Comparing health insurance policies doesn’t have to be overwhelming. With the right approach, you can find a plan that fits your needs, budget, and lifestyle. This guide walks you through simple, effective steps to evaluate coverage, costs, and benefits so you can make confident, informed choices.

Key Takeaways

- Understanding How to Compare Health Insurance Policies Easily: Provides essential knowledge

📑 Table of Contents

- How to Compare Health Insurance Policies Easily

- Why Comparing Health Insurance Policies Matters

- Step 1: Assess Your Healthcare Needs

- Step 2: Understand Key Health Insurance Terms

- Step 3: Compare Plans Side by Side

- Step 4: Check the Provider Network

- Step 5: Evaluate Additional Benefits

- Step 6: Use Online Comparison Tools

- Step 7: Consider Financial Assistance

- Step 8: Read the Fine Print

- Common Mistakes to Avoid

- When to Seek Help

- Conclusion: Make Confident Choices with Ease

How to Compare Health Insurance Policies Easily

Choosing the right health insurance policy can feel like navigating a maze—especially when you’re bombarded with jargon, confusing terms, and endless plan options. Whether you’re shopping for yourself, your family, or your employees, making an informed decision is crucial. After all, health insurance is one of the most important investments you’ll make in your well-being and financial stability.

But here’s the good news: you don’t have to be a healthcare expert to compare health insurance policies easily. With a clear, step-by-step approach, you can cut through the noise and find a plan that truly works for you. In this comprehensive guide, we’ll walk you through everything you need to know—from understanding coverage types to using online tools, and even spotting red flags. By the end, you’ll feel confident and empowered to choose the best health insurance plan with ease.

So grab a notebook (or open a spreadsheet—your future self will thank you), and let’s dive in.

Why Comparing Health Insurance Policies Matters

Health insurance isn’t just about getting sick and needing care. It’s about peace of mind, financial protection, and access to quality healthcare when you need it most. Without proper coverage, a single emergency room visit can cost thousands of dollars. But with the right policy, you can avoid medical debt and focus on recovery instead.

Visual guide about How to Compare Health Insurance Policies Easily

Image source: imgeng.jagran.com

The Risks of Not Comparing Plans

Many people assume that the first plan they see is the best—or worse, they stick with the same plan year after year without reviewing it. This can lead to several problems:

- Overpaying: Premiums can rise annually, and if you’re on the wrong plan, you might be paying more than necessary for less coverage.

- Underinsuring yourself: A plan with a low premium might have high deductibles or narrow networks, leaving you vulnerable during a health crisis.

- Missing out on benefits: New plans often include improved coverage for mental health, telehealth, or preventive care—benefits you might not even know exist.

Regularly comparing health insurance policies ensures you’re getting the best value for your money and the care you deserve.

Step 1: Assess Your Healthcare Needs

Before you even start looking at plans, take a moment to reflect on your health situation. This will help you narrow down your options and avoid wasting time on plans that don’t fit your lifestyle.

Visual guide about How to Compare Health Insurance Policies Easily

Image source: compareinsurance.ie

Ask Yourself These Questions

- Do you have any chronic conditions (like diabetes or asthma) that require ongoing treatment?

- Are you planning to start a family or have a baby in the near future?

- Do you see a primary care doctor regularly?

- Do you take prescription medications?

- How often do you visit specialists or the emergency room?

- Do you travel frequently or live in a rural area with limited healthcare access?

Your answers will help you determine what kind of coverage you need—and what to prioritize when comparing health insurance policies.

Example: A Young Professional vs. a Family with Kids

Imagine two people: Alex, a 28-year-old who’s generally healthy and only visits the doctor once a year, and Maria, a 35-year-old mother of two who has a child with asthma and visits specialists monthly. Alex might do well with a high-deductible plan paired with a Health Savings Account (HSA), while Maria would likely benefit from a plan with lower out-of-pocket costs and strong pediatric coverage.

Tailoring your search to your personal needs makes the comparison process much easier.

Step 2: Understand Key Health Insurance Terms

Jargon can be intimidating, but once you know the basics, comparing health insurance policies becomes a lot simpler. Here are the most important terms to know:

Visual guide about How to Compare Health Insurance Policies Easily

Image source: trucompare.in

Premium

This is the amount you pay monthly for your insurance—regardless of whether you use medical services. Think of it as your membership fee.

Deductible

The amount you pay out of pocket before your insurance starts covering costs. For example, if your deductible is $1,500, you pay the first $1,500 of medical bills yourself.

Co-pay

A fixed amount you pay for a specific service, like $20 for a doctor’s visit. This usually applies after you’ve met your deductible.

Coinsurance

This is the percentage of costs you share with your insurer after meeting your deductible. For example, “80/20 coinsurance” means you pay 20% and the insurer pays 80%.

Out-of-Pocket Maximum

The most you’ll have to pay in a year for covered services. Once you hit this limit, your insurance pays 100% of covered costs.

Network

The group of doctors, hospitals, and clinics that have agreed to provide care at lower rates. Staying in-network saves you money.

Understanding these terms helps you compare plans fairly and avoid hidden costs.

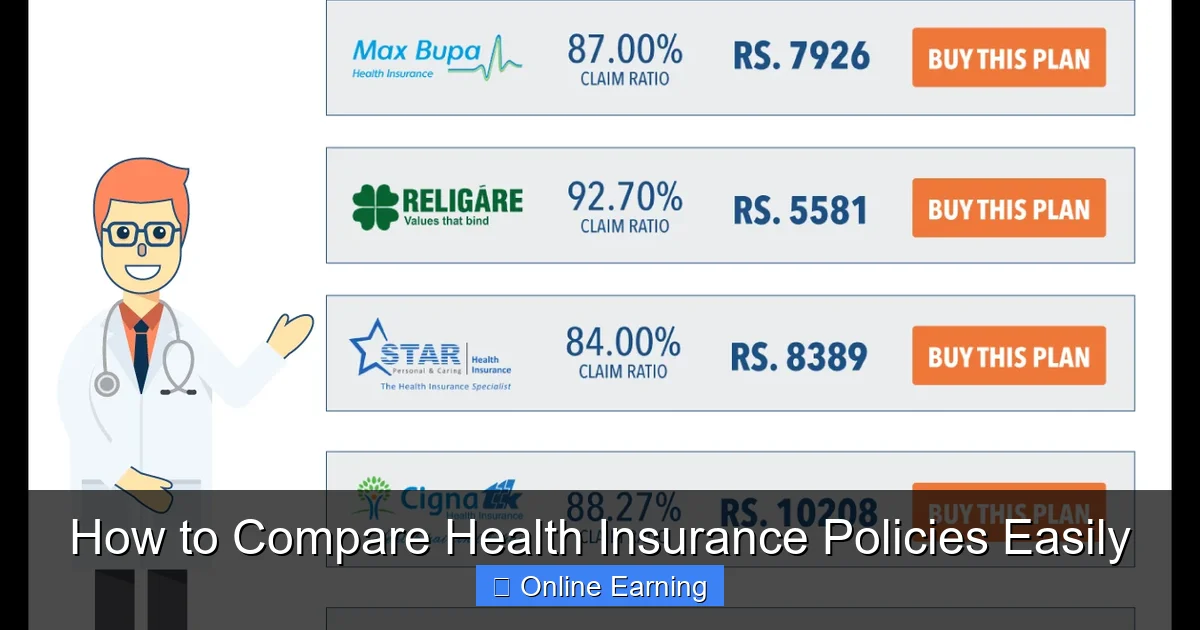

Step 3: Compare Plans Side by Side

Now that you know what to look for, it’s time to compare plans. The best way to do this is to create a simple comparison chart.

What to Include in Your Comparison Chart

- Plan name and type (HMO, PPO, EPO, or POS)

- Monthly premium

- Deductible (individual and family)

- Co-pays and coinsurance rates

- Out-of-pocket maximum

- Prescription drug coverage

- Maternity and newborn care

- Mental health and substance abuse services

- Preventive care (e.g., annual checkups, vaccinations)

- Telehealth availability

- Network size and provider access

Tip: Use Color Coding

Highlight your top choices in green, middle options in yellow, and plans to avoid in red. This visual method makes it easy to spot the best value at a glance.

Example Comparison Table

| Plan | Premium | Deductible | Co-pay | Out-of-Pocket Max | Network |

|---|---|---|---|---|---|

| Silver Plan A | $320/month | $1,800 | $25 | $6,000 | In-network only |

| Gold Plan B | $480/month | $500 | $10 | $3,500 | Open network |

| Bronze Plan C | $220/month | $5,000 | $50 | $9,000 | In-network only |

While Bronze has the lowest premium, its high deductible and out-of-pocket max make it risky if you need frequent care. Gold offers better value for someone who wants low out-of-pocket costs but pays more monthly.

Step 4: Check the Provider Network

Even if a plan looks great on paper, it’s no good if your doctor isn’t included. Always verify that your current healthcare providers are in-network.

How to Check Your Network

- Visit your insurer’s website and use their “Find a Doctor” tool.

- Search by name, specialty, or zip code.

- Confirm that your preferred hospital or clinic is listed.

Red Flags to Watch For

- Your primary care physician is no longer in-network.

- Specialists you rely on are not covered.

- You’d have to travel long distances for care.

If you’re considering a new doctor, check if they accept your insurance before making the switch.

Step 5: Evaluate Additional Benefits

Modern health insurance plans often include extras that can improve your health and convenience. Don’t overlook these when comparing policies.

Popular Value-Added Features

- Telehealth services: Virtual visits with doctors—great for minor issues or follow-ups.

- Mental health coverage: Therapy and counseling sessions with licensed professionals.

- Wellness programs: Gym discounts, smoking cessation support, or nutrition counseling.

- Prescription drug formulary: Check if your medications are covered and at what tier.

- Second opinion services: Access to specialists for complex diagnoses.

These perks can make a big difference in your overall experience and long-term health.

Step 6: Use Online Comparison Tools

Instead of manually researching each plan, use trusted online tools to compare health insurance policies quickly and accurately.

Top Resources

- Healthcare.gov: The official U.S. government marketplace for individual and family plans.

- eHealthInsurance: Offers side-by-side comparisons with customer reviews.

- Policygenius: Provides free quotes and expert advice.

- State-based exchanges: Some states have their own marketplaces with additional local options.

How to Use These Tools Effectively

- Enter your zip code and household details.

- Filter by metal tier (Bronze, Silver, Gold, Platinum) based on your budget and needs.

- Compare plans using the built-in comparison chart.

- Read customer reviews and star ratings.

- Check for subsidies or tax credits you may qualify for.

These platforms save time and help you avoid costly mistakes.

Step 7: Consider Financial Assistance

You might be eligible for help paying your premiums or reducing out-of-pocket costs—even if you think you make too much.

Types of Financial Aid

- Premium Tax Credits: Subsidies based on income to lower monthly payments.

- Cost-Sharing Reductions (CSRs): Lower deductibles and co-pays for lower-income individuals on Silver plans.

- Medicaid and CHIP: Free or low-cost coverage for low-income families and children.

- Employer-sponsored plans: Many employers offer subsidies or flexible spending accounts (FSAs).

During open enrollment, use the Health Insurance Marketplace calculator to estimate your savings.

Step 8: Read the Fine Print

Don’t skip the policy documents. While they’re long, they contain critical information that could save you from unexpected bills.

What to Look For

- Exclusions: Services not covered (e.g., cosmetic surgery, infertility treatments).

- Pre-existing conditions: How they’re handled under the plan.

- Appeals process: What to do if a claim is denied.

- Termination policy: When and how you can cancel or change your plan.

If something isn’t clear, contact the insurer or a licensed agent for clarification.

Common Mistakes to Avoid

Even with the best intentions, people make mistakes when comparing health insurance policies. Here are the most common ones—and how to avoid them.

Mistake 1: Choosing the Lowest Premium Only

A cheap plan might sound great, but if it has a $10,000 deductible, you could end up paying more in the long run. Always balance premium with out-of-pocket costs.

Mistake 2: Ignoring Network Changes

Insurers sometimes change their networks. A plan that worked last year might not include your doctor this year. Always double-check.

Mistake 3: Not Considering Future Needs

If you’re planning to have a baby or start a family, choose a plan with strong maternity coverage—even if you’re young and healthy now.

Mistake 4: Skipping Customer Service Reviews

Even the best plan is frustrating if the insurer has poor customer service. Read reviews on sites like Trustpilot or the Better Business Bureau.

Mistake 5: Forgetting to Re-evaluate Annually

Your health needs change. Life events like marriage, having a child, or a new job can affect your coverage needs. Review your plan every open enrollment period (usually November–January).

When to Seek Help

Comparing health insurance policies can be overwhelming, especially if you’re new to it. Don’t hesitate to get help.

Who Can Assist You

- Licensed insurance agents: They can explain plans and help you enroll.

- Navigators and brokers: Free or low-cost assistance through the Health Insurance Marketplace.

- HR departments: If you’re shopping for group coverage.

- Nonprofit organizations: Some offer free counseling for low-income individuals.

Remember, seeking help is a sign of smart decision-making—not weakness.

Conclusion: Make Confident Choices with Ease

Comparing health insurance policies doesn’t have to be a stressful, time-consuming ordeal. By following a clear, step-by-step process—assessing your needs, understanding key terms, comparing plans, and using trusted tools—you can find a plan that protects your health and wallet.

Take your time. Read carefully. Ask questions. And remember: the cheapest plan isn’t always the best—and the most expensive one isn’t always the most valuable either. It’s about finding the right balance of coverage, cost, and convenience for your unique situation.

With the knowledge in this guide, you’re now equipped to compare health insurance policies easily and confidently. Start today, and take the first step toward better health and financial peace of mind.

Frequently Asked Questions

How often should I compare health insurance plans?

You should compare health insurance policies every year during open enrollment (typically November to January). Life changes like marriage, having a child, or a new job can also be good reasons to re-evaluate your coverage.

Can I switch plans outside of open enrollment?

Yes, but only if you have a qualifying life event—such as getting married, having a baby, losing other coverage, or moving to a new area. These are called special enrollment periods.

What’s the difference between HMO, PPO, EPO, and POS plans?

HMOs require you to use in-network providers and get referrals for specialists. PPOs offer more flexibility to see out-of-network doctors at higher costs. EPOs cover in-network care and emergency services but usually don’t cover out-of-network care except in emergencies. POS plans combine features of HMOs and PPOs with referrals and network restrictions.

How do I know if a health insurance plan is right for me?

Consider your health needs, budget, preferred doctors, and how often you use medical services. A plan that fits your lifestyle and offers good value—not just low cost—is the right choice.

Are all health insurance plans the same?

No. Plans vary by premium, deductible, coverage limits, network size, and benefits. Even within the same insurance company, different plans (Bronze, Silver, Gold, Platinum) offer different levels of coverage and cost-sharing.

Can I get help comparing health insurance policies?

Absolutely. Licensed agents, navigators, and nonprofit organizations can provide free or low-cost assistance. You can also use government websites like Healthcare.gov or private comparison tools to get started.