Choosing the best medical insurance plan can save you thousands while protecting your health and financial future. With so many options available, it’s easy to feel overwhelmed—but knowing what to look for makes all the difference. This guide walks you through the essentials, from understanding premiums and deductibles to evaluating network providers and coverage limits. Whether you’re self-employed, freelancing, or employed, the right plan gives you peace of mind and access to quality care when you need it most.

Key Takeaways

- Understand your healthcare needs: Consider your age, health history, family size, and how often you visit doctors when selecting a plan.

- Compare premiums, deductibles, and out-of-pocket costs: Lower premiums often mean higher out-of-pocket expenses—find the balance that fits your budget.

- Check the provider network: Make sure your preferred doctors and hospitals are in-network to avoid surprise bills.

- Review prescription drug coverage: If you take regular medications, ensure they’re covered under the plan’s formulary.

- Look for additional benefits: Some plans offer wellness programs, telehealth, or mental health services—great extras worth considering.

- Read the fine print: Understand exclusions, waiting periods, and claim processes before enrolling.

- Consider future flexibility: If you’re freelancing, choose a plan that allows portability or works across state lines.

📑 Table of Contents

- How to Choose the Best Medical Insurance Plan

- Understanding the Basics: What Is Medical Insurance?

- Types of Medical Insurance Plans

- How to Evaluate Your Healthcare Needs

- Comparing Costs: Premiums vs. Out-of-Pocket Expenses

- Network and Provider Considerations

- Additional Benefits and Features

- How to Enroll and Avoid Common Mistakes

- Conclusion: Your Health, Your Choice

How to Choose the Best Medical Insurance Plan

Let’s be honest—health insurance sounds important, but honestly, most people don’t know where to start. You’ve probably heard terms like “premium,” “deductible,” and “copay,” but what do they really mean? And how do you pick a plan that doesn’t leave you scrambling when you actually need care? Whether you’re a freelancer juggling multiple clients, a recent graduate starting your career, or someone looking to switch plans, choosing the right medical insurance can feel like navigating a maze. But don’t worry—you’re not alone, and it doesn’t have to be overwhelming.

The truth is, the best medical insurance plan isn’t the most expensive or the cheapest—it’s the one that fits your unique situation. It protects you from financial ruin during a medical emergency, covers routine checkups, and gives you access to the doctors and treatments you need. For freelancers especially, where benefits aren’t always included, choosing the right plan isn’t just smart—it’s essential. In this guide, we’ll walk you through everything you need to know to make an informed decision. We’ll break down confusing terms, compare plan types, and share practical tips so you can feel confident about your choice. Ready to take control of your health and finances? Let’s dive in.

Understanding the Basics: What Is Medical Insurance?

Before we get into the nitty-gritty of choosing a plan, let’s start with the foundation: what exactly is medical insurance? At its core, medical insurance is a contract between you and an insurance company. You pay a monthly fee—called a premium—and in exchange, the insurer agrees to cover a portion of your medical costs. This could be anything from a routine doctor visit to a major surgery or emergency room trip.

Visual guide about How to Choose the Best Medical Insurance Plan

Image source: sipfund.com

Think of it like this: insurance spreads the risk. If 10,000 people pay $200 a month into a pool, and one person has a $50,000 surgery, the insurance company can cover most of it from that shared pool. That way, no single person has to pay the full cost out of pocket. But here’s the catch: insurance doesn’t cover everything. You’ll still have out-of-pocket costs, which is why understanding the different parts of a plan is so important.

Key Components of a Medical Insurance Plan

Every plan has a few core pieces that work together to determine how much you pay and what’s covered. Let’s break them down:

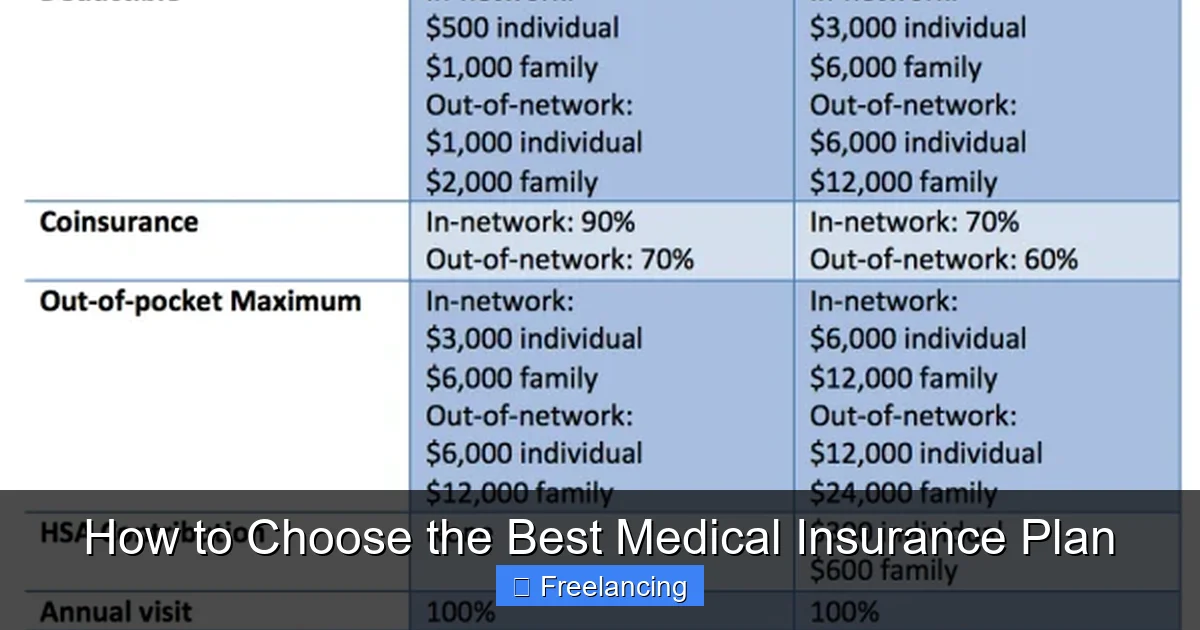

- Premium: This is the amount you pay every month for your insurance, regardless of whether you use it or not. For example, if your premium is $300/month, you pay $300, even if you don’t visit the doctor that month.

- Deductible: This is the amount you must pay for covered services before your insurance starts to pay. Let’s say your deductible is $1,500. You’ll pay the first $1,500 of medical expenses yourself. After that, your plan kicks in.

- Copay: A fixed amount you pay for certain services, like a $25 copay for a doctor’s visit or $10 for a prescription. Copays usually apply after you’ve met your deductible.

- Coinsurance: This is the percentage of costs you share with the insurer after you’ve met your deductible. If your coinsurance is 20%, and a procedure costs $1,000, you pay $200 and the insurer pays $800.

- Out-of-pocket maximum: The most you’ll ever have to pay in a year for covered services. Once you hit this limit, the insurance covers 100% of additional costs. For example, if your out-of-pocket max is $6,000, you won’t pay more than that in a single year.

These terms can be confusing, but once you understand them, comparing plans becomes much easier. For freelancers, who often pay for their own insurance, knowing these numbers helps you budget and avoid financial surprises.

Types of Medical Insurance Plans

Not all medical insurance plans are created equal. In fact, there are several types of plans available, each with its own structure and level of flexibility. The most common types in the U.S. include:

Visual guide about How to Choose the Best Medical Insurance Plan

Image source: i0.wp.com

1. Health Maintenance Organization (HMO)

HMO plans are among the most popular and affordable options. With an HMO, you must choose a primary care physician (PCP) who coordinates your care and gives referrals to see specialists. You typically need to stay within the plan’s network to get full coverage—going outside the network, except in emergencies, usually means paying the full cost.

Pros: Lower premiums and out-of-pocket costs, strong care coordination.

Cons: Limited provider choice, requires referrals for specialists.

Best for: People who want low costs and don’t mind having a PCP manage their care.

2. Preferred Provider Organization (PPO)

PPO plans offer more flexibility. You can see any doctor or specialist without a referral, and you can go in-network or out-of-network. However, going out-of-network costs more.

Pros: Greater freedom to choose providers, no need for referrals.

Cons: Higher premiums and out-of-pocket costs than HMOs.

Best for: Those who want flexibility and don’t mind paying a bit more for it.

3. Exclusive Provider Organization (EPO)

EPOs are a hybrid. Like HMOs, you must use network providers to get coverage—except for emergencies. But like PPOs, you don’t need referrals to see specialists.

Pros: Lower costs than PPOs, more flexibility than HMOs.

Cons: No coverage for out-of-network care (except emergencies).

Best for: People who want balance between cost and flexibility.

4. Point of Service (POS)

POS plans combine features of HMOs and PPOs. You choose a primary care physician and need referrals for specialists, but you can go out-of-network at a higher cost.

Pros: Some flexibility, coordinated care.

Cons: More complex, higher costs for out-of-network care.

Best for: Those who want some control but still value care coordination.

5. High-Deductible Health Plan (HDHP)

HDHPs have lower premiums but higher deductibles. They’re often paired with a Health Savings Account (HSA), which lets you save pre-tax money for medical expenses.

Pros: Lower monthly costs, tax advantages with HSA, ideal for healthy people who don’t expect major medical bills.

Cons: High out-of-pocket costs until deductible is met.

Best for: Freelancers or young adults who are generally healthy and want to save on premiums.

For freelancers, HDHPs with HSAs are especially attractive because they offer tax savings and long-term flexibility. But if you have ongoing health needs, a lower-deductible plan might be better.

How to Evaluate Your Healthcare Needs

Choosing the best medical insurance plan starts with knowing yourself—specifically, your health habits and needs. A plan that works for someone else might not work for you. Let’s walk through how to assess your situation.

Visual guide about How to Choose the Best Medical Insurance Plan

Image source: slideteam.net

Assess Your Health History

Ask yourself: Do you have any chronic conditions like diabetes or asthma? Do you take regular medications? How often do you visit the doctor? If you have ongoing health needs, you’ll want a plan with lower out-of-pocket costs and strong specialist access.

Example: Sarah, a freelance graphic designer, has asthma and visits her pulmonologist twice a year. She needs a plan that covers specialist visits and prescription inhalers without high copays.

Consider Your Family Situation

Are you single, married, or planning to start a family? If you have dependents, you’ll need coverage for spouses and children. Some plans offer family plans with higher premiums but broader coverage.

Tip: Look for plans that allow you to add family members easily, especially if you’re freelancing and may need to scale coverage as your situation changes.

Think About Lifestyle and Location

If you travel frequently for work or live in an area with limited healthcare providers, you’ll want a plan with a broad network or national coverage. For example, if you’re a freelance consultant who travels across the country, a PPO or national HMO might be better than a regional plan.

Estimate Annual Healthcare Spending

Make a rough calculation: How much do you expect to spend on healthcare this year? Include doctor visits, prescriptions, lab tests, and potential emergencies. Compare this to the plan’s premium, deductible, and out-of-pocket max. The goal is to find a balance where the total cost (premiums + expected out-of-pocket) is affordable.

Example: Mike, a freelance writer, estimates $2,000 in annual healthcare costs. He compares two plans: Plan A has a $400/month premium and $1,000 deductible; Plan B has a $300/month premium and $2,500 deductible. Over a year, Plan A costs $5,800 total (premiums + expected out-of-pocket), while Plan B costs $5,500. For Mike, Plan B saves $300—but only if he doesn’t exceed his deductible.

Comparing Costs: Premiums vs. Out-of-Pocket Expenses

One of the biggest mistakes people make is choosing the cheapest plan based only on premium. But remember: the lowest premium might not be the most affordable in the long run. Let’s break down how to compare costs effectively.

Total Cost of Ownership

To compare plans, calculate the total cost of ownership: (Monthly premium × 12) + Expected out-of-pocket costs. This gives you a realistic picture of what you’ll pay in a year.

Example: Plan X: $250/month premium, $1,000 deductible, 20% coinsurance, $5,000 out-of-pocket max. If you expect $2,000 in medical expenses, your total cost might be $3,000 (premiums) + $1,000 (deductible) + $200 (coinsurance) = $4,200. Plan Y: $400/month premium, $500 deductible, 10% coinsurance, $4,000 out-of-pocket max. Total cost: $4,800 (premiums) + $500 + $150 = $5,450. In this case, Plan X is cheaper.

The Premium Trap

Plans with low premiums often have high deductibles. If you get sick or injured, you might end up paying thousands before insurance kicks in. Ask yourself: Can you afford to pay a high deductible if you need care?

Tip: For freelancers with irregular income, a plan with moderate premiums and lower out-of-pocket costs might be safer than a low-premium plan with high out-of-pocket risks.

HSAs and Tax Savings

If you choose an HDHP with an HSA, you can save pre-tax money for medical expenses. For 2024, the HSA contribution limit is $4,150 for individuals and $8,300 for families. This can significantly reduce your taxable income and help cover high deductibles.

Example: Emily, a freelance photographer, contributes $350/month to her HSA. That’s $4,200 a year in pre-tax savings. If she has a $2,000 medical bill, she can use her HSA to pay it—no tax hit.

Network and Provider Considerations

One of the most important—but often overlooked—aspects of choosing a medical insurance plan is the provider network. If your doctors aren’t in the network, you could end up paying full price, even for basic care.

Check Your Doctor’s Participation

Before enrolling, verify that your primary care physician, specialists, and hospitals are in-network. You can usually find this information on the insurer’s website or by calling customer service.

Red Flag: If your preferred doctor isn’t in-network, consider switching to a plan that includes them—or find a new doctor within the network.

Understand Out-of-Network Costs

Out-of-network care is usually not covered (except in emergencies) or only partially covered. For example, a PPO might cover 60% of out-of-network costs, while an HMO covers nothing.

Tip: If you travel frequently, look for plans with national or regional networks, like UnitedHealthcare or Blue Cross Blue Shield.

Telehealth and Virtual Care

Many plans now include telehealth services, which let you consult a doctor online for minor issues like colds, rashes, or mental health concerns. This can save time and money, especially for freelancers with busy schedules.

Example: A freelance developer in Austin has a mild rash. Instead of taking time off to visit a clinic, she uses her plan’s telehealth service and gets a prescription via video call—all for a $25 copay.

Additional Benefits and Features

Beyond the basics, many plans offer extra benefits that can improve your health and convenience. These aren’t always essential, but they can add real value.

Wellness Programs

Some insurers offer free gym memberships, smoking cessation programs, or nutrition counseling. These can help you stay healthy and reduce long-term medical costs.

Mental Health Coverage

Mental health is just as important as physical health. Make sure your plan covers therapy, counseling, and psychiatric care without high barriers.

Prescription Drug Coverage

Check the plan’s formulary (list of covered drugs). If you take regular medications, ensure they’re included and see the copay tiers. Tier 1 drugs (generics) are cheapest; Tier 3 (brand name) can be expensive.

Preventive Care

Most plans cover preventive services like annual checkups, vaccinations, and cancer screenings at no cost to you—even before you meet your deductible. Take advantage of these!

Dental and Vision

Some plans include dental and vision coverage, or offer discounts. If you wear glasses or need regular dental cleanings, this can save you money.

How to Enroll and Avoid Common Mistakes

Once you’ve chosen a plan, the next step is enrollment. But beware—there are common mistakes that can cost you.

Miss the Open Enrollment Period

In most states, you can only enroll in a new plan during the annual open enrollment period (usually November to December). Missing it means you can only sign up during a Special Enrollment Period (SEP)—like if you get married or lose other coverage.

Overlook Subsidies

If you’re eligible, you might qualify for premium tax credits or cost-sharing reductions through the Affordable Care Act (ACA) marketplace. These can lower your monthly payments and out-of-pocket costs.

Skip the Fine Print

Always read the Summary of Benefits and Coverage (SBC). It explains what’s covered, what’s not, and how to file claims. Skipping this could lead to surprises later.

Choose Based on Premium Alone

As we’ve said, the cheapest premium isn’t always the best deal. Always compare total costs and coverage.

Forget to Update Your Application

If your income or family size changes, update your application. This can affect your subsidy eligibility and plan cost.

Conclusion: Your Health, Your Choice

Choosing the best medical insurance plan isn’t about finding the cheapest option or the one with the most bells and whistles. It’s about finding the right balance of coverage, cost, and convenience for your unique situation. Whether you’re a freelancer managing irregular income, a young professional starting out, or someone with ongoing health needs, the right plan gives you peace of mind and protects you from financial disaster.

Take the time to assess your needs, compare plans carefully, and don’t be afraid to ask questions. Use online tools like Healthcare.gov, consult a licensed insurance broker, or talk to a financial advisor. And remember: your health is your greatest asset—don’t skimp on protection.

With the right plan, you’re not just buying insurance—you’re investing in your future. And that’s worth every penny.

Frequently Asked Questions

What is the difference between a premium and a deductible?

A premium is the monthly cost you pay for insurance, while a deductible is the amount you pay out of pocket for covered services before your insurance starts to cover costs. Think of the premium as your monthly subscription fee, and the deductible as your initial out-of-pocket expense.

Can I change my medical insurance plan outside of open enrollment?

Yes, but only during a Special Enrollment Period (SEP), which is triggered by major life events like getting married, having a baby, losing other coverage, or moving to a new state. Otherwise, you’ll need to wait for the next open enrollment period.

Is it worth choosing a high-deductible plan with an HSA?

For healthy individuals who don’t expect major medical expenses, an HDHP with an HSA can save money on premiums and offer tax advantages. The HSA funds can grow tax-free and roll over year to year, making it a powerful tool for long-term savings.

How do I find out if my doctor is in-network?

You can check your insurer’s provider directory on their website or call their customer service line. Most insurers also have searchable online tools where you can enter your doctor’s name or ZIP code to verify participation.

What is the out-of-pocket maximum, and why does it matter?

The out-of-pocket maximum is the most you’ll pay for covered services in a year. Once you reach this limit, the insurance covers 100% of additional costs. It’s important because it protects you from catastrophic medical bills.

Are mental health services covered under most medical insurance plans?

Yes, under the Mental Health Parity and Addiction Equity Act, most plans must cover mental health and substance use disorder services at the same level as physical health services. However, coverage details vary, so check your plan’s summary of benefits.