to provide coverage for a limited period—usually between 3 and 12 months, though some states allow up to 36 months. Unlike Affordable Care Act (ACA) marketplace plans, which must cover essential health benefits and protect against pre-existing conditions, short-term plans are not required to follow these rules. This flexibility makes them cheaper but also more limited in what they cover.

These plans are marketed as a way to fill coverage gaps. They’re not meant to replace long-term health insurance. Instead, they’re ideal for people who need a short-term safety net while transitioning between jobs, waiting for group coverage to begin, or living in a state where ACA plans aren’t available.

How Short-Term Plans Differ from Major Medical Insurance

The biggest difference between short-term health insurance and major medical plans lies in the level of protection. Major medical insurance, like those sold on the ACA marketplace, must cover ten essential health benefits. These include:

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Rehabilitative services

- Laboratory services

- Preventive care (like vaccinations and screenings)

- Pediatric care (including dental and vision for children)

Short-term plans, on the other hand, are not required to cover any of these. Many exclude coverage for pre-existing conditions, limit doctor visits, and don’t include prescription drug benefits. Some may not even cover hospital stays or emergency room visits beyond a certain dollar amount.

Another key difference is the underwriting process. When you apply for a short-term plan, the insurer can ask about your health history. If you have a condition like diabetes or high blood pressure, they may deny coverage or offer a plan with exclusions. In contrast, ACA plans cannot deny you coverage or charge more based on health status.

Who Should Consider Short-Term Health Insurance?

Visual guide about Short-term Health Insurance: Is It Worth It?

Image source: lh6.googleusercontent.com

Short-term health insurance isn’t for everyone. It’s best suited for specific situations where you need temporary coverage and can accept the trade-offs. Let’s break down who might benefit.

The Young and Healthy

If you’re in your 20s or early 30s and generally healthy, you might find short-term plans appealing. They’re often much cheaper than ACA plans—sometimes by 50% or more. For someone who rarely visits the doctor and doesn’t take prescription medications, the risk of needing expensive care is low. In that case, a short-term plan could be a smart way to save money while staying covered.

For example, Alex, a 28-year-old graphic designer, recently moved to a new state and didn’t qualify for the local ACA marketplace. He found a short-term plan for $85 a month. He knew it wouldn’t cover dental or vision, but he didn’t need those. He also didn’t have any chronic conditions. For him, the low cost and simplicity made sense.

Between Jobs or Waiting for Employer Coverage

This is one of the most common reasons people buy short-term insurance. If you’re unemployed and waiting for your new job to start, or you’re in between jobs, you might not want to go uninsured. Even a few months without coverage could leave you exposed if you get sick or injured.

Short-term plans can bridge that gap. As long as you understand the limits, they can give you peace of mind during a transition period. Just remember to enroll in a new plan before your short-term coverage ends—or risk a coverage gap.

Recent Graduates or Students

Many students lose coverage when they graduate or leave school. If you’re not yet employed full-time and can’t afford a full ACA plan, a short-term policy might help until you qualify for employer benefits.

Keep in mind, though—some short-term plans don’t cover mental health services, which can be important for college graduates dealing with stress, anxiety, or depression.

What About People with Pre-Existing Conditions?

Unfortunately, short-term health insurance is rarely a good fit for someone with a pre-existing condition. These plans can deny coverage based on your medical history, or they may exclude treatment for your condition.

For example, Sarah, a 45-year-old who had breast cancer five years ago, tried to apply for a short-term plan. The insurer reviewed her health history and declined her application because of her cancer history. She had no other options until she qualified for Medicaid.

If you have a chronic illness, it’s crucial to explore other options—like COBRA, Medicaid, or ACA plans with cost-sharing subsidies.

Pros and Cons of Short-Term Health Insurance

Visual guide about Short-term Health Insurance: Is It Worth It?

Image source: shorttermhealthinsurance.com

Like any insurance product, short-term health insurance has both advantages and disadvantages. Understanding both sides will help you decide if it’s worth it for your situation.

Pros: The Benefits

- Lower premiums: Short-term plans are often 30-60% cheaper than ACA plans. This makes them attractive for people on tight budgets.

- Quick approval: You can often apply and get approved in a few days, sometimes even the same day.

- Flexible terms: You can renew or extend your plan for up to 36 months in many states, giving you time to find a permanent solution.

- No open enrollment: Unlike ACA plans, you can enroll or renew anytime, making it easy to get coverage when you need it.

Cons: The Drawbacks

- Limited coverage: Many plans exclude hospital stays, maternity care, mental health, and prescription drugs.

- Pre-existing condition exclusions: Insurers can deny coverage or exclude treatment for known health issues.

- No guaranteed renewability: Insurers can cancel your plan at any time, even if you get sick.

- No subsidies: Short-term plans don’t qualify for premium tax credits or cost-sharing reductions.

- Not ACA-compliant: You can’t use short-term plans to meet the individual mandate (though the mandate is no longer enforced federally).

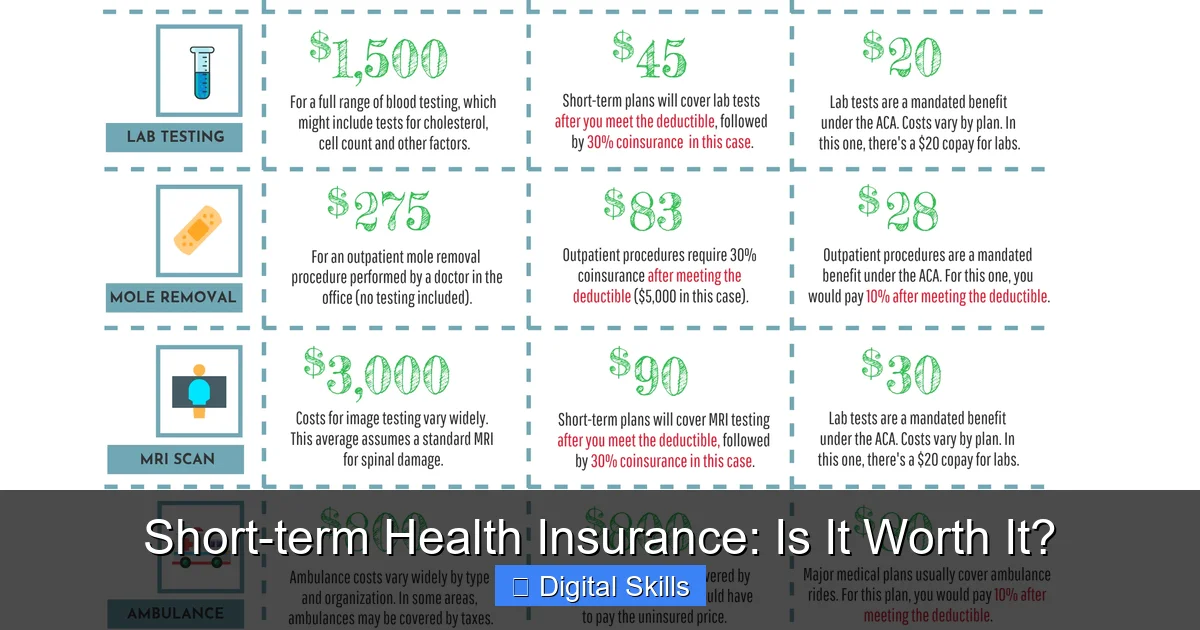

Real-World Example: The Cost Comparison

Let’s say you’re a 30-year-old non-smoker living in Texas. Here’s how premiums might compare:

- Short-term plan: $75–$120 per month

- ACA marketplace plan (Silver level): $250–$350 per month

- ACA plan with subsidy (based on income): $50–$100 per month

- Pre-existing condition clauses

- Exclusions for specific treatments (like maternity or mental health)

- Annual or lifetime maximums

- Waiting periods for coverage

At first glance, the short-term plan seems like a no-brainer. But consider this: if you need a $5,000 hospital stay and your short-term plan only covers 50% after a $1,000 deductible, you’d still owe $3,500 out of pocket. An ACA plan would cap your out-of-pocket costs at around $8,000—but many people qualify for subsidies that reduce that to under $2,000.

So while short-term plans save on premiums, they can lead to much higher costs if you need care.

How to Choose the Right Short-Term Plan

Visual guide about Short-term Health Insurance: Is It Worth It?

Image source: stat.joinditto.in

If you’ve decided a short-term plan might work for you, how do you pick the best one? Here are some practical tips.

Compare Coverage Limits

Look at the maximum benefit amount. Most short-term plans cap coverage between $1 million and $2 million. But some may have lower limits—like $500,000. If you’re young and healthy, a lower cap might be fine. But if you have family responsibilities, you might want more.

Also, check if the plan covers doctor visits, emergency care, and hospital stays. Some plans only cover a percentage of costs, leaving you with high out-of-pocket expenses.

Check the Network

Unlike ACA plans, which have broad provider networks, short-term plans often use narrow networks. This means you may not be able to see your regular doctor or go to a hospital you prefer.

Before enrolling, confirm that your preferred doctors and hospitals are in-network. You can usually find this information on the insurer’s website or by calling customer service.

Read the Fine Print

This is critical. Short-term plans are full of exclusions. Look for:

Don’t assume anything. If a benefit isn’t listed, it’s probably not covered.

Consider Your Health Needs

Ask yourself: Do I take regular medications? Do I have a chronic condition? Am I planning to start a family? If the answer is yes to any of these, a short-term plan might not be safe.

Instead, consider an ACA plan, especially if you qualify for subsidies. The extra cost could save you thousands in the long run.

Alternatives to Short-Term Health Insurance

Before committing to a short-term plan, explore other options. You might find something better suited to your needs.

COBRA Continuation Coverage

If you’ve recently left a job with health benefits, COBRA allows you to keep your current plan for up to 18 months. It’s expensive—you pay the full premium plus a 2% admin fee—but it offers full coverage.

COBRA is ideal if you have a pre-existing condition or need specific treatments. Just be aware that the cost can be overwhelming for someone on a tight budget.

Medicaid

If your income is low, you might qualify for Medicaid. It’s a government program that provides free or low-cost coverage to eligible individuals. Eligibility varies by state, but it’s worth checking.

For example, a single parent earning $25,000 a year might qualify for Medicaid in many states—far better than a short-term plan.

ACA Marketplace Plans

The ACA marketplace offers subsidized plans for people who don’t have employer coverage. You can shop for plans year-round if you qualify for a special enrollment period (like losing job-based coverage).

Even if you don’t qualify for subsidies, ACA plans offer more comprehensive coverage than short-term plans. They also protect you from high out-of-pocket costs.

Health Care Sharing Ministries

These are faith-based organizations where members share medical costs. They’re not insurance, but they can be cheaper than traditional plans.

However, they’re not regulated like insurance, and participation is based on religious beliefs. They may also exclude certain treatments or conditions.

Is Short-Term Health Insurance Worth It?

So, is short-term health insurance worth it? The answer depends on your situation.

For a young, healthy person between jobs who doesn’t need extensive medical care, it can be a smart, affordable choice. It’s quick, flexible, and saves money on premiums. Just be honest about your health needs and understand the limitations.

But for someone with chronic illness, taking medications, or planning for future health needs, short-term insurance is risky. The savings on premiums could be wiped out by high medical bills.

The bottom line: short-term health insurance is worth it if you’re in a temporary situation and can accept the trade-offs in coverage. But it’s not a substitute for comprehensive, long-term health insurance.

Always compare your options, read the fine print, and consider consulting a licensed insurance agent or benefits counselor. Your health is too important to leave to chance.

Frequently Asked Questions

Can I get short-term health insurance if I have a pre-existing condition?

Possibly, but not always. Insurers can deny coverage or exclude treatment for pre-existing conditions. If you have a chronic illness, consider COBRA, Medicaid, or ACA plans instead.

How long does short-term health insurance last?

Typically 3 to 12 months, but some states allow plans to last up to 36 months. You can often renew or extend your coverage during that period.

Do short-term plans cover prescription drugs?

Not always. Many short-term plans exclude prescription drug coverage. If you take medications regularly, make sure your plan includes pharmacy benefits.

Can I use short-term insurance to meet the individual mandate?

No. Short-term plans are not ACA-compliant and do not count toward the individual mandate. However, the federal mandate is no longer enforced.

Are short-term plans available in all states?

Yes, but rules vary. Some states have strict limits on how long plans can last or require additional benefits. Check your state’s regulations before enrolling.

What happens if I get sick and need treatment under a short-term plan?

Coverage depends on your plan’s terms. Some may cover emergency care but exclude hospital stays or pre-existing conditions. Out-of-pocket costs can be high if benefits are limited.