Cut your medical insurance costs without sacrificing coverage. By comparing plans, raising deductibles, and using HSAs, you can save hundreds—even thousands—of dollars annually. This guide walks you through practical steps to lower premiums while keeping healthcare affordable and accessible.

Key Takeaways

- Understanding How to Save Money on Medical Insurance Premiums: Provides essential knowledge

📑 Table of Contents

- How to Save Money on Medical Insurance Premiums

- Understanding Your Insurance Options

- Choose the Right Plan for Your Lifestyle

- Maximize Your Health Savings Account (HSA)

- Shop During Open Enrollment and Special Enrollment Periods

- Take Advantage of Preventive Care

- Consider Alternative Coverage Options

- Optimize Your Coverage Year-Round

- Conclusion: Save Smart, Stay Healthy

How to Save Money on Medical Insurance Premiums

Let’s face it—health insurance is expensive. Whether you’re shopping for yourself, your family, or your employees, medical insurance premiums can eat up a big chunk of your budget. But here’s the good news: you don’t have to pay full price every month. With a little know-how and some smart planning, you can significantly reduce what you spend on health insurance—without losing the coverage you need.

In this article, we’ll walk through practical, real-world strategies to help you save money on medical insurance premiums. From understanding your plan options to leveraging tax-advantaged accounts, we’ve got you covered. Whether you’re young and healthy, a family with kids, or managing a small business, these tips apply across the board. Let’s dive in.

Understanding Your Insurance Options

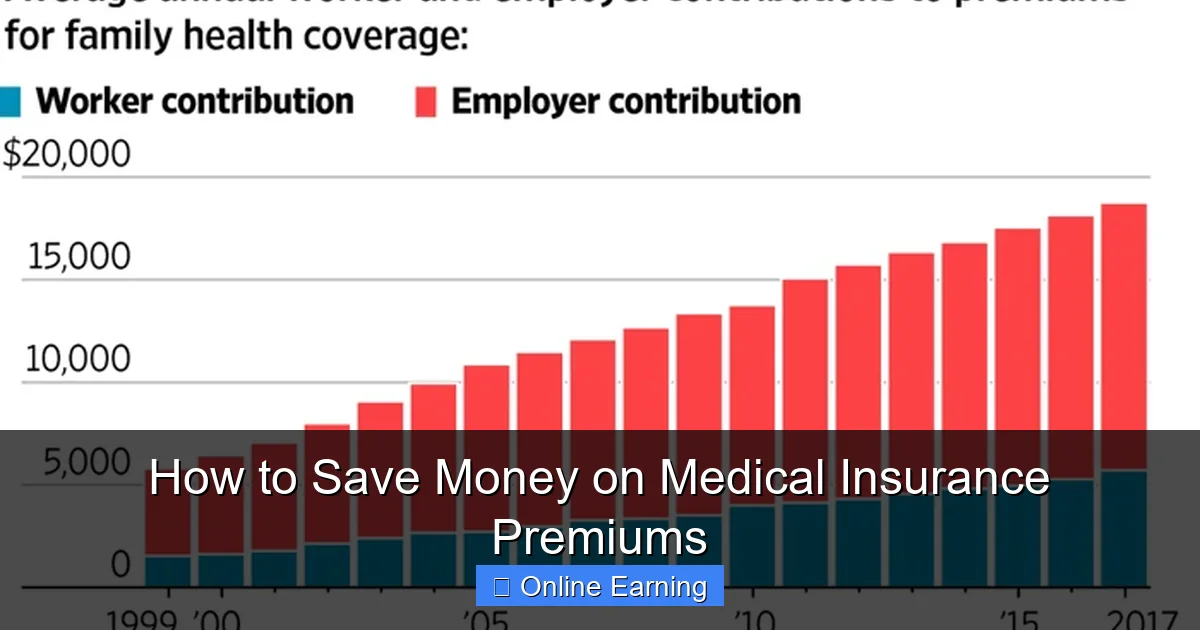

Before you can save money, you need to understand how medical insurance works. Most plans fall into one of two categories: HMOs (Health Maintenance Organizations) and PPOs (Preferred Provider Organizations). HMOs usually have lower premiums but require you to see doctors within a specific network and get referrals for specialists. PPOs offer more flexibility—you can see out-of-network providers at a higher cost—but often come with higher monthly premiums.

Visual guide about How to Save Money on Medical Insurance Premiums

Image source: debt.org

What Are Premiums, Deductibles, and Out-of-Pocket Maximums?

Three key terms you’ll hear a lot: premiums, deductibles, and out-of-pocket maximums. Your premium is what you pay monthly to keep your plan active. The deductible is the amount you pay before insurance kicks in. And the out-of-pocket maximum is the most you’ll pay in a year, after which insurance covers 100%.

For example, if your premium is $300/month, your deductible is $2,000, and your out-of-pocket max is $5,000, you’ll pay $3,600 annually just in premiums. If you don’t visit the doctor much, a plan with a higher deductible and lower premium might save you money. But if you have chronic conditions or frequent medical needs, a lower deductible plan may be worth the extra cost.

How to Compare Plans Like a Pro

Use tools like Healthcare.gov (for individual plans) or your employer’s benefits portal to compare options. Look at:

- Monthly premium

- Deductible

- Co-pays and co-insurance rates

- Network size

- Prescription drug coverage

- Wellness programs and preventive care benefits

Don’t just pick the cheapest plan. Ask yourself: How often do I see the doctor? Do I take regular medications? Am I okay with paying more upfront in exchange for lower monthly payments?

Choose the Right Plan for Your Lifestyle

One of the best ways to save on medical insurance premiums is to pick a plan that matches your health habits and budget. There’s no one-size-fits-all answer, but here’s how to decide.

Visual guide about How to Save Money on Medical Insurance Premiums

Image source: assets.nst.com.my

Healthy and Low-Risk Individuals

If you’re young, generally healthy, and rarely visit the doctor, a high-deductible health plan (HDHP) paired with a Health Savings Account (HSA) is often the smartest choice. These plans have low monthly premiums—sometimes under $200—and let you build tax-free savings for future medical expenses.

For example, Sarah, a 28-year-old graphic designer, pays $180/month for an HDHP with a $3,000 deductible. She contributes $200/month to her HSA, which grows tax-free. Over five years, she’s saved $10,800 in premiums alone and has $12,000 in tax-free savings for emergencies.

Families with Ongoing Medical Needs

If you have children, a chronic condition, or take regular medications, a plan with a lower deductible and higher premium might make more financial sense. Look for plans with low co-pays for doctor visits and strong prescription coverage.

Also, consider family dental and vision add-ons. Some insurers bundle these into one plan, which can save you money compared to buying them separately.

Small Business Owners

As a small business owner, you can offer employees a choice of plans and share premium costs. Offering an HDHP with an HSA can reduce your monthly expenses while giving employees tax advantages. Plus, you may qualify for the Small Business Health Care Tax Credit if you have 25 or fewer full-time workers and pay at least 50% of their premiums.

Maximize Your Health Savings Account (HSA)

If you have a high-deductible health plan, you’re eligible for an HSA—and it’s one of the best tools for saving money on medical expenses.

Visual guide about How to Save Money on Medical Insurance Premiums

Image source: mymoneyblog.com

Why HSAs Are a Triple Threat

HSAs offer three major tax benefits:

- Tax-deductible contributions—you reduce your taxable income when you contribute.

- Tax-free growth—your money grows without being taxed.

- Tax-free withdrawals—you can use the funds for qualified medical expenses at any time.

For 2024, the HSA contribution limit is $4,150 for individuals and $8,300 for families. If you’re 55 or older, you can add an extra $1,000 as a catch-up contribution.

Example: Mark, 42, contributes $350/month to his HSA. After 10 years at 6% annual growth, his account is worth over $60,000—all tax-free and ready for medical bills, retirement, or even long-term care.

How to Use Your HSA Wisely

- Pay for qualified medical expenses immediately—don’t wait until tax season.

- Use it for dental, vision, and hearing aids.

- Invest the funds if your provider allows—long-term growth can turn $50/month into $100,000+.

- Keep receipts in case the IRS asks for proof of use.

Shop During Open Enrollment and Special Enrollment Periods

Health insurance prices and plans change every year. The best time to shop for cheaper options is during open enrollment (usually November–December). But life events—like getting married, having a baby, or losing job-based coverage—can trigger a special enrollment period, giving you a chance to switch plans outside the usual window.

How to Find the Best Deals

Use comparison tools like:

- Healthcare.gov

- Your state’s health insurance marketplace

- Private brokers or online insurance aggregators

Enter your age, location, income, and health status. The tool will show you all available plans and estimate your costs. Don’t forget to factor in subsidies—if you earn between 100% and 400% of the federal poverty level, you may qualify for premium tax credits.

Example: Using Subsidies to Save Big

Maria, a single mother earning $28,000/year, qualifies for a $200/month premium tax credit. Without it, her plan would cost $550/month. With the credit, she only pays $350. Over a year, that’s $2,400 in savings—enough to cover her daughter’s orthodontic work.

Take Advantage of Preventive Care

Most health plans cover preventive care at no cost—including annual checkups, vaccinations, cancer screenings, and wellness exams. Use these services regularly to catch problems early and avoid expensive treatments later.

What’s Covered Under Preventive Care?

- Blood pressure and cholesterol checks

- Diabetes screening

- Mammograms and colonoscopies (based on age and risk)

- Smoking cessation programs

- Contraception and family planning

By staying on top of your health, you reduce the chance of needing costly emergency care or long-term treatments. That means your insurance stays affordable—and so does your wallet.

Consider Alternative Coverage Options

Traditional employer or marketplace insurance isn’t the only way to get coverage. Depending on your situation, other options might save you money.

Health Care Sharing Ministries

These are faith-based organizations where members share medical costs. Premiums are often lower than traditional insurance, and there’s no deductible. However, they’re not insurance—and may not cover pre-existing conditions or certain services like mental health or maternity care.

They’re best for people who are comfortable with shared responsibility and don’t need comprehensive coverage.

Catastrophic Plans

Available to people under 30 or those with a hardship exemption, catastrophic plans have very low premiums and high deductibles. They’re designed to protect against worst-case scenarios—like a major illness or injury—while letting you pay for routine care out of pocket.

Medicaid and CHIP

If your income is low, you may qualify for Medicaid or the Children’s Health Insurance Program (CHIP). These programs offer free or low-cost coverage with minimal or no premiums. Check your state’s eligibility rules—coverage varies by location.

Optimize Your Coverage Year-Round

Once you’ve picked a plan, don’t forget to review it regularly. Life changes—new job, kids, retirement—mean your insurance needs may change too.

Tips for Ongoing Savings

- Track your medical spending—keep a log of co-pays, prescriptions, and deductible payments.

- Use in-network providers—out-of-network care can double or triple your costs.

- Ask about payment plans—hospitals often offer discounts if you pay bills over time.

- Negotiate medical bills—many hospitals will reduce charges if you ask.

- Use telehealth—many plans cover virtual visits at low or no cost, avoiding ER visits or urgent care fees.

Conclusion: Save Smart, Stay Healthy

Cutting your medical insurance premiums doesn’t mean cutting corners on care. With the right strategy—comparing plans, choosing the right deductible, using HSAs, and taking advantage of preventive services—you can keep more money in your pocket while staying protected.

Remember, the goal isn’t to pay the least possible—it’s to pay the smartest amount for your lifestyle. Whether you’re a young adult, a growing family, or a small business owner, there are real ways to lower your monthly bills without sacrificing quality care.

Start today. Review your current plan. Explore your options. And take control of your health—and your wallet.

Frequently Asked Questions

Can I save money by switching to a high-deductible plan?

Yes, if you’re generally healthy and don’t visit the doctor often. High-deductible plans (HDHPs) have lower monthly premiums and can be paired with an HSA for tax-free savings. Just make sure you can afford the deductible if you need care.

How much can I really save on medical insurance premiums?

It varies, but many people save $200–$500+ per month by switching to a lower-premium plan or qualifying for subsidies. Over a year, that’s $2,400 to $6,000 in savings—not counting HSA growth.

Are HSAs worth it even if I don’t use them right away?

Absolutely. Even if you don’t need medical care now, HSAs offer triple tax benefits and let your money grow. Many people use them in retirement for qualified medical expenses.

Can I get cheaper insurance if I’m self-employed?

Yes. Self-employed individuals can shop on Healthcare.gov, deduct premiums on taxes, and offer their own HSA. Some also qualify for the Small Business Health Care Tax Credit.

What if I lose my job-based insurance?

You may qualify for a special enrollment period to buy a plan on the marketplace. You might also be eligible for COBRA (expensive), Medicaid, or a subsidy if your income dropped.

Should I always pick the cheapest plan?

Not necessarily. The cheapest plan may have a high deductible and leave you paying out of pocket for care. Balance premium cost with your expected medical needs to find the best value.