Finding affordable medical insurance in 2026 is more important than ever—especially for freelancers managing irregular income and high out-of-pocket costs. With rising premiums and evolving healthcare policies, it’s smart to explore options like short-term plans, association health plans, and government subsidies. You don’t need a full-time job to get quality, low-cost coverage—there are several practical, flexible solutions available.

Key Takeaways

- Freelancers can access affordable medical insurance through government marketplaces, association plans, and short-term options. These alternatives often cost less than traditional employer-sponsored plans and provide essential coverage.

- Subsidies and tax credits significantly reduce monthly premiums for low- and middle-income earners. In 2026, expanded eligibility under the Affordable Care Act (ACA) means more people qualify.

- Short-term health insurance plans offer budget-friendly options for temporary coverage needs. While not comprehensive, they can bridge gaps between jobs or waiting periods.

- Health Savings Accounts (HSAs) pair well with high-deductible plans to lower long-term healthcare costs. HSAs are tax-advantaged and ideal for freelancers managing cash flow.

- Comparing providers using tools like Healthcare.gov or state-run exchanges saves money and time. These platforms let you shop plans side by side with clear cost breakdowns.

- Local community health centers and nonprofit insurers offer sliding-scale fees for uninsured or underinsured individuals. These options are especially helpful in rural or high-cost areas.

- Staying informed about policy changes in 2026 is key to maximizing savings and coverage. Federal and state reforms may open new affordable pathways.

📑 Table of Contents

- Introduction: Why Affordable Medical Insurance Matters More Than Ever

- Understanding Your Options: The Big Picture

- 1. Affordable Marketplace Plans: Your Best Bet for Comprehensive Coverage

- 2. Short-Term Health Insurance: Flexible, Budget-Friendly Coverage

- 3. Association Health Plans (AHPs): Group Insurance for Freelancers

- 4. Health Savings Accounts (HSAs): Save Now, Pay Less Later

- 5. Local and Nonprofit Options: Community-Based Care

- 6. Catastrophic Plans: For the Young and Healthy

- Conclusion: Take Control of Your Health and Finances

- FAQs

Introduction: Why Affordable Medical Insurance Matters More Than Ever

Imagine this: you’re a freelance graphic designer, a digital marketer, or a consultant working from home. You set your own hours, take on your own clients, and enjoy the freedom of being your own boss. But here’s the catch—you don’t have access to employer-sponsored health insurance. And without it, a sudden illness or injury could mean not just medical bills, but lost income and financial stress. That’s why finding affordable medical insurance options in 2026 isn’t just a nice-to-have—it’s a necessity.

Fast forward to 2026, and the healthcare landscape continues to evolve. Premiums have stabilized slightly after years of volatility, but out-of-pocket costs remain high. For freelancers, the challenge is compounded by irregular income, making it hard to budget for monthly insurance payments. Yet, with the right knowledge and resources, securing affordable coverage is not only possible—it’s smarter than ever. Whether you’re just starting out or running a growing side hustle, understanding your options can save you thousands while keeping you protected.

In this guide, we’ll walk you through the most practical and cost-effective medical insurance solutions available to freelancers in 2026. From government-backed plans to niche alternatives, we’ll break down what each option offers, how to qualify, and how to pick the one that fits your lifestyle and budget. Let’s get started.

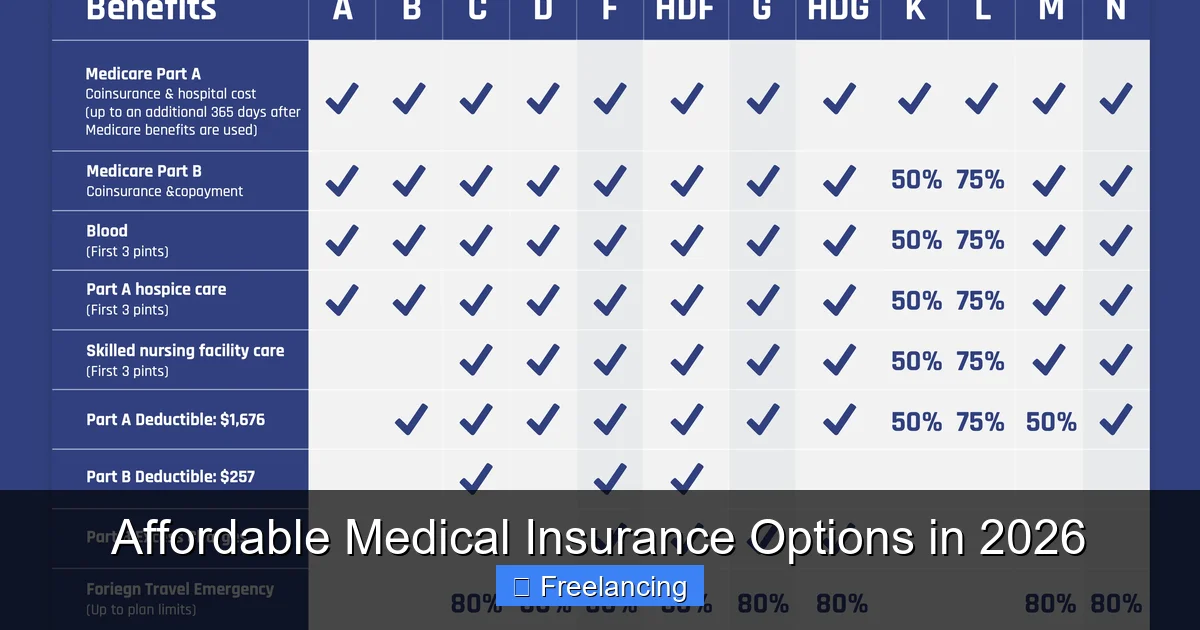

Understanding Your Options: The Big Picture

Before diving into specific plans, it’s important to understand the types of medical insurance available. For freelancers, the main categories include:

Visual guide about Affordable Medical Insurance Options in 2026

Image source: auntmarthas.org

- Marketplace Plans (ACA-compliant): Offered through Healthcare.gov or state exchanges, these plans meet the Affordable Care Act standards and include essential health benefits.

- Short-Term Health Insurance: Temporary coverage that can last up to 12 months (with renewals), ideal for gaps in employment.

- Association Health Plans (AHPs): Group plans available to members of professional associations or freelance networks.

- Health Sharing Ministries: Faith-based alternatives that pool funds for medical expenses, though not insurance.

- Medicaid and CHIP: Government programs for low-income individuals, available in most states.

- Catastrophic Plans: Low-premium plans with high deductibles, designed for young, healthy individuals.

Each has pros and cons, and the best choice depends on your income, health status, and how much risk you’re willing to take on. Let’s explore each in detail.

1. Affordable Marketplace Plans: Your Best Bet for Comprehensive Coverage

What Are Marketplace Plans?

Marketplace plans—also known as ACA plans—are government-regulated health insurance options available to individuals and small businesses. In 2026, the ACA continues to offer robust consumer protections, including no pre-existing condition exclusions, essential health benefits, and coverage for preventive care.

Visual guide about Affordable Medical Insurance Options in 2026

Image source: jclis.com

These plans are sold through the federal exchange (Healthcare.gov) or state-run marketplaces. You can browse and compare plans by cost, coverage, and provider network. Most importantly, if you qualify based on income, you may be eligible for premium tax credits and cost-sharing reductions that lower your monthly payments and out-of-pocket costs.

How to Qualify for Subsidies

Subsidies are the game-changer for freelancers. If your income is between 100% and 400% of the federal poverty level (FPL), you likely qualify for financial help. For example, if you earn $30,000 a year and live in a state with a benchmark Silver plan costing $500/month, you might only pay $100/month after subsidies.

To apply, visit Healthcare.gov during the open enrollment period (usually November to January). If you miss enrollment, you may qualify for a Special Enrollment Period due to life events like starting a freelance business.

Tips for Choosing a Marketplace Plan

- Compare metal tiers: Bronze plans are cheapest but have high deductibles; Platinum plans are most expensive but cover 90% of costs after deductible.

- Check the provider network: Make sure your preferred doctors and hospitals are in-network to avoid surprise bills.

- Use the plan comparison tool: Healthcare.gov lets you filter by premium, deductible, and out-of-pocket maximum.

For a freelancer earning $45,000/year, a Silver plan with subsidies could cost as little as $150/month—a fraction of what full-price plans cost.

2. Short-Term Health Insurance: Flexible, Budget-Friendly Coverage

What Is Short-Term Health Insurance?

Short-term health insurance is designed to provide temporary coverage—typically up to 3 months, though some states allow up to 12 months with renewals. These plans are not ACA-compliant, meaning they may exclude pre-existing conditions and essential health benefits like maternity care, mental health, and prescription drugs.

Visual guide about Affordable Medical Insurance Options in 2026

Image source: acko-cms.ackoassets.com

However, they’re incredibly affordable—often $50 to $150/month—making them ideal for freelancers between jobs, waiting for Medicare, or needing coverage while waiting for a new plan to take effect.

Pros and Cons

Pros:

- Lower monthly premiums

- Quick application and approval (sometimes in under 24 hours)

- No medical underwriting (though exclusions apply)

Cons:

- Does not cover pre-existing conditions

- Limited benefits and provider networks

- Not renewable indefinitely; may not cover emergency care

Who Should Consider It?

If you’re young, healthy, and need coverage for a short period (e.g., between freelance gigs), short-term plans can be a smart stopgap. Just don’t rely on them as your primary insurance long-term.

Example: A freelance writer in Texas pays $85/month for a short-term plan that covers urgent care and hospitalization, saving $200/month compared to a Bronze ACA plan—but only if they don’t need regular prescriptions or therapy.

3. Association Health Plans (AHPs): Group Insurance for Freelancers

What Are AHPs?

Association Health Plans allow freelancers, independent contractors, and small business owners to join together and access group health insurance rates. These plans are regulated at the state level but often offer broader networks and more affordable premiums than individual market plans.

In 2026, many professional associations—like the Freelancers Union, National Association of Independent Contractors, or industry-specific groups—offer AHPs to their members. These plans are not ACA-compliant, so they may lack certain benefits, but they’re a cost-effective way to get comprehensive coverage.

How to Join an AHP

- Find a reputable association that offers health plans in your state.

- Pay a membership fee (often $50–$200/year).

- Apply for the plan during open enrollment or special enrollment periods.

For example, the Freelancers Union offers a Silver-tier AHP in several states with premiums starting at $250/month—lower than individual market rates in high-cost areas.

Important Considerations

- Read the fine print: AHPs may have limited provider networks or higher deductibles.

- Verify the association’s legitimacy: Avoid scams by checking with your state insurance department.

- Compare with ACA plans: If you qualify for subsidies, a marketplace plan might still be cheaper.

4. Health Savings Accounts (HSAs): Save Now, Pay Less Later

What Is an HSA?

A Health Savings Account is a tax-advantaged savings account that works with high-deductible health plans (HDHPs). You contribute pre-tax dollars, and the funds can be used for qualified medical expenses—including deductibles, copays, prescriptions, and even some dental and vision costs.

In 2026, the HSA contribution limit for individuals is $4,150. If you’re 55 or older, you can add a $1,000 catch-up contribution.

Why HSAs Are Perfect for Freelancers

- Triple tax advantage: Contributions are tax-deductible, growth is tax-free, and withdrawals for medical expenses are tax-free.

- Portability: You keep the account even if you switch jobs or go freelance.

- Long-term savings: Unused funds roll over year after year, building a nest egg for future healthcare costs.

How to Get Started

- Enroll in a qualified HDHP (deductible of at least $1,600 for individuals in 2026).

- Open an HSA with a bank or financial institution.

- Contribute up to the annual limit and keep receipts for expenses.

Example: A freelancer earning $50,000 contributes $300/month to an HSA. Over 10 years, that’s $36,000 saved tax-free for future medical needs—plus the tax savings on contributions.

5. Local and Nonprofit Options: Community-Based Care

Community Health Centers

Federally funded community health centers offer medical, dental, and mental health services on a sliding fee scale based on income. These centers are available in urban, suburban, and rural areas and often accept uninsured patients.

Services may include primary care, lab tests, immunizations, and chronic disease management—all at reduced costs. Some centers also offer free or low-cost insurance enrollment assistance.

Nonprofit Insurance Providers

Some nonprofit organizations offer low-cost health plans tailored to freelancers and gig workers. For example, Health Republic Insurance in New York and Oscar Health in select states offer transparent pricing and digital tools to help freelancers manage their coverage.

These plans often include telehealth, wellness programs, and no-claim fees—making them attractive for cost-conscious individuals.

How to Find Local Resources

- Visit FindaHealthCenter.hrsa.gov to locate nearby clinics.

- Contact your state’s insurance department for a list of nonprofit insurers.

- Ask peers in freelance communities for recommendations.

6. Catastrophic Plans: For the Young and Healthy

What Are Catastrophic Plans?

Catastrophic health insurance is available to individuals under 30 or those who qualify for a hardship exemption. These plans have very low monthly premiums—often under $200/month—but come with high deductibles (minimum $9,100 in 2026 for individuals).

They cover three primary care visits per year before the deductible kicks in, and all essential health benefits after that. They’re designed for people who are generally healthy and want protection against major medical events.

Who Should Consider It?

If you’re young, rarely see a doctor, and want to avoid high premiums, a catastrophic plan can be a smart choice. Just be prepared to pay out-of-pocket for routine care.

Example: A 28-year-old freelance photographer pays $120/month for a catastrophic plan. If they get injured in an accident, the plan covers 100% of costs after the deductible—saving them from financial disaster.

Conclusion: Take Control of Your Health and Finances

Navigating medical insurance as a freelancer doesn’t have to be overwhelming. In 2026, there are more affordable and flexible options than ever before. Whether you choose a subsidized marketplace plan, a short-term solution, or a combination of HSAs and local care, the key is to act early, compare carefully, and choose what fits your lifestyle and budget.

Remember, health insurance is an investment in your peace of mind and financial stability. With the right plan, you can protect yourself from unexpected bills, maintain your independence, and keep more of your hard-earned income. Don’t wait until you’re sick to start looking—begin your search today and take the first step toward affordable, reliable coverage.

FAQs

Can freelancers get government subsidies for medical insurance in 2026?

Yes, freelancers can qualify for premium tax credits and cost-sharing reductions through Healthcare.gov if their income is between 100% and 400% of the federal poverty level. These subsidies can make coverage significantly more affordable.

Is short-term health insurance a good option for freelancers?

Short-term plans can be a budget-friendly option for freelancers needing temporary coverage between jobs or during income gaps. However, they don’t cover pre-existing conditions or essential health benefits, so use them cautiously.

How do I know if I qualify for a Health Savings Account?

You can open an HSA if you’re enrolled in a high-deductible health plan (HDHP) with a deductible of at least $1,600 for individuals in 2026. HSAs are ideal for freelancers who want to save tax-free for medical expenses.

Are association health plans regulated by the federal government?

No, AHPs are regulated at the state level and are not required to follow all ACA rules. While they can offer group rates, they may lack certain benefits and have limited provider networks.

What happens if I miss the open enrollment period?

You can usually enroll during a Special Enrollment Period if you experience a life event like getting married, having a baby, or losing other coverage. Missing open enrollment means waiting until the next cycle unless you qualify for an exception.

Can I use my HSA for non-medical expenses?

Yes, but you’ll pay income tax and a 20% penalty if you’re under 65. After age 65, you can withdraw funds tax-free for any reason without penalty—though income tax still applies to non-medical withdrawals.

Frequently Asked Questions

What is Affordable Medical Insurance Options in 2026?

Affordable Medical Insurance Options in 2026 is an important topic with many practical applications.