Medical insurance and health insurance are often used interchangeably, but they aren’t exactly the same. Medical insurance typically covers specific medical treatments and doctor visits, while health insurance is broader, including preventive care, wellness programs, and sometimes life insurance. Understanding the difference helps you choose the right plan for your needs and budget.

Key Takeaways

- Medical Insurance covers specific medical services like surgeries, hospital stays, and doctor visits.

- Health Insurance is a broader category that includes medical insurance plus preventive care, wellness, and sometimes dental and vision.

- Medical insurance plans are usually tied to employer-sponsored or individual hospital and surgical plans.

- Health insurance often includes HMOs, PPOs, and government programs like Medicare and Medicaid.

- Preventive care like vaccinations and annual checkups are more commonly covered under health insurance.

- Understanding your coverage can save you money and improve access to care.

- Choosing the right plan depends on your health needs, budget, and where you live.

📑 Table of Contents

- Medical Insurance vs Health Insurance Explained: What You Need to Know

- What Is Medical Insurance?

- What Is Health Insurance?

- Key Differences Between Medical and Health Insurance

- When to Choose Medical Insurance

- When to Choose Health Insurance

- How to Choose Between Medical and Health Insurance

- Common Misconceptions

- Real-Life Examples

- Tips for Managing Your Health Insurance

- Conclusion

Medical Insurance vs Health Insurance Explained: What You Need to Know

Have you ever looked at your health insurance bill and wondered, “Wait—is this medical insurance or just health insurance?” You’re not alone. In everyday conversation, people often use “medical insurance” and “health insurance” as if they mean the same thing. But in reality, they’re not identical. Understanding the difference can help you make smarter decisions about your coverage, avoid unexpected bills, and get the care you need without financial stress.

In this article, we’ll break down what medical insurance and health insurance actually mean, how they differ, and why it matters. Whether you’re shopping for your first plan, switching jobs, or just trying to understand your current coverage, this guide will give you clear, practical insights. We’ll use simple language, real-life examples, and helpful tips to make sure you walk away feeling confident about your health coverage.

What Is Medical Insurance?

Medical insurance is a type of health coverage that pays for specific medical services when you’re sick or injured. Think of it as a safety net for when things go wrong—like a broken bone, a sudden illness, or an emergency room visit. It’s designed to help cover the costs of diagnosis, treatment, hospitalization, and sometimes even surgeries.

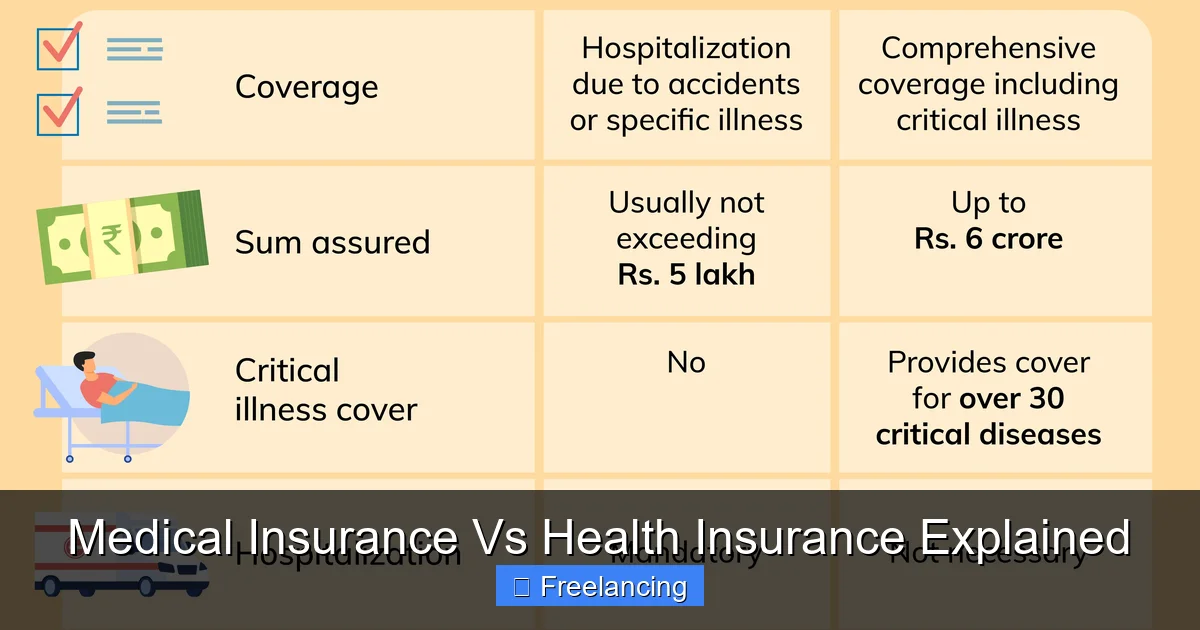

Visual guide about Medical Insurance Vs Health Insurance Explained

Image source: image.slidesharecdn.com

Key Features of Medical Insurance

Medical insurance plans usually come in two main types: hospital insurance and surgical insurance. Hospital insurance covers expenses like room and board, nursing care, and diagnostic tests during your stay. Surgical insurance, on the other hand, covers the cost of surgeries, including the surgeon’s fee and anesthesia.

For example, if you break your leg and need surgery, your medical insurance might cover the hospital stay, the surgeon’s fee, and the cost of the cast. But it probably won’t cover your physical therapy sessions unless they’re part of the initial treatment plan.

Most medical insurance plans are offered through employers or purchased individually. They often require you to pay a deductible—the amount you pay out of pocket before the insurance kicks in—and may have copayments or coinsurance for services.

Who Needs Medical Insurance?

If you’re at risk for unexpected health issues—like a family history of heart disease or a physically demanding job—medical insurance is essential. It’s especially important if you don’t have a lot of savings to cover a sudden medical bill. Without it, a single ER visit could cost thousands of dollars.

What Is Health Insurance?

Health insurance is a broader term that includes medical insurance but goes beyond it. While medical insurance focuses on treating illness or injury, health insurance covers a wider range of services—including preventive care, wellness programs, mental health, dental, and vision.

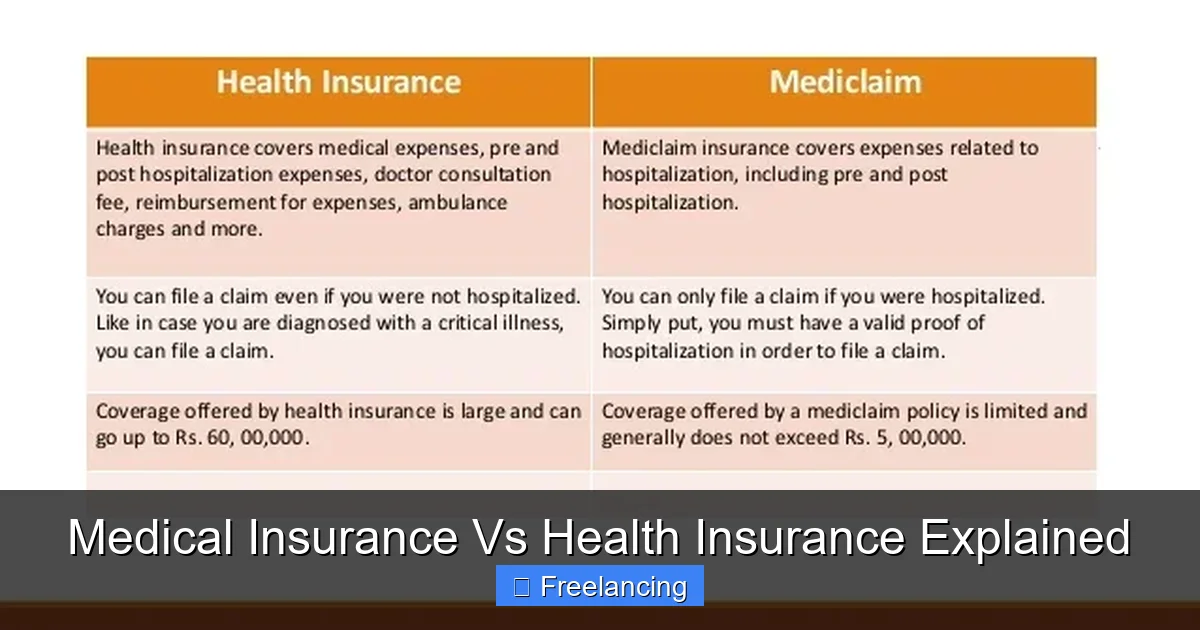

Visual guide about Medical Insurance Vs Health Insurance Explained

Image source: web-assets.metrobank.com.ph

What’s Included in Health Insurance?

A typical health insurance plan might include:

- Doctor visits and specialist consultations

- Prescription drug coverage

- Mental health services like therapy and counseling

- Dental and vision care (sometimes as add-ons)

- Preventive services such as vaccinations, cancer screenings, and annual checkups

- Emergency care and hospitalization

- Rehabilitation services like physical therapy

For example, under a health insurance plan, you might get a free flu shot, a yearly mammogram, or coverage for therapy sessions—all without paying a copay. These services are designed to keep you healthy and catch problems early.

Types of Health Insurance Plans

Health insurance plans come in several forms, each with its own rules about where you can go for care and how much you pay. The most common types include:

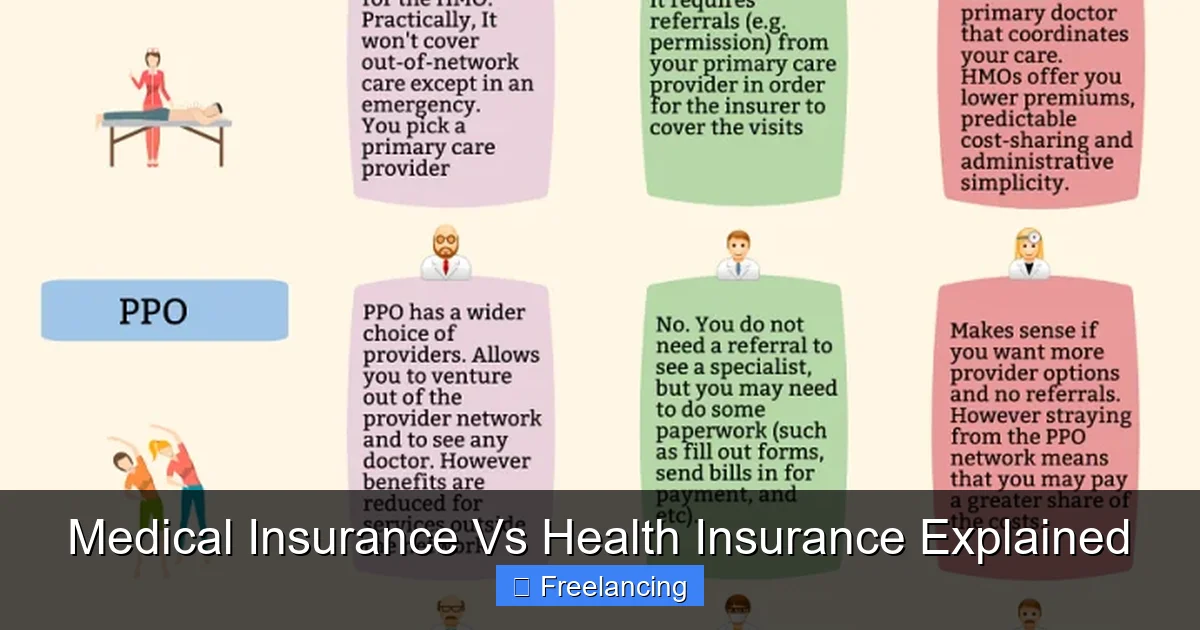

- HMO (Health Maintenance Organization): Requires you to choose a primary care doctor and get referrals to see specialists. You usually pay less for care, but you must stay within the HMO network.

- PPO (Preferred Provider Organization): Gives you more flexibility. You can see any doctor or specialist without a referral, but you pay more if you go out of network.

- EPO (Exclusive Provider Organization): Similar to PPOs, but you usually can’t use out-of-network care except in emergencies.

- POS (Point of Service): Combines HMO and PPO features. You need a referral for specialists, but you can go out of network for a higher cost.

Health insurance is often provided through employers, government programs like Medicare and Medicaid, or purchased on the individual market through health exchanges.

Key Differences Between Medical and Health Insurance

Now that we’ve defined both terms, let’s compare them side by side. The main difference lies in scope. Medical insurance is a subset of health insurance. Think of health insurance as the umbrella, and medical insurance as one of the shaded areas under it.

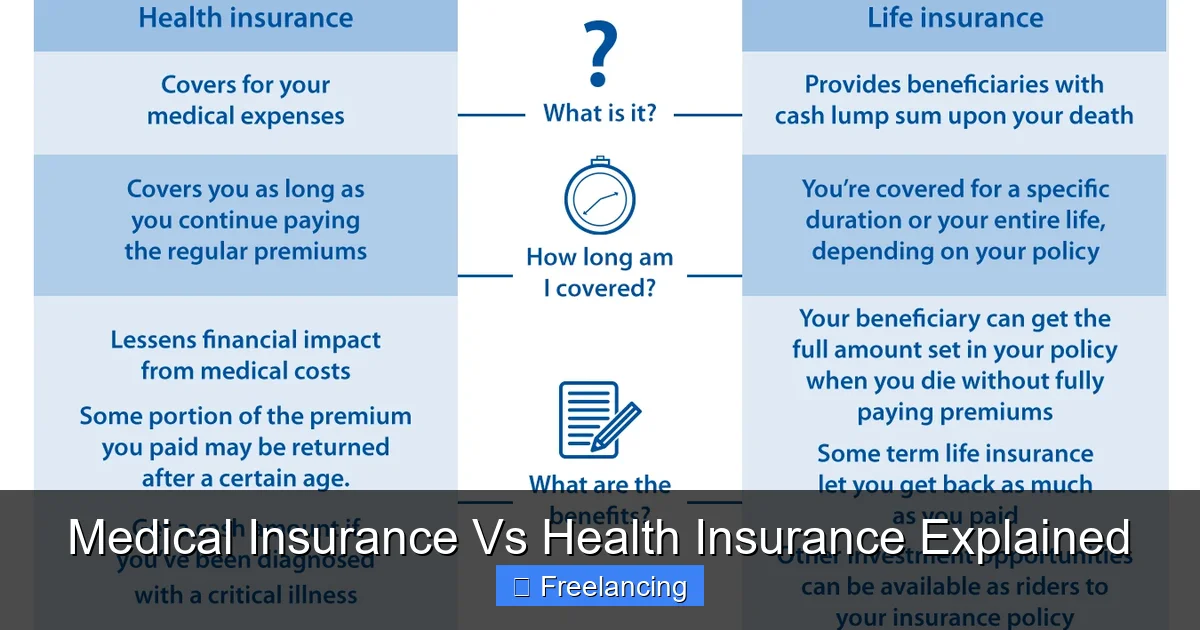

Visual guide about Medical Insurance Vs Health Insurance Explained

Image source: i0.wp.com

Coverage Scope

Medical insurance covers only specific medical treatments and emergencies. Health insurance covers a wider range of services, including preventive care, mental health, and wellness programs.

For example, if you have a cold and visit your doctor, medical insurance might cover the visit. But if that same doctor recommends a flu shot and a blood pressure check, those are more likely to be covered under health insurance—even if they’re part of the same visit.

Preventive Care

One of the biggest differences is preventive care. Health insurance plans often require coverage for preventive services at no extra cost to you. This includes things like annual physicals, vaccinations, and cancer screenings. Medical insurance may not include these unless they’re directly related to treating an illness.

Cost Structure

Medical insurance plans often have higher deductibles and are more focused on covering large, unexpected expenses. Health insurance plans may have lower out-of-pocket costs for routine care and preventive services.

Flexibility

Health insurance plans, especially PPOs, offer more flexibility in choosing doctors and hospitals. Medical insurance plans may be more limited, especially if they’re tied to specific providers.

When to Choose Medical Insurance

Medical insurance is a good choice if you:

- Are healthy and rarely need medical care

- Want to avoid high premiums by choosing a plan with a high deductible

- Are self-employed and want a cost-effective way to cover major medical expenses

- Are on a tight budget and can’t afford full health insurance

For example, if you’re young, active, and have no chronic conditions, you might opt for a high-deductible medical insurance plan. You pay lower monthly premiums, and if you get sick, the plan kicks in to cover the big bills.

Tip: Consider a Health Savings Account (HSA)

If you choose a high-deductible medical insurance plan, you might be eligible for an HSA. This is a tax-advantaged account where you can save money for medical expenses. Contributions are tax-deductible, and withdrawals for qualified medical costs are tax-free.

When to Choose Health Insurance

Health insurance is the better choice if you:

- Have a chronic condition like diabetes or asthma

- Need regular doctor visits or preventive care

- Have dependents (children or elderly parents) who need care

- Want access to mental health, dental, or vision services

- Prefer predictable monthly costs with lower out-of-pocket expenses

For instance, if you have a family history of heart disease, you’ll benefit from regular checkups and screenings covered by health insurance. You’ll also save money on prescriptions, therapy, and other wellness services.

Tip: Look for Employer-Sponsored Plans

If your employer offers health insurance, it’s often a smart choice. Many employers pay a portion of the premium, which can make coverage more affordable. Plus, you’ll get access to a wide network of doctors and hospitals.

How to Choose Between Medical and Health Insurance

Choosing the right plan depends on your health needs, budget, and lifestyle. Here’s how to decide:

Assess Your Health Needs

Ask yourself: How often do you visit the doctor? Do you have any chronic conditions? Do you need mental health support? If you’re healthy and rarely need care, medical insurance might be enough. If you need ongoing care, health insurance is likely better.

Compare Costs

Look at the total cost, including premiums, deductibles, copays, and coinsurance. A plan with lower premiums might sound cheaper, but if it has a high deductible, you could end up paying more when you need care.

Check the Network

Make sure your preferred doctors and hospitals are in the plan’s network. Going out of network can mean higher costs or no coverage at all.

Review Benefits

Read the plan details. Does it cover preventive care? Prescription drugs? Mental health services? Choose a plan that fits your needs.

Consider Government Programs

If you’re low-income, you might qualify for Medicaid. If you’re 65 or older, Medicare is an option. These programs offer comprehensive health insurance at little or no cost.

Common Misconceptions

Even experts get confused. Let’s clear up some myths:

- Myth: “Medical insurance and health insurance are the same.”

Reality: Medical insurance is a type of health insurance, but not all health insurance is medical insurance. - Myth: “I only need health insurance if I’m sick.”

Reality: Preventive care is a key part of health insurance and helps you stay healthy. - Myth: “Health insurance is too expensive.”

Reality: There are affordable options, especially if you qualify for subsidies or employer plans.

Real-Life Examples

Let’s look at two scenarios:

Example 1: Sarah, Age 28, Healthy and Active

Sarah is a freelance graphic designer with no chronic conditions. She exercises regularly and rarely gets sick. She chooses a high-deductible medical insurance plan with a $3,000 deductible. Her monthly premium is $150, much lower than a full health insurance plan. If she breaks her arm, the plan covers the hospital and surgery after she pays the deductible. For routine care like a flu shot, she pays out of pocket. She also opens an HSA to save for future medical expenses.

Example 2: James, Age 45, with Diabetes

James has type 2 diabetes and needs regular checkups, insulin, and blood sugar monitoring. He chooses a PPO health insurance plan. His plan covers doctor visits, prescriptions, and lab tests with low copays. He also gets free annual screenings and counseling for stress management. Because the plan covers everything he needs, he spends less overall than if he had only medical insurance.

Tips for Managing Your Health Insurance

No matter which plan you choose, here are some tips to make the most of it:

- Keep track of your deductible and out-of-pocket maximum.

- Use in-network providers to avoid surprise bills.

- Schedule preventive care annually.

- Ask your doctor about generic drugs or lower-cost treatment options.

- Review your plan every year during open enrollment.

- Use telehealth services for minor issues—they’re often cheaper and more convenient.

Conclusion

Medical insurance and health insurance may sound similar, but they serve different purposes. Medical insurance is focused on covering specific medical treatments and emergencies. Health insurance is broader, including preventive care, wellness, and a wider range of services. Choosing the right one depends on your health needs, budget, and lifestyle.

Remember, the goal isn’t just to save money—it’s to protect your health and financial well-being. Whether you choose medical or health insurance, the most important thing is to understand your coverage and use it wisely. Take the time to compare plans, ask questions, and make an informed decision. Your health—and your wallet—will thank you.

Frequently Asked Questions

Is medical insurance the same as health insurance?

No, medical insurance is a type of health insurance that covers specific medical treatments like surgeries and hospital stays. Health insurance is broader and includes preventive care, wellness programs, and other services.

What does health insurance cover that medical insurance doesn’t?

Health insurance typically covers preventive care like vaccinations and screenings, mental health services, dental, vision, and wellness programs. Medical insurance focuses mainly on treating illness or injury.

Can I have both medical and health insurance?

Yes, some people have both—especially if they have a high-deductible health plan and a separate medical insurance plan for extra coverage. But it’s important to avoid double coverage to prevent unnecessary costs.

Which is better: medical insurance or health insurance?

It depends on your needs. If you’re healthy and want low premiums, medical insurance might work. If you need regular care or preventive services, health insurance is usually better.

Are preventive services covered by medical insurance?

Not always. Preventive services like annual checkups and screenings are more commonly covered under health insurance plans.

How do I choose the right plan?

Consider your health needs, budget, and preferred doctors. Compare premiums, deductibles, and coverage options. Don’t forget to check if you qualify for government programs like Medicaid or Medicare.