Medical insurance deductibles are the amount you pay out-of-pocket before your insurance starts covering costs. Understanding how deductibles work can help you budget for healthcare and avoid unexpected bills. This guide breaks down everything you need to know about medical insurance deductibles, from what they are to how to minimize their impact.

Key Takeaways

- What is a deductible? A deductible is the amount you pay for covered healthcare services before your insurance begins to pay.

- How deductibles affect costs: You pay 100% of costs up to the deductible, then coinsurance or copays may apply depending on your plan.

- Types of deductibles: Understand individual, family, and out-of-network deductibles to avoid surprises.

- How to lower your deductible: Choose higher-premium plans, use in-network providers, or consider health savings accounts (HSAs).

- Timing matters: Some services (like preventive care) may be covered before meeting your deductible.

- Plan comparison: Compare deductibles across plans to find the best balance of cost and coverage.

- Stay informed: Review your plan annually and track your spending to stay on top of your deductible.

📑 Table of Contents

- Understanding Medical Insurance Deductibles: A Complete Guide

- What Is a Medical Insurance Deductible?

- Types of Deductibles: What You Need to Know

- How Deductibles Affect Your Healthcare Costs

- How to Lower Your Medical Insurance Deductible

- Common Misconceptions About Deductibles

- Real-Life Examples: How Deductibles Work in Action

- Tips for Managing Your Deductible as a Freelancer

- Conclusion: Take Control of Your Healthcare Costs

Understanding Medical Insurance Deductibles: A Complete Guide

Let’s face it—healthcare can be confusing. One of the most misunderstood parts of health insurance is the medical insurance deductible. If you’ve ever opened your insurance card and wondered, “Wait, what does that number mean again?”—you’re not alone. A deductible is simply the amount you’re expected to pay for covered services before your insurance kicks in. Think of it as the threshold you must clear before your plan starts sharing the cost.

Understanding how medical insurance deductibles work is crucial for managing your healthcare expenses. Whether you’re shopping for a new plan or trying to make sense of your latest medical bill, this guide will walk you through everything you need to know. From what a deductible really means to how you can reduce your out-of-pocket costs, we’ll make it simple and practical. By the end, you’ll feel confident navigating your health plan and making smarter decisions about your care.

What Is a Medical Insurance Deductible?

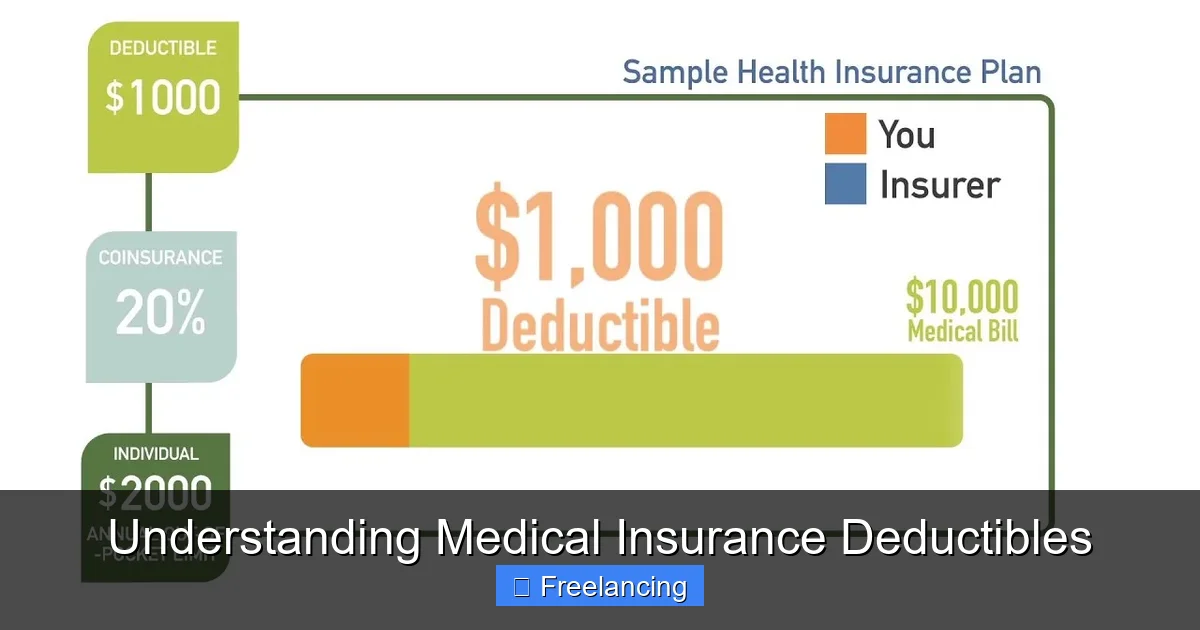

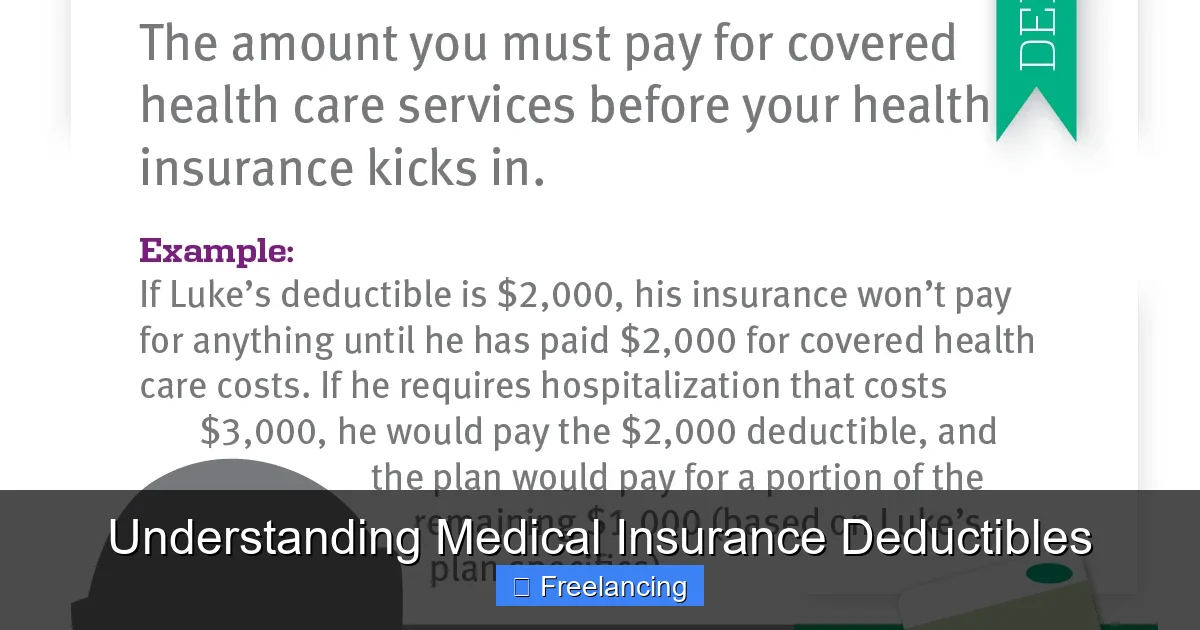

A medical insurance deductible is the amount of money you must pay for healthcare services before your insurance plan starts to cover costs. For example, if your deductible is $1,000, you’ll pay the first $1,000 of covered services yourself. After you meet your deductible, your insurance typically covers a portion of the remaining costs, depending on your plan’s coinsurance or copayment rules.

Visual guide about Understanding Medical Insurance Deductibles

Image source: blog.cdphp.com

How Deductibles Work in Practice

Imagine you visit the doctor for a routine checkup and get a blood test. Your plan covers these services, but since you haven’t met your deductible yet, you pay the full cost—say, $200. Once you’ve paid $1,000 in total for covered services throughout the year, your insurance starts covering 80% of the costs, and you’re responsible for the remaining 20%.

It’s important to note that not all services count toward your deductible. Preventive care, like annual physicals or vaccinations, is often covered in full before you meet your deductible. This is a key benefit of most health plans, designed to encourage early care and prevent bigger health issues down the road.

Types of Deductibles: What You Need to Know

Not all deductibles are created equal. Depending on your plan, you may encounter different types of deductibles that affect how and when you pay for care.

Visual guide about Understanding Medical Insurance Deductibles

Image source: aiainsurance.ca

Individual vs. Family Deductibles

Some plans have a single deductible for the entire family, while others apply separate deductibles to each person. For example, a family plan might require each family member to meet a $1,000 individual deductible before the plan starts paying. Once all family members have met their individual deductibles, the plan may cover services for everyone.

In contrast, a family deductible might be $3,000 total, meaning the family collectively needs to pay that amount before coverage begins. This can be more expensive if multiple family members use healthcare services early in the year.

In-Network vs. Out-of-Network Deductibles

Using in-network providers (those contracted with your insurance company) usually results in lower out-of-pocket costs. Some plans have separate deductibles for in-network and out-of-network care. If you go out-of-network, you might face higher deductibles and less coverage, even after meeting your deductible.

For example, your in-network deductible might be $1,000, but your out-of-network deductible could be $3,000. This encourages you to use in-network providers, where possible, to save money.

Embedded vs. Non-Embedded Deductibles

An embedded deductible means that the family deductible includes the deductibles of each individual family member. For instance, a family plan with a $3,000 embedded deductible might require each person to meet a $1,000 deductible before the plan starts paying for any family member.

A non-embedded deductible applies only to the total family amount. In this case, once the family reaches the $3,000 deductible, all services are covered regardless of how much each individual has paid. This can benefit families with high healthcare usage.

How Deductibles Affect Your Healthcare Costs

Understanding how medical insurance deductibles influence your spending is essential for budgeting and financial planning. The higher your deductible, the more you’ll pay upfront—but the lower your monthly premiums. This trade-off is a key factor when choosing a health plan.

Visual guide about Understanding Medical Insurance Deductibles

Image source: onemedical.com

High-Deductible vs. Low-Deductible Plans

A high-deductible health plan (HDHP) typically has lower monthly premiums but higher deductibles—often $1,500 or more for an individual. These plans are often paired with a health savings account (HSA), which lets you save pre-tax money to pay for qualified medical expenses.

On the other hand, a low-deductible plan has higher monthly premiums but lower out-of-pocket costs when you need care. These are better for people who expect frequent medical visits or high healthcare usage.

Coinsurance and Copayments After the Deductible

Once you meet your deductible, your plan usually covers a percentage of the remaining costs. This is called coinsurance. For example, your plan might cover 80% of the cost, and you pay the remaining 20%. Copayments (fixed amounts for specific services like doctor visits) may also apply after your deductible is met.

Let’s say your deductible is $1,000, and you’ve already paid $1,200. You then visit the ER for $2,000. Your plan covers 80% of the $2,000, which is $1,600, so you’re responsible for $400 (plus any copays or deductible carryover).

How to Lower Your Medical Insurance Deductible

While you can’t change your deductible once you’ve enrolled in a plan, you can take steps to reduce how much you pay toward it—or manage your spending more effectively.

Choose the Right Plan

When selecting a health plan, compare deductibles along with premiums, out-of-pocket maximums, and covered services. A plan with a higher deductible might save you money if you rarely use healthcare, but it could be risky if you have ongoing medical needs.

For freelancers or self-employed individuals, this is especially important. You don’t have employer-sponsored plans, so choosing wisely can save thousands over the year.

Use In-Network Providers

Sticking to in-network doctors, hospitals, and specialists can significantly lower your costs. Out-of-network care often comes with higher deductibles and lower coverage percentages. Check your insurance’s provider directory to stay in-network.

Take Advantage of Preventive Care

Most plans cover preventive services like screenings, vaccines, and annual checkups at no cost—even before you meet your deductible. Use these services regularly to stay healthy and avoid costly treatments later.

Set Up a Health Savings Account (HSA)

If you have a high-deductible health plan, an HSA allows you to save pre-tax dollars for medical expenses. Contributions are tax-deductible, and withdrawals for qualified expenses are tax-free. This can help you pay your deductible more easily and reduce your tax burden.

Track Your Medical Spending

Keep a log of your healthcare expenses throughout the year. This helps you stay aware of how much you’ve paid toward your deductible and plan for upcoming costs. Many insurance portals and apps make this easier by tracking your spending automatically.

Common Misconceptions About Deductibles

Even healthcare-savvy people get confused by medical insurance deductibles. Let’s clear up some myths.

Myth: Once You Meet Your Deductible, Everything Is Covered

False. Meeting your deductible doesn’t mean your insurance covers 100% of future costs. You’ll still pay coinsurance or copays until you reach your out-of-pocket maximum.

Myth: All Medical Expenses Count Toward Your Deductible

Not quite. Cosmetic procedures, out-of-network services (in some cases), and certain non-essential treatments may not count. Always check your plan’s summary of benefits.

Myth: You Have to Pay the Full Deductible in One Year

You pay toward your deductible throughout the year. Once the total reaches the deductible amount, your plan starts covering a share of future costs.

Myth: Deductibles Are the Same Across All Plans

Deductibles vary widely—from $0 to over $5,000—depending on your plan type, provider network, and employer. Always compare plans carefully.

Real-Life Examples: How Deductibles Work in Action

Let’s look at a few scenarios to see how medical insurance deductibles play out in real life.

Example 1: Routine Care and Preventive Services

Maria has a $1,500 deductible plan. She gets a flu shot and a physical. Both are preventive services, so she pays $0. Later, she sees her doctor for a sore throat. The visit costs $200, and she hasn’t met her deductible yet, so she pays the full $200. After paying $200, she’s still $1,300 away from meeting her deductible.

Example 2: Meeting the Deductible and Moving to Coinsurance

John has a $2,000 deductible plan. He gets a $1,500 MRI and a $800 doctor visit early in the year. He pays $2,300 total, meeting his deductible. Later, he has surgery costing $10,000. His plan covers 80%, so he pays 20% ($2,000) plus any copays.

Example 3: Family Plan with Embedded Deductibles

The Smith family has a plan with a $3,000 family deductible and $1,000 individual deductibles. Mom gets a $1,200 ER visit, Dad gets a $900 specialist visit, and their child has a $500 checkup. Each has met their individual deductible. The plan covers services for all three after the total family deductible is reached.

Tips for Managing Your Deductible as a Freelancer

As a freelancer, you don’t have the benefit of employer-sponsored health insurance, so managing your medical insurance deductible is even more important.

Shop Around for Affordable Plans

Use health insurance marketplaces or compare plans through brokers. Look for subsidies if you qualify based on income. A lower deductible might mean higher monthly costs, so find the balance that fits your budget.

Consider a High-Deductible Plan with an HSA

An HDHP paired with an HSA can be a smart choice. You pay lower premiums, save on taxes, and build a fund for future medical expenses. Just make sure you can afford the deductible if needed.

Use Telehealth Services

Many plans offer telehealth at low or no cost. This can help you avoid office visits and reduce costs, especially when you’re just starting to build up your deductible.

Plan Ahead for Major Procedures

If you know you’ll need surgery or ongoing treatment, save up in an HSA or emergency fund. This helps you cover costs before insurance starts paying.

Review Your Plan Annually

Healthcare needs change. Review your plan each year during open enrollment to ensure it still fits your situation. Your deductible might be too high—or too low—depending on your health.

Conclusion: Take Control of Your Healthcare Costs

Understanding medical insurance deductibles is one of the most powerful tools you have for managing your healthcare expenses. By knowing what a deductible is, how it works, and how to minimize its impact, you can make informed decisions about your health plan and avoid financial stress.

Whether you’re a freelancer, a new parent, or someone managing chronic health conditions, the key is to stay informed and plan ahead. Compare plans, use in-network providers, take advantage of preventive care, and consider tools like HSAs to help manage costs.

Remember, a deductible isn’t a penalty—it’s a shared responsibility. By understanding it, you’re not just saving money; you’re taking control of your health and your financial future.

Frequently Asked Questions

What is the difference between a deductible and out-of-pocket maximum?

The deductible is the amount you pay before insurance starts covering costs. The out-of-pocket maximum is the most you’ll pay in a year, including deductibles, copays, and coinsurance. Once you hit this limit, your insurance covers 100% of covered services.

Can I use my HSA to pay my deductible?

Yes, if you have a high-deductible health plan and an HSA, you can use HSA funds to pay your deductible tax-free. This makes it easier to manage out-of-pocket costs.

Do prescriptions count toward my deductible?

It depends on your plan. Some plans require you to meet your deductible before covering prescriptions, while others cover certain medications (like generic drugs) after you’ve paid a portion of the deductible.

What happens if I don’t meet my deductible?

If you don’t meet your deductible by the end of the year, you still pay 100% of covered services up to that point. Your plan won’t “roll over” unused deductible amounts.

Can I change my deductible mid-year?

No, deductibles are set for the entire plan year. However, you can switch plans during open enrollment or a qualifying life event, which may change your deductible for the following year.

Are dental and vision covered by my deductible?

Often, yes. Many plans include dental and vision under the same deductible, but some have separate deductibles or coverage limits. Check your plan documents for details.