Medical insurance is more than just a monthly bill—it’s your safety net when health issues strike. Whether you’re self-employed, working for a small business, or part of a large corporation, understanding your medical insurance coverage can save you thousands and reduce stress. This guide breaks down everything from deductibles and premiums to out-of-pocket costs and network providers, giving you the tools to make smarter health decisions.

Key Takeaways

- Medical insurance covers a wide range of services: From doctor visits and prescriptions to emergency care and hospital stays—knowing what’s included helps you avoid surprise bills.

- Understand key terms like premium, deductible, and copay: These define how much you pay and when, so you can budget effectively and avoid confusion.

- Network matters: Staying within your insurance provider’s network typically costs less; going out-of-network can lead to much higher out-of-pocket expenses.

- Preventive care is often free: Many plans cover annual checkups, vaccinations, and screenings at no extra cost, helping you catch issues early.

- Open enrollment is your best chance to change plans: Outside this window, you may only qualify for changes due to major life events like marriage or job loss.

- Compare plans carefully: A plan with low premiums might have high out-of-pocket costs—balance both to find what fits your health needs and budget.

- Keep records and know your rights: Save receipts, review Explanation of Benefits (EOBs), and don’t hesitate to appeal denied claims.

📑 Table of Contents

- Introduction: Why Medical Insurance Coverage Matters More Than Ever

- What Is Medical Insurance Coverage?

- Key Terms You Need to Know

- Types of Medical Insurance Plans

- What Does Medical Insurance Typically Cover?

- How to Choose the Right Medical Insurance Plan

- How to Use Your Medical Insurance Effectively

- Special Considerations for Freelancers and Self-Employed Individuals

- Common Mistakes to Avoid

- Conclusion: Take Control of Your Health and Finances

Introduction: Why Medical Insurance Coverage Matters More Than Ever

Let’s face it—medical bills can be terrifying. One unexpected ER visit can cost thousands, and even routine care can add up. That’s where medical insurance coverage comes in. It’s not just a piece of paper or a monthly payment; it’s peace of mind. Knowing you’re covered when illness or injury strikes can make all the difference between financial ruin and manageable recovery.

Whether you’re a freelancer, a small business owner, or part of a large company, medical insurance is essential. But with so many plans, terms, and options, it’s easy to feel overwhelmed. That’s why this complete guide to medical insurance coverage exists—to cut through the jargon and give you clear, actionable insights. We’ll walk you through how insurance works, what it covers, how to choose the right plan, and how to use it wisely. By the end, you’ll feel confident navigating the healthcare system and making choices that protect both your health and your wallet.

What Is Medical Insurance Coverage?

Medical insurance coverage is a financial agreement between you and an insurance company. In exchange for regular payments called premiums, the insurer agrees to pay all or part of your medical expenses when you get sick or injured. Think of it as a team effort: you pay a portion, and your insurer covers the rest—within certain limits and rules.

Visual guide about Complete Guide to Medical Insurance Coverage

Image source: trucompare.in

How Does It Work?

When you visit a doctor or get treatment, your insurance plan determines how much gets paid and by whom. For example, if you see a primary care physician, your plan might cover 80% of the cost after you meet your deductible. That means you pay 20%, and your insurer pays 80%. The specifics depend on your plan type—like HMO, PPO, or EPO—and whether you’re in or out of network.

Who Needs It?

Everyone does—especially if you rely on regular medical care, take prescription medications, or want protection against high medical bills. Even young, healthy people benefit because accidents and unexpected illnesses can happen to anyone. For freelancers and self-employed individuals, medical insurance isn’t just helpful—it’s often a necessity for financial stability.

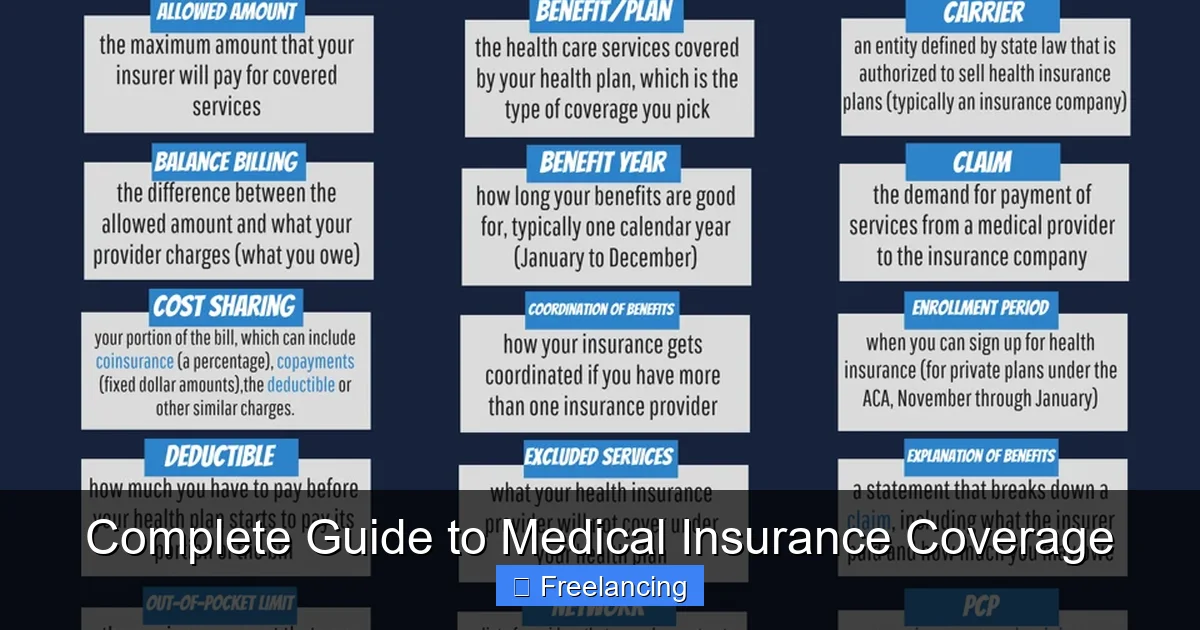

Key Terms You Need to Know

If you’ve ever opened a health insurance form and felt lost, you’re not alone. The language can be confusing. But understanding these core terms will help you compare plans and avoid surprises.

Visual guide about Complete Guide to Medical Insurance Coverage

Image source: velocityglobal.com

Premium

Your premium is the amount you pay regularly—usually monthly—for your insurance. It doesn’t matter if you use your health plan or not; you still pay this amount. Premiums can vary widely based on your age, location, plan type, and whether you’re on an individual or family plan.

Deductible

The deductible is how much you pay out of pocket before your insurance starts covering costs. For example, if your deductible is $1,500, you’ll pay the first $1,500 in medical bills each year. After that, your plan may kick in. Some plans have low deductibles but higher premiums, while others have high deductibles and lower monthly costs.

Copay and Coinsurance

A copay is a fixed amount you pay for a service, like $30 for a doctor’s visit. Coinsurance is a percentage you pay, like 20% of a $200 bill. Most plans use a mix: you pay a copay at the time of service, and after meeting your deductible, you may also pay coinsurance.

Out-of-Pocket Maximum

This is the most you’ll pay in a year for covered services. Once you hit this limit, your insurance covers 100% of additional costs. For 2024, the federal out-of-pocket maximum is $9,450 for individuals and $18,900 for families. This cap protects you from financial disaster.

Network and Out-of-Network

Your plan has a network of doctors, hospitals, and clinics that have agreed to provide care at negotiated rates. Staying in-network usually means lower costs. Going out-of-network can result in higher bills or even full payment, depending on your plan.

Types of Medical Insurance Plans

Not all health insurance plans are created equal. Choosing the right one depends on your health needs, budget, and lifestyle. Here’s a breakdown of the most common types.

Visual guide about Complete Guide to Medical Insurance Coverage

Image source: dartmouth.edu

Health Maintenance Organization (HMO)

HMO plans require you to choose a primary care physician (PCP) and get referrals to see specialists. You must stay within the network for coverage, except in emergencies. HMOs usually have lower premiums and out-of-pocket costs but offer less flexibility in choosing providers.

Preferred Provider Organization (PPO)

PPO plans give you more freedom. You can see any doctor or specialist without a referral, and you can go in-network or out-of-network. Out-of-network care is covered at a reduced rate, but you pay more. PPOs typically have higher premiums but greater flexibility.

Exclusive Provider Organization (EPO)

EPO plans are a middle ground. Like HMOs, you need to stay in-network for coverage, but you don’t need referrals to see specialists. EPOs often have lower premiums than PPOs but less flexibility than HMOs.

High-Deductible Health Plan (HDHP)

HDHPs have lower monthly premiums but higher deductibles. These plans are often paired with a Health Savings Account (HSA), which lets you save money tax-free for medical expenses. HDHPs are ideal for people who are generally healthy and want to save on premiums.

Catastrophic Insurance

Available to people under 30 or those with a hardship exemption, catastrophic plans offer protection against worst-case scenarios. They have very high deductibles but low premiums and cover essential health benefits after the deductible is met.

What Does Medical Insurance Typically Cover?

Under the Affordable Care Act (ACA), all marketplace and most employer-sponsored plans must cover a set of essential health benefits. These include:

- Outpatient care (doctor visits, lab tests)

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use treatment

- Prescription drugs

- Rehabilitative services (like physical therapy)

- Laboratory services

- Preventive care (vaccines, screenings, annual checkups)

Preventive Care: Free and Covered

One of the best benefits of ACA-compliant plans is that preventive services are covered at 100%. That means no copays or deductibles for things like flu shots, blood pressure checks, mammograms, and cancer screenings. This encourages early detection and saves money in the long run.

Prescription Drug Coverage

Most plans include a formulary—a list of covered medications. Tiered pricing means generic drugs are cheaper than brand-name drugs, which are cheaper than specialty drugs. If a drug isn’t on the formulary, you may need to request a prior authorization or pay full price.

Mental Health and Substance Use

Modern insurance plans must cover mental health services equally to physical health care. That includes therapy, counseling, and treatment for substance use disorders. Many plans now offer telehealth options for mental health visits, making care more accessible.

How to Choose the Right Medical Insurance Plan

With so many options, choosing a plan can feel like a full-time job. But with the right approach, you can find a plan that fits your needs.

Assess Your Health Needs

Ask yourself: Do you have chronic conditions like diabetes or asthma? Do you take regular medications? Do you see specialists often? If so, a plan with lower out-of-pocket costs and in-network specialists might be worth the higher premium. If you’re healthy and rarely visit the doctor, a high-deductible plan with an HSA could save you money.

Compare Costs

Look beyond the premium. Consider the deductible, copays, coinsurance, and out-of-pocket maximum. A plan with a $100 monthly premium and $5,000 deductible may seem cheap, but it could cost you $10,000 in the first year if you get sick. Use online plan comparison tools to see total estimated costs.

Check the Provider Network

Make sure your doctors, specialists, and hospitals are in-network. Even if a plan looks great on paper, it’s not useful if your regular doctor isn’t covered. Use your insurer’s directory to verify coverage.

Consider Telehealth

Many plans now offer virtual doctor visits. These can save time and money, especially for minor issues like colds, rashes, or follow-up appointments. Check if telehealth is included and how it works.

Look at Prescription Coverage

If you take medications regularly, compare formularies and copays across plans. A small difference in drug costs can add up over time.

Evaluate Customer Service

Read reviews or ask friends about the insurer’s customer service. If you have questions or need help with a claim, you want a company that’s responsive and helpful.

How to Use Your Medical Insurance Effectively

Having insurance is one thing—using it wisely is another. Here’s how to get the most value from your coverage.

Always Use In-Network Providers

Even if a specialist is highly recommended, check if they’re in-network. Out-of-network care can cost 2–3 times more. When in doubt, call your insurer’s customer service line.

Know When to Go to the ER

Emergency rooms are expensive, but they’re covered if it’s a true emergency. For non-urgent issues, consider urgent care or telehealth instead.

Use Preventive Services

Schedule your annual checkups and screenings. These are free under most plans and can catch problems early—before they become costly.

Keep Records

Save receipts for medical expenses, especially if you have an HDHP and want to contribute to an HSA. Also, review your Explanation of Benefits (EOB) statements each month to catch errors.

Appeal Denied Claims

If your claim is denied, don’t give up. You have the right to appeal. Contact your insurer with supporting documents and ask for a review.

Shop Around for Procedures

For elective procedures, ask about facility fees. Some hospitals charge more than others for the same service. Comparing costs can save hundreds or thousands.

Special Considerations for Freelancers and Self-Employed Individuals

As a freelancer, you don’t have the same benefits as employees. That means you’re responsible for your own medical insurance. But there are ways to make it affordable and manageable.

Explore the Health Insurance Marketplace

Freelancers can shop on the Health Insurance Marketplace (Healthcare.gov) during open enrollment. Depending on your income, you may qualify for subsidies that lower your premium. You can also enroll during special enrollment periods if you experience a qualifying life event, like losing other coverage.

Consider a Health Sharing Ministry

Health sharing ministries are alternatives to traditional insurance. Members share medical costs based on religious or philosophical beliefs. They’re not insurance and don’t comply with ACA requirements, but they can be cheaper for some people.

Use an HSA if You Have an HDHP

If you choose a high-deductible plan, pair it with a Health Savings Account. You can contribute up to $4,150 (2024) for individuals and $8,300 for families. Funds roll over year to year and can be used for qualified medical expenses tax-free.

Plan for Tax Deductions

Self-employed individuals can deduct health insurance premiums as a business expense. This can reduce your taxable income and lower your overall tax bill.

Group Plans and Associations

Some professional associations offer group health plans to members. These can be more affordable than individual plans and may include dental and vision.

Stay Informed About Changes

Healthcare laws and subsidies change. Subscribe to newsletters from Healthcare.gov or a trusted advisor to stay updated on open enrollment dates and new options.

Common Mistakes to Avoid

Even experienced users make mistakes with medical insurance. Here are some pitfalls to avoid.

Not Reviewing Your Plan Annually

Your health and finances change. What worked last year might not work now. Review your plan every fall during open enrollment.

Ignoring the Fine Print

Read your Summary of Benefits and Coverage (SBC). It explains what’s covered, costs, and limitations. Don’t rely on ads or summaries alone.

Skipping Preventive Care

Even if you feel fine, preventive services are free and important. Skipping them can lead to undetected conditions.

Using Out-of-Network Services Without Checking

Always verify network status before scheduling care. A quick phone call can save you hundreds.

Not Using Telehealth

Virtual visits are convenient and often cheaper. Use them for minor issues to save time and money.

Forgetting to Update Life Changes

Married, had a baby, moved? These events trigger special enrollment periods. Don’t miss your chance to change plans.

Conclusion: Take Control of Your Health and Finances

Medical insurance coverage is more than a safety net—it’s a strategic tool for protecting your health and financial future. By understanding how it works, what it covers, and how to choose and use the right plan, you can avoid surprises and make informed decisions. Whether you’re a freelancer navigating the marketplace or someone looking to switch employers, the principles remain the same: know your options, compare carefully, and use your benefits wisely.

Remember, the best plan isn’t always the cheapest or the most expensive—it’s the one that fits your health needs, budget, and lifestyle. Take time this open enrollment season to review your options. Talk to a broker if needed, use online tools to compare plans, and don’t hesitate to ask questions. With the right knowledge, you can walk into 2025 with confidence, knowing you’re covered when it matters most.

Frequently Asked Questions

What is the difference between in-network and out-of-network care?

Network refers to doctors and hospitals that have agreed to provide care at negotiated rates with your insurer. In-network care is typically much cheaper, while out-of-network care can result in higher bills or even full payment, depending on your plan.

Can I change my medical insurance plan outside of open enrollment?

Generally, no—but you may qualify for a special enrollment period if you experience a life event like getting married, having a baby, losing other coverage, or moving to a new state. Check Healthcare.gov for details.

What is a Health Savings Account (HSA)?

An HSA is a tax-advantaged account available with high-deductible health plans. You can contribute pre-tax dollars to pay for qualified medical expenses, and funds roll over year to year. It’s a powerful tool for saving on healthcare.

Are mental health services covered by medical insurance?

Yes, under the Affordable Care Act, mental health and substance use disorder services must be covered at the same level as physical health care. This includes therapy, counseling, and inpatient treatment.

How do I find out if my doctor is in-network?

Visit your insurer’s website and use their provider directory. You can search by name, specialty, or location. If you can’t find them, call your insurer’s customer service line for confirmation.

What should I do if my insurance claim is denied?

First, review the Explanation of Benefits (EOB) to understand why. Then, contact your insurer to request a review. You have the right to appeal the decision, and many claims are overturned during the appeals process.