Global health insurance is essential for travelers, expats, and digital nomads. It offers medical coverage anywhere in the world, protecting you from unexpected health expenses. This guide walks you through the entire application process—so you can stay healthy and worry-free, no matter where life takes you.

Key Takeaways

- Understanding How to Apply for Global Health Insurance: Provides essential knowledge

📑 Table of Contents

- How to Apply for Global Health Insurance: A Complete Guide

- Why Global Health Insurance Matters

- Types of Global Health Insurance

- How to Choose the Right Global Health Insurance Plan

- What You’ll Need to Apply

- How to Apply for Global Health Insurance: Step-by-Step

- Tips for a Smooth Application

- Common Mistakes to Avoid

- How Much Does Global Health Insurance Cost?

- Renewing and Updating Your Policy

- Conclusion: Stay Protected, Stay Free

How to Apply for Global Health Insurance: A Complete Guide

Imagine this: you’re hiking through the Swiss Alps, or working remotely from a café in Bali, when suddenly you feel dizzy. Or worse—you twist your ankle while exploring Machu Picchu. Without proper medical care, a simple injury could cost thousands. That’s where global health insurance comes in. It’s your safety net, your peace of mind, and your financial shield when you’re far from home.

Whether you’re a digital nomad, an expat, a student abroad, or just a frequent traveler, having international health coverage is no longer optional—it’s essential. But applying for it? That’s where confusion often begins. Where do you start? What do you need? How much does it cost? Don’t worry. This guide breaks it all down, step by step, so you can apply with confidence and stay protected anywhere in the world.

In this article, we’ll walk you through everything from understanding your needs to choosing the right provider, gathering documents, and completing your application. We’ll also share real-world examples, tips from seasoned travelers, and answers to common questions. By the end, you’ll know exactly how to apply for global health insurance—no jargon, no stress.

Why Global Health Insurance Matters

Let’s face it: medical emergencies don’t wait for you to be prepared. A sudden illness or injury can happen anywhere—on a cruise ship, in a foreign hospital, or while backpacking through Southeast Asia. Without insurance, you could face medical bills in the tens of thousands of dollars. That’s not just scary—it’s financially devastating.

Visual guide about How to Apply for Global Health Insurance

Image source: images.movehub.com

Global health insurance protects you from these risks. It covers doctor visits, hospital stays, emergency care, prescriptions, and sometimes even evacuations. Some plans even include telemedicine, mental health support, and dental care. And the best part? You can access care almost anywhere in the world.

Who Needs Global Health Insurance?

Not everyone needs the same type of coverage. Here’s who should seriously consider global health insurance:

- Digital nomads: If you’re working remotely across multiple countries, you need coverage that follows you.

- Expatriates: If you’re moving abroad long-term, local health systems might not cover you.

- Students studying abroad: Most U.S. student plans don’t cover you outside the U.S.

- Frequent travelers: Even if you’re just visiting, a short-term plan can save you in emergencies.

- Freelancers and remote workers: You’re not tied to one country’s system—so you need flexible coverage.

Even if you’re healthy now, accidents happen. And health care costs are rising globally. A broken leg in Germany could cost over $10,000. In Japan, a single night in the hospital can be $3,000. Without insurance, these costs could wipe out your savings—or worse, leave you in debt.

Types of Global Health Insurance

Before applying, it’s important to know the different types of global health insurance available. Each serves a different purpose, so choose wisely.

Visual guide about How to Apply for Global Health Insurance

Image source: healthygk.com

1. Travel Health Insurance

This is the most common type for short-term travelers. It typically covers trips lasting up to 180 days. Plans vary, but they usually include:

- Emergency medical treatment

- Hospitalization

- Medical evacuation

- Trip interruption or cancellation (in some plans)

Best for: Vacationers, business travelers, and short-term visitors.

Example: You’re going on a two-week trip to Italy. You buy a travel insurance plan that covers you for the duration. If you get food poisoning, you’re covered for treatment and repatriation if needed.

2. International Health Insurance (Long-Term)

This is for people living abroad for more than a year. It offers more comprehensive coverage, including:

- Regular doctor visits

- Prescription drugs

- Maternity care

- Pre-existing conditions (in some plans)

Best for: Expats, long-term remote workers, and people relocating for work or family.

Example: You’ve moved to Portugal for a year. You enroll in a long-term international plan that covers you for routine check-ups, chronic conditions, and emergency care—no matter where you go in the world.

3. Digital Nomad Health Insurance

Designed specifically for remote workers, these plans allow you to live and work across multiple countries. They often include:

- Flexible renewal periods

- Coverage in over 150 countries

- Telemedicine services

- No fixed address required

Best for: Freelancers, entrepreneurs, and location-independent professionals.

Example: You’re a freelance writer traveling every few months. You choose a nomad plan that lets you renew every 3 months and covers you in 170 countries. You can get a prescription in Thailand or a doctor’s visit in Spain—all covered.

4. Student Health Insurance Abroad

If you’re studying overseas, you’ll need a plan that complies with your school’s requirements. These plans usually include:

- Emergency medical care

- Mental health services

- Accidental death and dismemberment

Best for: International students and exchange programs.

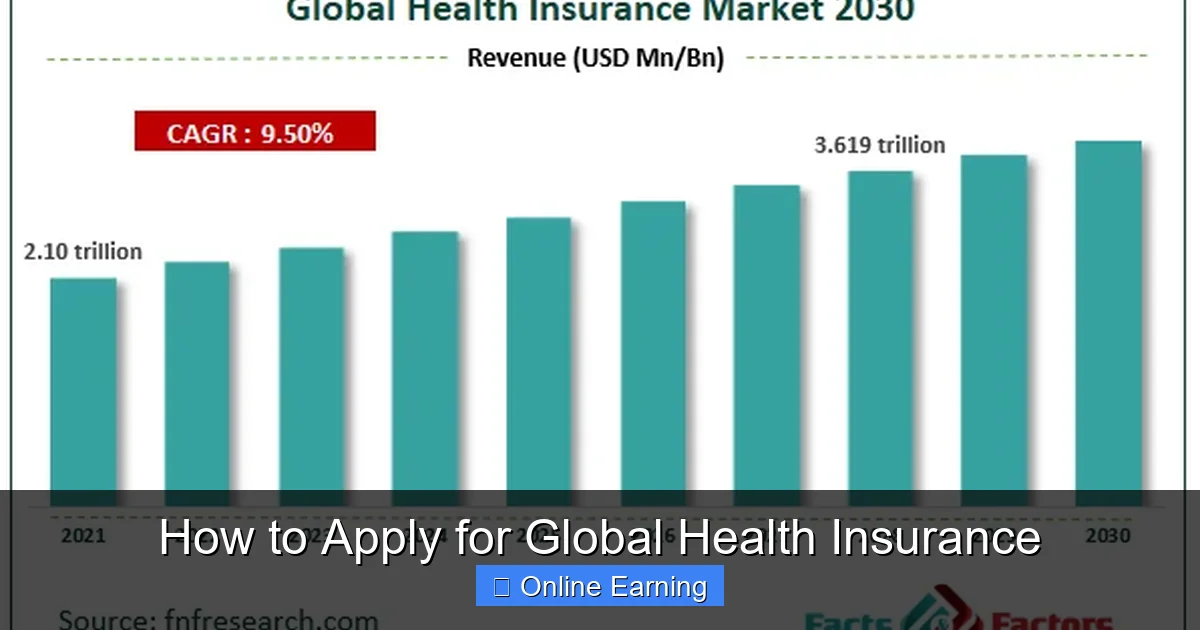

How to Choose the Right Global Health Insurance Plan

With so many options, choosing the right plan can feel overwhelming. Here’s how to make the best decision.

Visual guide about How to Apply for Global Health Insurance

Image source: fnfresearch.com

Step 1: Assess Your Needs

Start by asking yourself:

- How long will I be abroad?

- Do I have any chronic conditions?

- Will I be working or studying?

- Do I need maternity coverage?

- How much can I afford to pay out of pocket?

If you’re unsure, use a needs assessment quiz on insurer websites. Many providers offer tools to help you pick the right plan.

Step 2: Compare Providers

Not all insurers are created equal. Look for companies with:

- Global network of hospitals and doctors

- 24/7 customer support

- Positive customer reviews

- Clear terms and conditions

Top-rated providers include:

- World Nomads: Great for adventure travelers

- SafetyWing: Affordable for nomads

- Cigna Global: Comprehensive long-term plans

- Allianz Care: Strong for expats

- IMG Global: Popular with students

Use comparison websites like HealthPlans.com or InsureMyTrip.com to compare prices and features side by side.

Step 3: Check Coverage Limits and Exclusions

Every plan has limits. Make sure you understand:

- Maximum coverage per condition

- Annual or lifetime caps

- Excluded countries (e.g., war zones, high-risk areas)

- Pre-existing conditions (some plans cover them after a waiting period)

For example, a plan might cover up to $1 million in emergency care but only $50,000 for chronic conditions. Or it might exclude coverage in Venezuela or Syria.

Step 4: Consider Add-Ons

Many insurers offer optional add-ons, such as:

- Emergency evacuation

- Trip cancellation

- Adventure sports coverage

- Lost baggage

If you’re skydiving in New Zealand or scuba diving in the Maldives, you’ll want adventure sports coverage.

What You’ll Need to Apply

Applying for global health insurance is usually quick, but you’ll need some documents ready. Here’s what to gather:

- Passport: Full name, photo, and expiration date

- Travel itinerary: Dates and destinations

- Proof of address: If applying for a long-term plan, you may need a local address

- Bank details: For premium payments

- Medical history: Especially for long-term plans

Some insurers ask for:

- Employment details (for nomads)

- School enrollment (for students)

- Visa or residency documents

Tip: Save digital copies of all documents. You’ll need them for the application and for future renewals.

How to Apply for Global Health Insurance: Step-by-Step

Now for the main event: applying. Here’s a simple, step-by-step guide.

Step 1: Choose a Provider

Pick a reputable insurer based on your needs. If you’re a digital nomad, SafetyWing is a great choice. If you’re moving abroad for a year, Cigna Global offers strong long-term plans.

Visit the provider’s website and look for “Get a Quote” or “Apply Now.”

Step 2: Fill Out the Application Form

You’ll be asked for personal details like:

- Full name and date of birth

- Email and phone number

- Country of residence

- Travel dates

- Employment status

Be honest. If you lie, your claim could be denied later.

Step 3: Choose Your Plan

Select a plan based on your budget and needs. Most sites show a comparison table with:

- Premium (monthly cost)

- Deductible (out-of-pocket amount before coverage kicks in)

- Coverage limits

- Exclusions

Example: SafetyWing’s Nomad Plan starts at $45/month with a $150 deductible and $250,000 medical coverage.

Step 4: Upload Documents

Upload your passport, itinerary, and other required files. Most uploads are instant.

Step 5: Pay the Premium

You can usually pay monthly or annually. Annual payments often come with a discount. Use a credit card for added fraud protection.

Step 6: Receive Your Policy

Once approved, you’ll get a policy number and digital certificate. Print it and carry it with you when traveling.

Step 7: Keep It Updated

Update your policy if your plans change—new destinations, longer stays, or new health conditions.

Tips for a Smooth Application

Want to avoid headaches? Follow these tips.

- Apply early: Don’t wait until the last minute. Some plans require medical underwriting, which can take days.

- Read the fine print: Understand what’s covered and what’s not.

- Use a broker: If you’re confused, a licensed insurance broker can help.

- Check for discounts: Some insurers offer discounts for annual payments, good health, or group plans.

- Renew on time: Lapses in coverage can lead to claim denials.

Real-life example: Maria, a digital nomad from Canada, applied for SafetyWing’s plan online. She uploaded her passport, selected a 3-month plan, and paid by credit card. She received her policy in under an hour and was covered immediately—even in remote areas of Patagonia.

Common Mistakes to Avoid

Even experienced travelers make these mistakes.

- Buying the cheapest plan: Low cost often means low coverage. You’ll pay more in the long run.

- Ignoring pre-existing conditions: Some plans exclude them unless you apply within a “look-back period.”

- Not checking country exclusions: If you’re going to Iran, North Korea, or Syria, coverage may be limited or excluded.

- Forgetting to renew: A 1-day gap can mean no coverage.

- Not carrying your card: Always keep a printed copy in your wallet.

How Much Does Global Health Insurance Cost?

Prices vary widely. Here’s a rough estimate:

- Travel insurance: $50–$200 for a 2-week trip

- Nomad plan: $30–$60/month

- Long-term international plan: $100–$400/month (depending on age, coverage, and country)

Factors affecting cost:

- Age (older = more expensive)

- Destination (U.S. is expensive; Southeast Asia is cheaper)

- Coverage level (basic vs. premium)

- Deductible (higher deductible = lower premium)

Tip: A $500 deductible can save you $20–$30/month. Just make sure you can afford to pay it if needed.

Renewing and Updating Your Policy

Insurance isn’t a “set it and forget it” thing. You’ll need to renew and update regularly.

- Renewals: Most plans auto-renew, but review terms each year.

- Updates: Notify your insurer of new destinations, health changes, or visa status.

- Changes: You can usually switch plans or add coverage mid-term.

Example: You started with a 3-month nomad plan. After 2 months, you decide to stay in Portugal for a year. You upgrade to a long-term plan and add maternity coverage.

Conclusion: Stay Protected, Stay Free

Applying for global health insurance doesn’t have to be complicated. With the right provider, a clear plan, and a few documents, you can get covered in minutes. Whether you’re hiking in Peru, working from a beach in Thailand, or studying in France, having health insurance means you’re prepared for anything.

Remember: you don’t need to be sick to need insurance. Accidents happen. Emergencies strike. And the peace of mind that comes with knowing you’re covered? That’s priceless.

So take the first step today. Compare plans, gather your documents, and apply. Your future self—sick, injured, or just needing a check-up—will thank you.

Frequently Asked Questions

Can I apply for global health insurance if I have a pre-existing condition?

Yes, but it depends on the insurer and plan. Some offer coverage after a waiting period, while others exclude pre-existing conditions. Always disclose your medical history during application.

How long does it take to get approved?

Most online applications are approved instantly or within 24 hours. Complex cases, like long-term expat plans, may take 1–3 days for underwriting.

Can I change my plan after applying?

Yes. Many insurers allow mid-term changes to coverage, destinations, or deductibles. Contact customer support to make updates.

Is global health insurance the same as travel insurance?

No. Travel insurance often includes medical coverage but may also include trip cancellation, lost luggage, and adventure sports. Global health insurance focuses solely on medical care.

Do I need global health insurance if I have U.S. health insurance?

Not always. U.S. plans may not cover you abroad, especially outside North America. Check your policy’s international coverage before traveling.

What happens if I don’t have insurance and get sick abroad?

You’ll pay out of pocket, which can be very expensive. Some countries require proof of insurance for visa applications or hospital admission. In emergencies, you may be denied care until payment is arranged.