Family medical insurance plans that save money aren’t just a safety net—they’re a smart financial decision. By choosing the right plan, you can cut healthcare costs without sacrificing coverage. With rising medical expenses, now more than ever, families need affordable yet comprehensive insurance options that balance protection and affordability.

Key Takeaways

- Preventive care is free: Many plans cover annual checkups, vaccines, and screenings at no extra cost, helping you catch health issues early and avoid expensive treatments later.

- Family discounts apply: Insurers often offer lower premiums when you add all family members, making group plans more affordable than individual policies.

- High-deductible plans save cash: HDHPs come with lower monthly premiums and let you save in an HSA for tax-free medical expenses.

- Network doctors save money: Staying in-network keeps costs down and ensures full coverage, avoiding surprise bills from out-of-network providers.

- Compare plans annually: Health needs and costs change yearly—reviewing your plan each fall helps you find better deals and avoid coverage gaps.

- Use wellness programs: Many insurers offer free fitness, mental health, and smoking cessation programs that improve health and reduce long-term costs.

- Tax credits can lower costs: If your income qualifies, you may get government subsidies to make family insurance more affordable through the Health Insurance Marketplace.

📑 Table of Contents

- Why Family Medical Insurance Plans That Save Money Matter

- Understanding How Family Medical Insurance Works

- Types of Family Medical Insurance Plans That Save Money

- How to Compare Family Medical Insurance Plans That Save Money

- Money-Saving Tips for Family Medical Insurance

- Common Mistakes to Avoid When Choosing Family Insurance

- Real-Life Example: How a Family Saved $3,000 a Year

- How to Enroll in a Family Medical Insurance Plan That Saves Money

- Conclusion: Protect Your Family Without Breaking the Bank

Why Family Medical Insurance Plans That Save Money Matter

Let’s face it—healthcare costs are climbing. A single emergency room visit can easily top $1,000. Now imagine that happening to multiple family members. Without proper coverage, one illness or injury could put your family in serious financial trouble. That’s why finding family medical insurance plans that save money isn’t just smart—it’s essential.

The good news? You don’t have to choose between being broke and being covered. Today’s insurance market offers a variety of affordable options designed specifically for families. These plans help you protect your loved ones while keeping your budget intact. Whether you’re a young parent, a growing family, or someone managing aging relatives, there’s a plan that fits your needs—and your wallet.

In this guide, we’ll walk you through how to find, compare, and choose the best family medical insurance plans that save money. From understanding deductibles to using health savings accounts, we’ll cover everything you need to know to make informed decisions. By the end, you’ll feel confident selecting a plan that offers real value without breaking the bank.

Understanding How Family Medical Insurance Works

Visual guide about Family Medical Insurance Plans That Save Money

Image source: insuracarelife.com

Before jumping into plan types, it’s important to understand the basics. Family medical insurance is a policy that covers multiple people under one contract—usually the policyholder, spouse, and dependent children. These plans bundle coverage so you don’t need separate policies for each person.

What’s Included in a Family Plan?

Most family medical insurance plans cover:

- Doctor visits (primary care and specialists)

- Hospital stays and surgeries

- Prescription medications

- Maternity and newborn care

- Mental health services

- Preventive care (like vaccinations and screenings)

- Emergency services

Some plans also include extras like dental, vision, or hearing coverage. Always check the details to know exactly what’s covered.

How Premiums Work

The premium is the amount you pay monthly for the plan—even if you don’t use medical services. Family plans usually have higher premiums than individual ones because they cover more people. However, insurers often give family discounts, so adding everyone can still be cheaper than buying separate policies.

For example, a family of four might pay $1,200 per month total—compared to $400 each for individual plans. That’s a big difference, especially over a year.

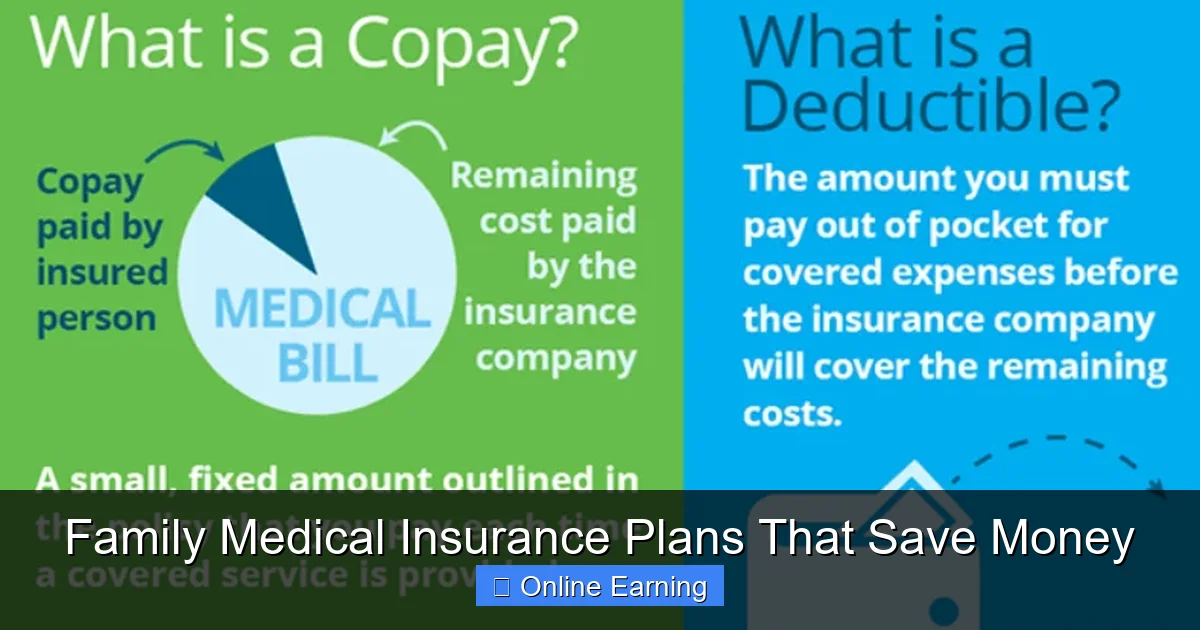

Deductibles, Copays, and Out-of-Pocket Maximums

These are the three main cost-sharing terms you’ll see:

- Deductible: The amount you pay before insurance kicks in. For example, a $5,000 family deductible means the family pays the first $5,000 in medical costs.

- Copay: A fixed fee for certain services, like $30 for a doctor’s visit.

- Out-of-pocket maximum: The most you’ll pay in a year. After that, insurance covers 100% of covered services.

Understanding these helps you compare plans fairly. A lower deductible might sound better, but it often means higher premiums. The best plan balances all three.

Types of Family Medical Insurance Plans That Save Money

Visual guide about Family Medical Insurance Plans That Save Money

Image source: i.ytimg.com

Not all insurance plans are created equal. Some are better for saving money, depending on your family’s health and budget. Let’s look at the most cost-effective options.

High-Deductible Health Plans (HDHPs)

HDHPs have lower monthly premiums and higher deductibles. For example, a family plan might cost $600/month with a $7,000 deductible. But once you meet the deductible, you get great coverage.

The real money-saving feature? You can open an HSA (Health Savings Account). Contributions are tax-deductible, the money grows tax-free, and withdrawals for medical expenses are tax-free too. That’s triple tax savings!

Many families use HSAs like a medical savings account. They save money monthly and build a fund for future care. Plus, unused HSA funds roll over year after year.

Preferred Provider Organization (PPO) Plans

PPOs offer flexibility. You can see any doctor, but you save the most when using in-network providers. Out-of-network care is still covered, but at a higher cost.

For families that want choice and don’t mind paying a bit more for peace of mind, PPOs are a solid pick. They’re especially useful if you travel often or need specialists.

Health Maintenance Organization (HMO) Plans

HMOs require you to pick a primary care doctor and get referrals for specialists. You must stay in-network for full coverage.

The trade-off? Lower premiums and out-of-pocket costs. HMOs are ideal for families who prefer a streamlined system and don’t need to see out-of-network doctors.

Catastrophic Plans (for Young Families)

Available to people under 30 or those with hardship exemptions, catastrophic plans have very low premiums—but high deductibles (usually $10,000+ for families). They’re designed to protect against worst-case scenarios, not routine care.

These aren’t for everyone, but they can be a lifeline for young families starting out. Just make sure you have savings to cover everyday medical needs.

Employer-Sponsored Family Plans

Many employers offer group health insurance with shared costs. You might pay only 10–20% of the premium, with the employer covering the rest.

This is often the most affordable way to get family coverage. Plus, contributions are usually made pre-tax, lowering your taxable income.

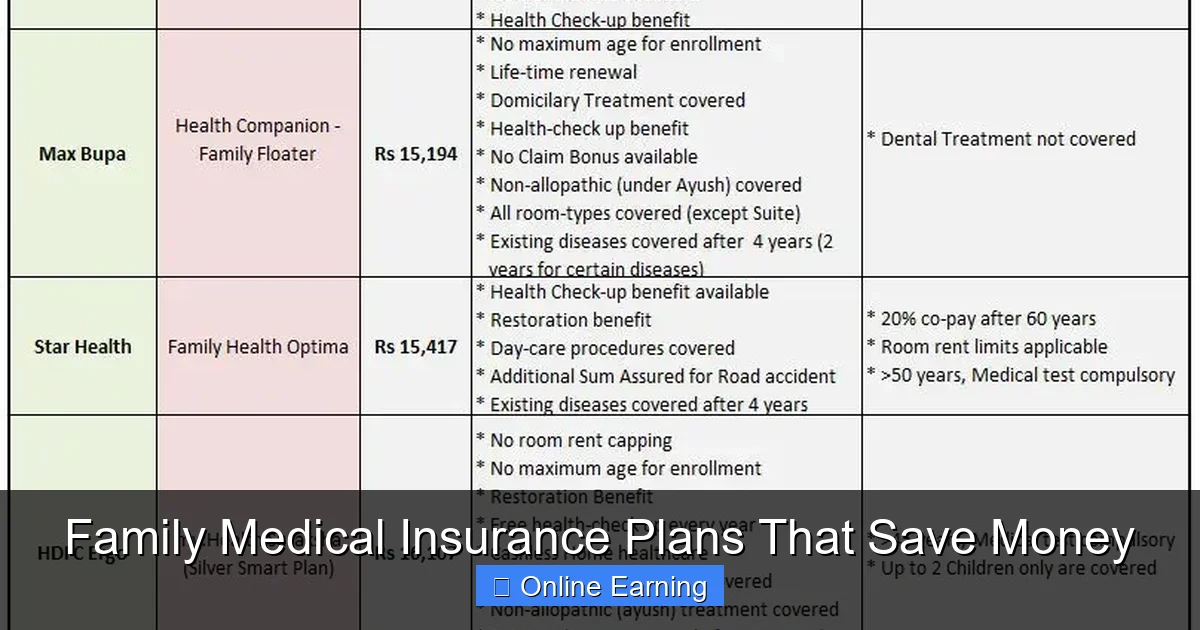

How to Compare Family Medical Insurance Plans That Save Money

Visual guide about Family Medical Insurance Plans That Save Money

Image source: relakhs.com

Shopping for insurance can feel overwhelming. But with a clear process, you can find the best plan for your family.

Step 1: Gather Your Family’s Health History

List everyone’s medical needs. Does someone have chronic conditions like diabetes? Are there kids who need frequent pediatric visits? This helps you estimate how much coverage you’ll actually use.

For example, if your teen plays sports, look for plans with good emergency and orthopedic coverage.

Step 2: Check the Network

Make sure your family’s doctors, hospitals, and pharmacies are in-network. Going out-of-network can double or triple your costs.

Use the insurer’s provider directory online or call customer service to confirm.

Step 3: Compare Deductibles and Out-of-Pocket Limits

Look at both the deductible and the maximum you’d pay in a year. A plan with a $3,000 deductible and a $10,000 out-of-pocket max might be better than one with a $1,000 deductible and a $15,000 max—even if the premiums are higher.

Use online calculators to estimate your total annual costs.

Step 4: Review Prescription Coverage

If your family takes regular medications, check the formulary (list of covered drugs). Some plans cover generics well but charge more for brand names.

Look for plans with tiered pricing and mail-order options to save on prescriptions.

Step 5: Look for Extra Benefits

Many plans offer free or low-cost extras:

- Telehealth visits

- Mental health counseling

- Fitness memberships

- Smoking cessation programs

These can improve your family’s health and reduce long-term costs.

Step 6: Use Online Tools and Compare Quotes

Websites like Healthcare.gov, eHealth, or private brokers let you compare plans side by side. Enter your ZIP code, family size, and income to see personalized options.

Don’t forget to check if you qualify for tax credits or subsidies through the Marketplace. These can cut your premium by hundreds or even thousands of dollars.

Money-Saving Tips for Family Medical Insurance

Even with the best plan, you can save more with smart habits.

Use Preventive Care Without Cost

Under the Affordable Care Act, most plans cover preventive services at 100%. That includes:

- Annual physicals

- Vaccines (flu, HPV, etc.)

- Blood pressure and cholesterol checks

- Breast and colon cancer screenings

Schedule these regularly. Catching health issues early saves money and lives.

Shop Around for Prescriptions

Pharmacies like Walmart, Costco, or online services often have lower prices. Use apps like GoodRx to compare costs at different stores.

Also, ask your doctor about generic alternatives. They work just as well and cost less.

Use Telehealth for Minor Issues

Virtual visits cost less than in-person appointments. Most plans cover them at the same rate as office visits.

Perfect for colds, rashes, or follow-ups—saving time and money.

Keep Track of Medical Expenses

Use a spreadsheet or app to log deductibles, copays, and HSA contributions. This helps you know exactly how much you’ve paid and when your benefits reset.

It also makes tax time easier.

Review Your Plan Each Year

Life changes—new baby, job loss, moving. These affect your insurance needs. Open enrollment (usually November–December) is the best time to switch plans.

Don’t forget to check if your income still qualifies you for subsidies.

Consider a Health Savings Account (HSA)

If you have an HDHP, open an HSA. Contribute as much as possible—especially if your employer matches. Use it for qualified medical expenses now or save it for retirement.

HSAs are one of the few tax-advantaged accounts available to everyone.

Common Mistakes to Avoid When Choosing Family Insurance

Even smart families make costly insurance mistakes. Here’s how to avoid them.

Mistake 1: Choosing Based on Premiums Alone

A low premium might sound great, but if the deductible is $20,000, you could pay more in the long run. Always compare total annual costs.

Mistake 2: Not Checking the Network

Going out-of-network can wipe out your savings. Confirm your doctors are included before enrolling.

Mistake 3: Ignoring Prescription Needs

If your family takes regular meds, a plan with poor drug coverage could cost thousands more. Always review the formulary.

Mistake 4: Forgetting to Use Preventive Care

Skipping free checkups means missing early warnings. Use your plan’s preventive benefits fully.

Mistake 5: Not Updating the Plan When Life Changes

Marriage, birth, job change—these all affect your coverage needs. Update your plan within 30 days of a qualifying event.

Mistake 6: Overlooking Employer Benefits

If your employer offers insurance, compare it to Marketplace plans. Sometimes the group plan is cheaper—even with subsidies.

Real-Life Example: How a Family Saved $3,000 a Year

Meet the Johnsons—a family of four in Ohio. They were paying $1,400/month for a PPO plan with a $4,000 deductible. When the youngest child got asthma, their costs skyrocketed.

They switched to an HDHP with an HSA. The new premium was $700/month—saving $8,400 a year. They contributed $4,000 to the HSA (tax-deductible), and used it for asthma treatments and doctor visits.

By using telehealth, shopping for generics, and scheduling preventive care, they stayed within their budget. In two years, they had $6,000 in their HSA for future needs.

This shows how smart choices can lead to real savings.

How to Enroll in a Family Medical Insurance Plan That Saves Money

Getting started is easy.

Step 1: Visit Healthcare.gov

This is the official U.S. government site for health insurance. It’s secure and offers personalized plans.

Step 2: Enter Your Information

You’ll need:

- ZIP code

- Family size

- Income (for subsidy eligibility)

- Employer details (if applicable)

Step 3: Review and Compare Plans

See side-by-side comparisons of premiums, deductibles, and benefits. Use the “Compare” tool to highlight savings.

Step 4: Choose Your Plan

Click “Enroll” and follow the steps. You’ll get a confirmation within minutes.

Step 5: Pay Your First Premium

Pay online, by phone, or by mail. Coverage starts the first day of the next month.

Step 6: Keep Records

Save your enrollment confirmation, plan ID card, and payment receipt. You’ll need these for claims and tax filing.

Conclusion: Protect Your Family Without Breaking the Bank

Finding family medical insurance plans that save money is not about choosing the cheapest option—it’s about choosing the smartest one. It’s about balancing cost, coverage, and peace of mind.

With rising healthcare costs, having the right plan can mean the difference between financial stress and security. By understanding your options, comparing carefully, and using every benefit, you can protect your loved ones without draining your savings.

Remember: insurance is an investment. It pays for itself when you avoid a single costly emergency. And with tools like HSAs, preventive care, and subsidies, you can stretch every dollar further.

Take control today. Compare plans, ask questions, and make a choice that keeps your family healthy and your wallet happy.

Frequently Asked Questions

What is the best family medical insurance plan for saving money?

The best plan depends on your family’s needs. High-deductible health plans (HDHPs) with HSAs often save the most money due to lower premiums and tax advantages. PPOs offer flexibility, while HMOs provide affordability for those who don’t need out-of-network care.

Can I get family insurance if I’m self-employed?

Yes, self-employed individuals can buy family medical insurance through the Health Insurance Marketplace or private insurers. You may qualify for tax credits to lower your premium based on income.

How much does family medical insurance typically cost?

Family plans average $1,200–$2,000 per month, depending on location, age, and coverage level. HDHPs are on the lower end, while PPOs and plans with low deductibles cost more. Subsidies can reduce this significantly.

Are pre-existing conditions covered?

Yes. Under the Affordable Care Act, insurers cannot deny coverage or charge more based on pre-existing conditions. All Marketplace plans must cover essential health benefits, including chronic condition management.

How do I know if I qualify for subsidies?

You may qualify if your household income is between 100% and 400% of the federal poverty level. Use the Healthcare.gov calculator to estimate your eligibility based on family size and income.

Can I change my plan during the year?

Only during open enrollment (usually November–December) or within 60 days of a qualifying life event (like marriage, birth, or job loss). Outside these times, you can’t make changes unless you qualify for a special enrollment period.