Medical insurance is your safety net when you get sick or injured. It helps cover the cost of doctor visits, hospital stays, and prescriptions so you don’t pay everything out of pocket. For freelancers and beginners, understanding how it works is essential to protecting your health and budget.

Key Takeaways

- Medical insurance reduces out-of-pocket costs: Instead of paying thousands for a hospital bill, insurance covers a large portion based on your plan.

- Premiums are monthly payments: You pay a set amount every month to keep your coverage active, even if you don’t use it.

- Deductibles must be met before coverage kicks in: You pay full cost until you spend enough on medical services to meet your deductible.

- Copays and coinsurance apply after deductibles: After you meet your deductible, you pay a fixed amount (copay) or a percentage (coinsurance) for services.

- Networks matter: Staying in-network usually costs less; going out-of-network may result in higher bills or no coverage.

- Freelancers often choose individual plans: As self-employed, you can buy private insurance through marketplaces or directly from insurers.

- Preventive care is often free: Many plans cover annual checkups, vaccines, and screenings with no out-of-pocket cost.

📑 Table of Contents

- How Medical Insurance Works for Beginners

- What Is Medical Insurance?

- The Basic Parts of a Medical Plan

- Types of Medical Insurance Plans

- How to Choose the Right Plan

- Medical Insurance for Freelancers

- Understanding Your Insurance Card and ID

- Common Mistakes Beginners Make

- How to Save Money on Medical Insurance

- Conclusion: You’ve Got This

How Medical Insurance Works for Beginners

So, you’re just starting out—maybe you’re freelancing, working part-time, or just figuring out your life. And now, you’ve heard about medical insurance. Maybe your friend got a bill for $1,000 after a broken arm. Or maybe you’ve seen ads on TV about health plans. But honestly, it all feels a little confusing. Don’t worry—you’re not alone. Medical insurance is one of those things that sounds complicated until you break it down.

In this article, we’re going to walk through exactly how medical insurance works—step by step—so you can feel confident about your choices. Whether you’re self-employed, just starting a career, or helping a family member understand their coverage, this guide will make sense of it all. We’ll explain the basics like premiums, deductibles, and copays. We’ll talk about how to pick a plan that fits your budget and needs. And we’ll even share tips for freelancers, who often have to navigate insurance on their own. By the end, you’ll know more about medical insurance than most people do—and that’s a big deal.

What Is Medical Insurance?

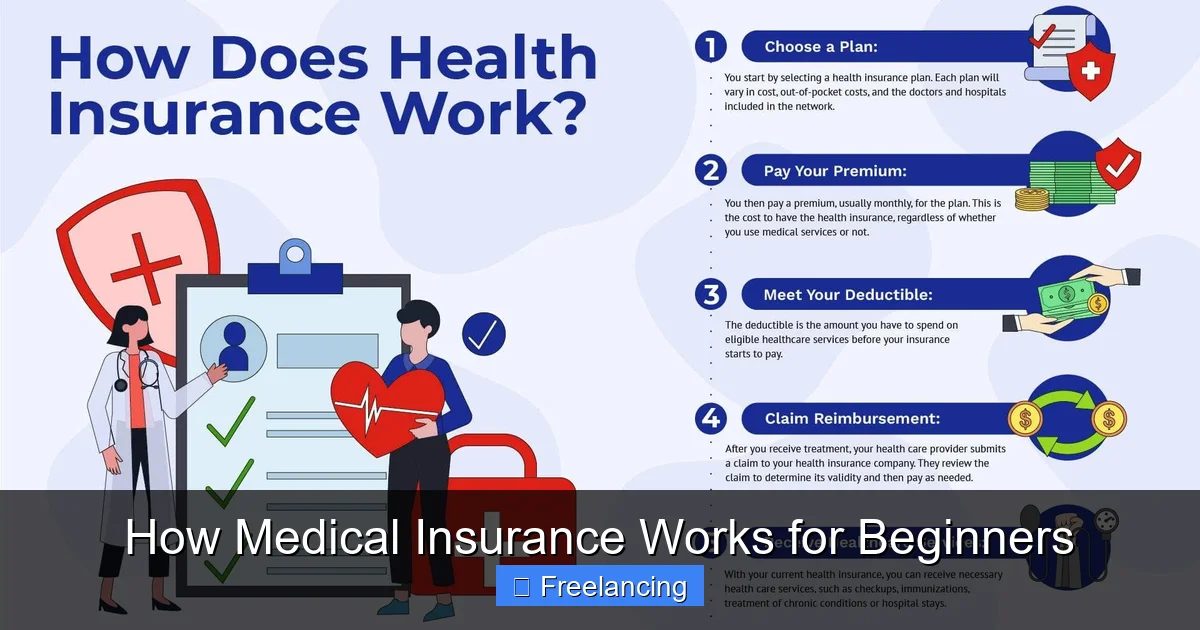

At its core, medical insurance is a contract between you and an insurance company. You pay a monthly fee (called a premium), and in return, the insurer agrees to help pay for your medical expenses. Think of it like a safety net. When you get sick, injured, or need preventive care, the insurance helps cover the cost—so you don’t have to pay the full price out of your own pocket.

Visual guide about How Medical Insurance Works for Beginners

Image source: infografolio.com

How Does It Actually Work?

Let’s say you break your wrist and go to the emergency room. Without insurance, you might be stuck with a bill for thousands of dollars. With insurance, the hospital sends the bill to your insurer. The company reviews it and pays a portion based on your plan. You then pay what’s left—but usually, it’s much less than the full amount.

But here’s the catch: insurance doesn’t cover everything right away. There are rules—like deductibles, copays, and networks—that determine how much you pay and when. That’s why understanding how medical insurance works is so important.

The Basic Parts of a Medical Plan

Every health insurance plan has a few key parts that affect how much you pay and what’s covered. Let’s go through them one by one.

Visual guide about How Medical Insurance Works for Beginners

Image source: pennriseadvisors.com

Premiums

A premium is the amount you pay every month for your insurance—no matter if you use it or not. For example, if your premium is $300 a month, you’ll pay $300 each month to stay covered. Premiums vary based on your age, location, plan type, and whether you’re buying individual or family coverage.

As a freelancer, your premium might be higher than if you had employer-sponsored insurance. But that’s okay—it’s part of the trade-off for flexibility. The key is to pick a premium you can afford without sacrificing your health.

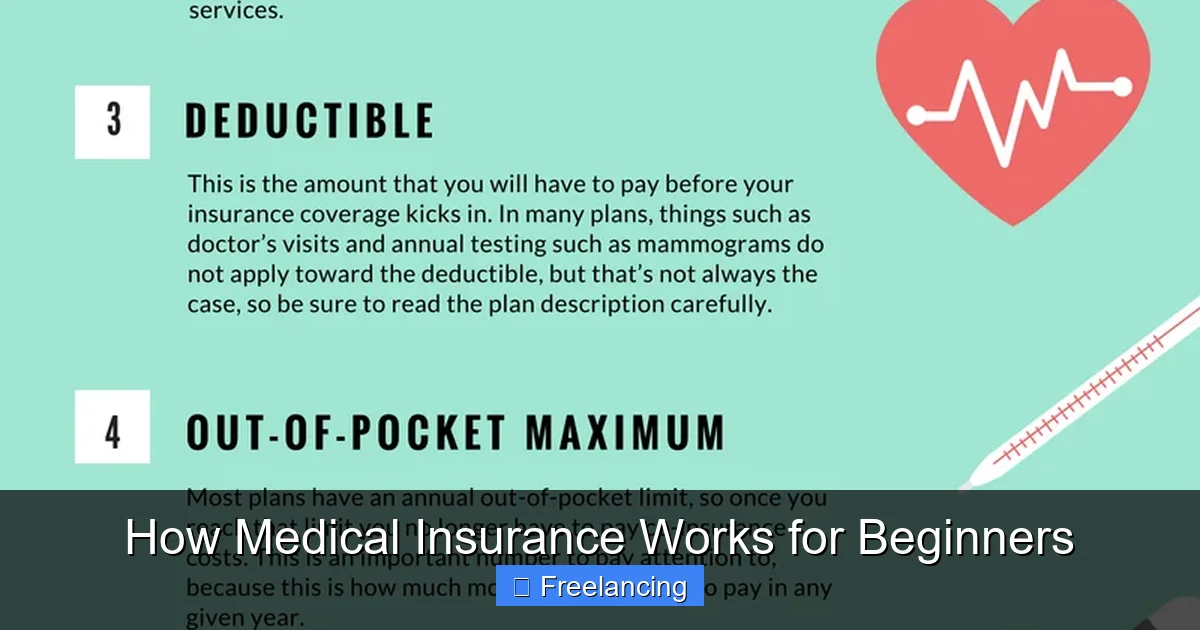

Deductibles

A deductible is the amount you pay for medical services before your insurance starts to cover anything. Let’s say your deductible is $2,000. That means you’ll pay full price for all your medical expenses—doctor visits, tests, prescriptions—until you’ve spent $2,000. Only after that does your insurance kick in.

For example: You go to the doctor twice in one year. Each visit costs $150. After two visits, you’ve paid $300. You still haven’t met your $2,000 deductible, so you pay the full amount. But if you had a $500 surgery, you’d pay the first $2,000 of that cost. Only the amount over $2,000 would be covered by insurance.

Plans with lower deductibles usually have higher premiums. High-deductible plans have lower premiums but require you to pay more upfront.

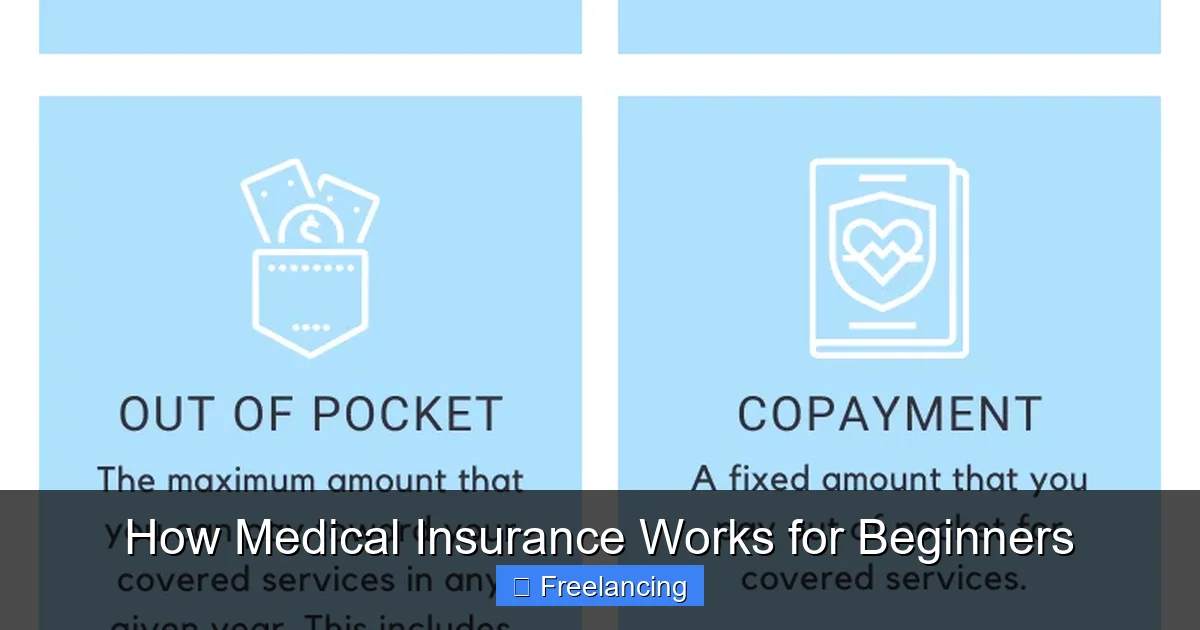

Copays and Coinsurance

Once you meet your deductible, you may still have to pay something for medical services. This is where copays and coinsurance come in.

- Copay: A fixed amount you pay for a specific service, like $20 for a doctor’s visit or $10 for a prescription.

- Coinsurance: A percentage of the cost you pay after your deductible. For example, your plan might cover 80% of a procedure, so you pay 20%.

Let’s say you have a $1,000 surgery. Your deductible is $2,000, so you pay the full $1,000. But next year, you meet your deductible early. Now, your insurance covers 80% of the $1,000, so you pay just $200.

Out-of-Pocket Maximum

Your out-of-pocket maximum is the most you’ll ever have to pay in a year for covered services. Once you hit that limit, your insurance covers 100% of most medical costs for the rest of the year.

For example, if your out-of-pocket max is $5,000 and you’ve already paid $4,800 this year, a $10,000 hospital bill would be fully covered. You’d only be responsible for the remaining $200.

This protects you from financial disaster if you have a serious illness or injury.

Types of Medical Insurance Plans

Not all health insurance plans are the same. There are several types, each with different rules and costs. Here are the most common ones for individuals and freelancers.

Visual guide about How Medical Insurance Works for Beginners

Image source: alliancehealth.com

HMO (Health Maintenance Organization)

HMO plans require you to pick a primary care physician (PCP) and get referrals to see specialists. You must use doctors and hospitals within the HMO’s network—except in emergencies. These plans usually have lower premiums and out-of-pocket costs, but less flexibility.

Example: You have an HMO plan. You need to see a cardiologist. You must first visit your PCP, who gives you a referral. If you go directly to the cardiologist without a referral, the insurance won’t cover it.

PPO (Preferred Provider Organization)

PPO plans give you more freedom. You can see any doctor or specialist without a referral. You can go in-network for lower costs or out-of-network for higher costs (but still some coverage). PPOs usually have higher premiums than HMOs.

Example: You have a PPO. You want to see a dermatologist. You can book an appointment directly—no referral needed. If you go in-network, your bill is lower. If you go out-of-network, you pay more, but the insurance still helps.

EPO (Exclusive Provider Organization)

EPO plans are like a mix of HMO and PPO. You usually can’t see out-of-network doctors except in emergencies. But you don’t need referrals to see specialists. Premiums are often lower than PPOs.

HDHP (High-Deductible Health Plan)

HDHPs have lower premiums but high deductibles—often $1,500 or more for individuals. These plans are often paired with a Health Savings Account (HSA), where you can save pre-tax money for medical expenses.

Tip: If you’re young and healthy, an HDHP with an HSA might save you money. You pay less each month and can grow tax-free savings for future medical needs.

How to Choose the Right Plan

Choosing a health insurance plan can feel overwhelming. But if you follow these steps, you’ll make a smart choice.

Assess Your Health Needs

Ask yourself: How often do you visit the doctor? Do you take regular prescriptions? Do you have a chronic condition like diabetes or asthma? If you’re generally healthy and only need occasional care, a high-deductible plan might work. If you have ongoing medical needs, a lower-deductible plan could save you money in the long run.

Compare Premiums and Deductibles

Look at the total cost—not just the premium. A plan with a $200 monthly premium and $1,000 deductible might cost $3,400 a year. Another with a $350 premium and $2,500 deductible could cost $6,700. Calculate both and see which fits your budget.

Check the Network

Make sure your doctors, specialists, and hospitals are in-network. Use your insurer’s directory to verify. Going out-of-network can double or triple your costs.

Review Prescription Coverage

If you take regular medications, check if they’re covered and how much you’ll pay. Some plans have tiered drug coverage—generic drugs cost less, brand names cost more.

Use a Health Insurance Marketplace

In the U.S., you can shop for plans on Healthcare.gov during open enrollment (usually November–January). If you’re eligible for subsidies based on income, you may qualify for lower premiums.

Medical Insurance for Freelancers

As a freelancer, you don’t have employer-sponsored insurance. That means you’re responsible for finding and paying for your own coverage. But that also gives you more control—and more responsibility.

Options for Self-Employed Individuals

- Marketplace Plans: Buy individual plans through Healthcare.gov or your state exchange. You may qualify for tax credits if your income is under $58,310 (individual) or $97,200 (family).

- Private Insurers: Some companies sell plans directly to individuals. Compare them with marketplace options.

- Group Plans: Join a professional association or co-op to access group rates.

Health Savings Account (HSA) for Freelancers

If you have an HDHP, you can open an HSA. You contribute pre-tax money (up to $4,300 in 2024 for individuals), grow it tax-free, and use it for medical expenses. The money rolls over year after year—even if you change jobs.

Example: You contribute $300 a month to your HSA ($3,600 a year). You use $2,000 for dental work and $1,000 for prescriptions. You still have $600 left for next year.

COBRA and Other Continuation Coverage

If you lose a job, COBRA lets you keep your employer’s plan for up to 18 months—but you pay the full premium (employer + employee share). It’s expensive, but it’s an option while you look for new coverage.

Understanding Your Insurance Card and ID

Once you have a plan, you’ll get an insurance card. It shows your member ID, group number, and plan details. Always carry it or have it on your phone. You’ll need it when visiting doctors, hospitals, or pharmacies.

What to Do If You Lose Your Card

Call your insurer or log into your online account to request a replacement. Some insurers let you print a temporary card online.

Know Your Plan’s Customer Service Number

Keep your insurer’s phone number handy. If you have questions about coverage, claim denials, or network changes, call them. Don’t wait until you’re sick to find out how to use your plan.

Common Mistakes Beginners Make

Even smart people make mistakes when they first get insurance. Here are the most common ones—and how to avoid them.

Not Reading the Summary of Benefits

Every plan has a Summary of Benefits and Coverage (SBC). It explains what’s covered, what’s not, and how much you’ll pay. Read it before signing up.

Forgetting to Check the Network

Going out-of-network can cost hundreds or thousands more. Always confirm your doctor is in-network before making an appointment.

Waiting Until You’re Sick to Enroll

Most plans have a 30-day enrollment window after open enrollment ends. If you miss it, you might have to wait a year for coverage—unless you have a qualifying life event (like getting married or having a baby).

Not Using Preventive Care

Many plans cover preventive services like flu shots, mammograms, and annual checkups at no cost. Use them—they’re free and keep you healthy.

Not Reviewing Your Plan Annually

Your health and budget change. Review your plan every year during open enrollment. Maybe your needs have changed, or a new plan is cheaper.

How to Save Money on Medical Insurance

Health insurance can be expensive—but there are ways to save.

Use In-Network Providers

Staying in-network can cut your costs by 30–50%. Use your insurer’s directory to find approved doctors and hospitals.

Shop Around for Prices

Some services, like MRIs or blood tests, can vary in price by hundreds of dollars. Call a few places and compare. You can even ask your doctor’s office to help you find the best price.

Use Generic Medications

Generic drugs cost less and are just as safe. Ask your doctor if a generic version is available.

Take Advantage of HSAs

If you have an HDHP, contribute to an HSA. The money is tax-free and grows over time. It’s like a savings account for your health.

Preventive Care Is Free

Get your annual checkup, vaccines, and screenings without paying anything out of pocket. It’s one of the best ways to avoid bigger medical bills later.

Conclusion: You’ve Got This

Medical insurance might seem complicated at first, but it’s really just a tool to protect you. It helps you pay for health care without going broke. Whether you’re freelancing, starting a new job, or just trying to understand your options, knowing how medical insurance works puts you in control.

Remember: premiums, deductibles, copays—they’re just parts of the puzzle. The bigger picture is peace of mind. You’re covered when you need it most. You’re not alone when you’re sick. And you’re smart for taking the time to learn.

So take it step by step. Compare plans. Ask questions. Use your HSA. And don’t be afraid to call your insurer if something doesn’t make sense. That’s what they’re for.

You’ve got this. And now, so do you.

Frequently Asked Questions

What happens if I don’t have medical insurance?

Without insurance, you’ll pay the full cost of medical services out of pocket. This can lead to high bills for doctor visits, emergencies, or chronic care. Some states require health insurance, and not having it may result in fines (though federal penalties were lifted after 2019).

Can I change my medical insurance plan anytime?

No, you can only change plans during open enrollment (usually November to January) or if you have a qualifying life event like getting married, having a baby, or losing another job. Otherwise, you must wait for the next enrollment period.

Is medical insurance the same as health insurance?

Yes, “medical insurance” and “health insurance” are often used interchangeably. Both refer to coverage that helps pay for medical services like doctor visits, hospital stays, and prescriptions.

Do I need to pay for prescriptions even with insurance?

It depends on your plan. Many plans require you to pay a copay or coinsurance for prescriptions, especially after meeting your deductible. Check your formulary (drug list) to see what’s covered and how much you’ll pay.

What is a network, and why does it matter?

A network is a group of doctors, hospitals, and clinics that have agreed to provide services at lower rates. Using in-network providers usually saves you money. Going out-of-network may result in higher costs or no coverage at all.

Can I use my medical insurance while traveling?

Yes, most plans cover you anywhere in the U.S., even when traveling. For international travel, check if your plan offers emergency coverage abroad—some don’t. Consider travel insurance for extra protection.