Travel insurance and medical insurance serve different purposes, but both are vital for protecting your health and wallet. While medical insurance covers routine and emergency healthcare at home, travel insurance is designed for unexpected issues abroad, like trip cancellations or lost luggage. Understanding when to use each ensures you’re covered whether you’re staying in your home country or exploring the world.

Key Takeaways

- Different Purposes: Medical insurance covers healthcare needs at home, while travel insurance handles trip-specific risks like cancellations, delays, or emergencies while abroad.

- Geographic Scope: Medical insurance typically applies only within your home country, whereas travel insurance activates during international or domestic trips.

- Coverage Overlap: Some medical plans offer limited international coverage, and some travel plans include basic medical, but neither fully replaces the other.

- Cost Differences: Medical insurance is usually a long-term premium paid monthly or annually; travel insurance is a short-term, one-time purchase based on trip duration and destination.

- Emergency Protection: Travel insurance often includes emergency medical care abroad, evacuation, and repatriation—features not standard in most domestic medical plans.

- Trip-Specific Benefits: Beyond medical, travel insurance covers non-health perks like baggage loss, flight delays, and trip interruption—unrelated to medical needs.

- Plan Selection Matters: Choose medical insurance for daily health needs and travel insurance for peace of mind during your next adventure.

📑 Table of Contents

- Understanding the Basics: What Is Medical Insurance?

- What Is Travel Insurance and Why Do You Need It?

- Key Differences Between Medical and Travel Insurance

- Can Medical Insurance Cover Travel-Related Medical Emergencies?

- When You Might Need Both: A Real-Life Example

- Tips for Choosing the Right Insurance

- Common Misconceptions

- Conclusion: Protect Your Health and Your Trip

Understanding the Basics: What Is Medical Insurance?

Let’s start with the foundation: medical insurance. Think of it as your safety net at home. This type of coverage helps pay for doctor visits, hospital stays, prescriptions, surgeries, and preventive care. Most people in the U.S.—and many countries worldwide—rely on medical insurance as a core part of their healthcare strategy. Whether you have employer-sponsored coverage, a marketplace plan, or a private policy, the goal is the same: to reduce out-of-pocket expenses when you get sick or injured.

How Medical Insurance Works

When you visit a doctor or go to the hospital, your medical insurance kicks in based on your plan’s rules. You might pay a copayment upfront, and the insurer covers the rest—or you could meet a deductible first before coverage begins. Some plans have coinsurance, meaning you and the insurer split costs. Preventive services like vaccinations or annual checkups are often fully covered with no out-of-pocket cost.

For example, if you have a cold and visit your primary care physician, your medical insurance might cover 80% of the bill after you pay a $20 copay. If you need an X-ray or blood test, those are usually included too—depending on your plan. This system keeps healthcare more affordable and accessible.

Who Needs Medical Insurance?

Everyone does—especially if you’re not young, healthy, and perfectly self-sufficient. Even if you’re generally healthy, unexpected accidents or illnesses happen. Medical insurance protects you from financial ruin due to a single hospital stay. In many countries, it’s also legally required or strongly encouraged to have coverage.

For freelancers, gig workers, or those between jobs, securing affordable medical insurance is critical. Platforms like HealthCare.gov (in the U.S.) or government-run exchanges in other countries make it easier to compare and enroll in plans.

What Is Travel Insurance and Why Do You Need It?

Now, let’s talk about travel insurance. Unlike medical insurance, which focuses on healthcare at home, travel insurance is all about protecting your trip. It’s designed to cover unexpected events that could derail your vacation or business trip—whether you’re going across town or across the globe.

Visual guide about Comparing Travel Insurance and Medical Insurance

Image source: brunel-insurance.com

Travel insurance isn’t just for emergencies. It can help if your flight gets canceled, your luggage goes missing, or you need to cut your trip short due to a family emergency. Most importantly, it includes emergency medical coverage while you’re abroad—something most domestic medical plans don’t cover.

Types of Travel Insurance

- Trip Cancellation/Interruption Insurance: Reimburses non-refundable trip costs if you can’t travel due to covered reasons like illness, natural disasters, or job loss.

- Medical Coverage: Pays for doctor visits, hospital stays, and emergency treatments while traveling. This often includes evacuation and repatriation—airlifting you to a hospital or back home if needed.

- Baggage and Personal Belongings: Covers lost, stolen, or damaged luggage and personal items.

- Travel Delay: Compensates for expenses like meals and accommodation if your flight is delayed more than a certain number of hours.

- Accidental Death and Dismemberment (AD&D): Provides a lump-sum payment in case of accidental injury or death during the trip.

When Is Travel Insurance Worth It?

Even a quick weekend getaway can cost hundreds of dollars—flights, hotels, tours. If something goes wrong, the financial hit can be devastating. Travel insurance is especially valuable for:

- International trips (where medical care is expensive and not covered by domestic plans)

- Last-minute bookings (which may not be refundable)

- Pre-existing medical conditions (some plans cover them with proper documentation)

- Adventure travel (like scuba diving or hiking in remote areas)

For example, if you book a $3,000 vacation to Europe and fall ill before departure, trip cancellation insurance could refund your money. If you break your leg on a ski trip in Switzerland, emergency medical coverage could save you tens of thousands in hospital bills.

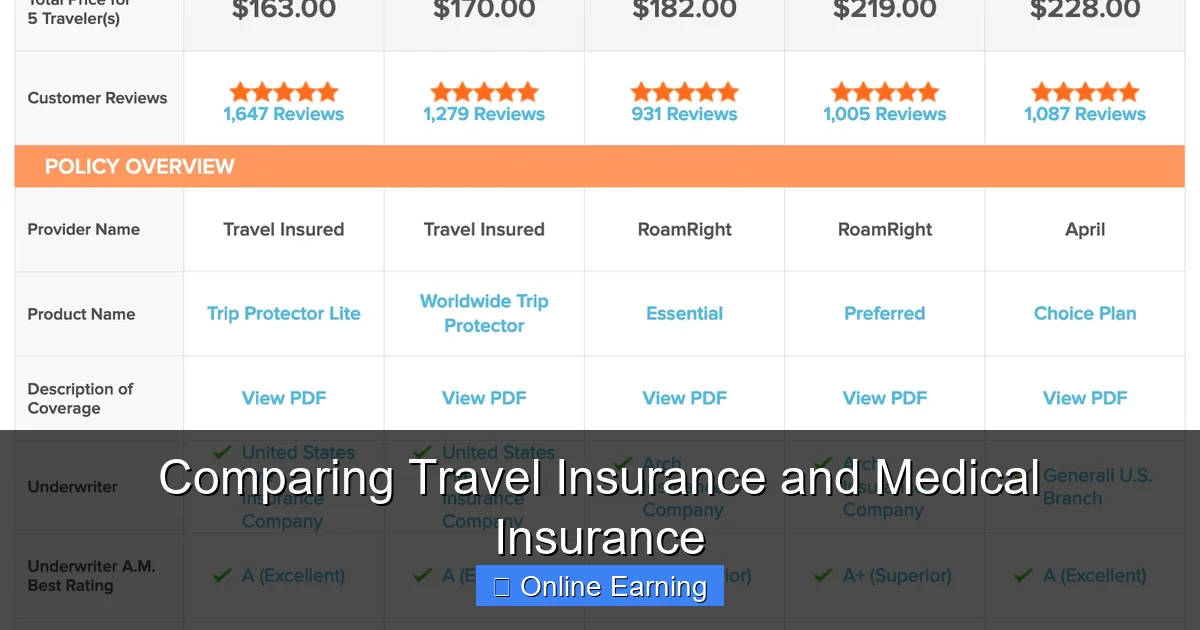

Key Differences Between Medical and Travel Insurance

At first glance, both types of insurance sound like they’re about health. But their purposes, coverage, and timing are quite different. Let’s break it down.

Visual guide about Comparing Travel Insurance and Medical Insurance

Image source: travelinsurancereview.net

1. Purpose and Scope

Medical insurance is for ongoing and routine healthcare needs. It’s your everyday health protection. Travel insurance is event-based—it activates only when you’re traveling and covers trip-related disruptions.

2. Geographic Coverage

Most medical insurance plans are limited to your home country. If you travel internationally, you may have little or no coverage. Travel insurance, by contrast, is built for international use. It follows you across borders and covers medical emergencies wherever you are.

3. Duration

Medical insurance is long-term—often a year or more. You pay monthly or annually. Travel insurance is short-term. You buy it when you book a trip, and it expires when you return home.

4. What’s Covered

Medical insurance covers doctor visits, prescriptions, surgeries, mental health services, and preventive care. Travel insurance covers medical emergencies abroad, trip cancellations, baggage loss, flight delays, and more—but not routine healthcare.

5. Cost

Medical insurance premiums can be high, especially for individuals or families. Travel insurance is usually affordable—often just a few dollars per day for a week-long trip. For a two-week vacation, you might pay $100–$300, depending on your age, destination, and coverage level.

Can Medical Insurance Cover Travel-Related Medical Emergencies?

This is a common question: “Does my medical insurance cover me if I get sick while traveling?” The short answer: usually not.

Visual guide about Comparing Travel Insurance and Medical Insurance

Image source: travelinsurance.com

Limited International Coverage

Some medical plans offer limited international coverage, but it’s rare and often comes with major restrictions. For example, you might get emergency care in another country, but only if you’re within a certain distance of home or if the treatment is pre-approved. Many plans exclude coverage entirely abroad.

Travel Insurance Fills the Gap

This is where travel insurance shines. It’s specifically designed for international medical emergencies. If you’re in Japan and need an ambulance, your travel insurance can cover the cost—often up to $100,000 or more. It also handles evacuation, which can cost $50,000+ on its own.

For instance, if you’re hiking in the Andes and suffer altitude sickness, travel insurance can arrange a helicopter evacuation to a hospital. Without it, you’d likely face massive bills and no support.

What About Pre-Existing Conditions?

Some travel insurance plans cover pre-existing medical conditions if you purchase the policy within a certain time frame of booking your trip (usually 10–21 days). You may need to provide medical records or pay an additional premium. Medical insurance, however, doesn’t cover travel-related issues—even if the condition is pre-existing.

When You Might Need Both: A Real-Life Example

Imagine Sarah, a freelance graphic designer in the U.S., who books a two-week trip to Thailand. She has a medical insurance plan through her previous employer, which covers her domestic healthcare. But when she arrives in Bangkok, she slips on a wet street and breaks her arm.

The Problem

Her medical insurance doesn’t cover her in Thailand. The hospital bills are in Thai baht, but the exchange rate makes them shockingly high—over $10,000 for surgery and rehabilitation. She didn’t think to buy travel insurance because she assumed her medical plan would follow her.

The Solution

If Sarah had purchased travel insurance, her policy would have covered the emergency medical expenses, including evacuation if needed. It might have also reimbursed her for trip interruption if she couldn’t return on time. Instead, she faced financial stress and had to ask family for help.

This example shows why travel insurance is essential for international trips, even if you have medical coverage at home.

Tips for Choosing the Right Insurance

With so many options, how do you pick? Here’s what to consider.

For Medical Insurance

- Check your network: Make sure your doctors and hospitals are in-network to avoid surprise bills.

- Understand your deductible: A lower deductible means higher monthly premiums but lower out-of-pocket costs when you need care.

- Review prescription coverage: Some plans don’t cover brand-name drugs unless generic alternatives aren’t available.

- Look for mental health coverage: Therapy and counseling should be included in your plan.

For Travel Insurance

- Read the fine print: Know what’s covered and what’s excluded—especially pre-existing conditions and adventure activities.

- Buy early: Purchase travel insurance within 10–21 days of booking to ensure pre-existing condition coverage.

- Choose based on trip cost: For expensive trips, the insurance premium is a small price for peace of mind.

- Check credit card benefits: Some cards offer trip cancellation insurance—but only for purchases made with that card.

Common Misconceptions

Let’s clear up some myths.

Myth 1: “I Don’t Need Travel Insurance If I Have Medical Insurance”

False. Most medical plans don’t cover international travel. Travel insurance fills that gap and adds trip protection.

Myth 2: “Travel Insurance Is Only for Expensive Trips”

Not true. Even a $200 weekend trip can be ruined by a sudden illness. A $30 travel insurance policy can save you $2,000 in medical bills.

Myth 3: “I’m Too Young and Healthy to Need Either”

Accidents happen to anyone. And even healthy people can face unexpected costs. It’s better to be prepared.

Myth 4: “My Credit Card Covers Everything”

Some cards offer limited coverage, but it’s often secondary to other insurance and excludes certain events. Don’t rely on it alone.

Conclusion: Protect Your Health and Your Trip

So, should you have medical insurance, travel insurance, or both? The answer is yes. They serve different roles and together create a safety net for your life at home and on the road.

Medical insurance keeps you healthy and financially secure when you’re at home. Travel insurance protects your investment in your trip and handles emergencies abroad. One isn’t a replacement for the other—they’re complementary.

Whether you’re planning a dream vacation, a business trip, or a quick city break, take the time to understand your options. The right insurance doesn’t just save you money—it gives you peace of mind. And in life, that’s priceless.

Frequently Asked Questions

Can I use my medical insurance while traveling internationally?

Most domestic medical insurance plans offer limited or no coverage abroad. Even if you have international coverage, it’s often restricted. For full protection, travel insurance is recommended for international trips.

Does travel insurance cover pre-existing medical conditions?

Some travel insurance plans cover pre-existing conditions if you purchase the policy within 10–21 days of booking and meet other requirements. Always check the policy details and apply early.

Is travel insurance worth it for domestic trips?

Yes, especially for expensive trips. Even a domestic flight or hotel booking can cost hundreds. Travel insurance covers cancellations, delays, and medical emergencies, providing valuable protection.

Can I buy travel insurance after my trip has started?

Yes, but coverage may be limited. Emergency medical coverage is available, but trip cancellation benefits usually require purchasing the policy before departure. Act quickly if something goes wrong.

What’s the difference between travel medical insurance and full travel insurance?

Travel medical insurance covers only medical emergencies abroad. Full travel insurance includes medical coverage plus trip cancellation, baggage loss, delays, and other non-medical perks.

How much does travel insurance cost?

It varies by age, destination, trip length, and coverage level. For a two-week domestic trip, expect to pay $50–$200. International trips may cost more, especially for older travelers or adventure activities.