Buying medical insurance online is faster, smarter, and more affordable than ever. With just a few clicks, you can compare plans, get instant quotes, and enroll in coverage that fits your budget and needs. Online platforms make health insurance accessible to everyone—no paperwork, no delays.

Key Takeaways

- Speed & Convenience: Get quotes and enroll in minutes using user-friendly online portals.

- Wide Plan Selection: Compare multiple insurers and coverage options from one platform.

- Cost Savings: Access exclusive discounts, subsidies, and lower premiums through digital marketplaces.

- Transparency: Read real user reviews, coverage details, and exclusions before purchasing.

- Customer Support: Most platforms offer live chat, phone support, and 24/7 assistance.

- Mobile Access: Manage your policy, file claims, and renew coverage on the go via mobile apps.

- Eligibility Tools: Use online calculators to find plans based on age, income, and health status.

📑 Table of Contents

- Online Platforms to Buy Medical Insurance Fast

- Why Buy Medical Insurance Online?

- Top Online Platforms to Buy Medical Insurance Fast

- How to Choose the Right Platform

- Tips for a Smooth Online Insurance Purchase

- Common Mistakes to Avoid

- Real-Life Example: Sarah’s Journey

- Future of Online Medical Insurance

- Conclusion

Online Platforms to Buy Medical Insurance Fast

Let’s face it—healthcare can be expensive, and the last thing you want is to be stuck without coverage when you need it most. Whether you’re self-employed, switching jobs, moving to a new city, or just want to simplify your benefits, buying medical insurance doesn’t have to be a hassle. In fact, with the rise of digital platforms, getting the right health plan is faster, easier, and often more affordable than ever before.

Today, millions of people are turning to online insurance marketplaces to compare plans, read real reviews, and enroll in coverage—all from the comfort of their homes. These platforms act like travel sites for health insurance: you input your details, see your options side by side, and choose the plan that fits your lifestyle. No more calling agents, waiting on hold, or filling out endless forms. Just smart, efficient, and transparent shopping.

In this guide, we’ll walk you through the best online platforms to buy medical insurance fast, how they work, what to look for, and how to make the most of your digital insurance-buying journey. Whether you’re a first-time buyer or switching plans, this article will help you navigate the digital insurance landscape with confidence.

Why Buy Medical Insurance Online?

Before diving into specific platforms, it’s important to understand why going digital is such a game-changer. Traditional insurance shopping often involves visiting agents, attending in-person meetings, or calling multiple offices—each time losing precious time. Online platforms eliminate these barriers by centralizing information and simplifying the process.

Visual guide about Online Platforms to Buy Medical Insurance Fast

Image source: images.surferseo.art

Time-Saving Efficiency

One of the biggest advantages of online insurance platforms is speed. Instead of spending hours on the phone or in meetings, you can get a full quote in under 10 minutes. Just enter your age, location, income, and health status, and the platform instantly matches you with suitable plans.

For example, if you’re a 32-year-old freelance designer in Austin, Texas, you can input your details into a platform like Healthcare.gov or Zuellig Wellness, and within minutes, see three to five plans tailored to your needs. No back-and-forth. No guesswork.

Transparency and Comparison

Online platforms shine when it comes to comparison. You can view premiums, deductibles, co-pays, network doctors, prescription coverage, and even customer satisfaction scores—all in one place. This level of transparency helps you avoid hidden fees or misleading sales pitches.

Imagine comparing two plans side by side: Plan A has a $200/month premium with a $1,000 deductible, while Plan B costs $250/month but covers 80% of preventive care with no deductible. The decision becomes clear—and easy.

Access to Subsidies and Discounts

Many online platforms help you qualify for government subsidies or employer discounts you might not know about. For instance, if you earn less than 400% of the federal poverty level, you may be eligible for reduced premiums through the Affordable Care Act (ACA) marketplace.

Platforms like Covered California or HealthSherpa automatically calculate your eligibility and show you how much you can save. This can mean hundreds or even thousands of dollars in annual savings.

Top Online Platforms to Buy Medical Insurance Fast

Now that you understand the benefits, let’s explore the leading digital platforms where you can buy medical insurance quickly and securely. Each offers unique features, so we’ve highlighted what makes them stand out.

Visual guide about Online Platforms to Buy Medical Insurance Fast

Image source: is1-ssl.mzstatic.com

1. Healthcare.gov

If you’re in the United States and looking for health insurance through the Affordable Care Act (ACA), Healthcare.gov is the official government portal. It’s the one-stop shop for open enrollment, special enrollment periods, and subsidy applications.

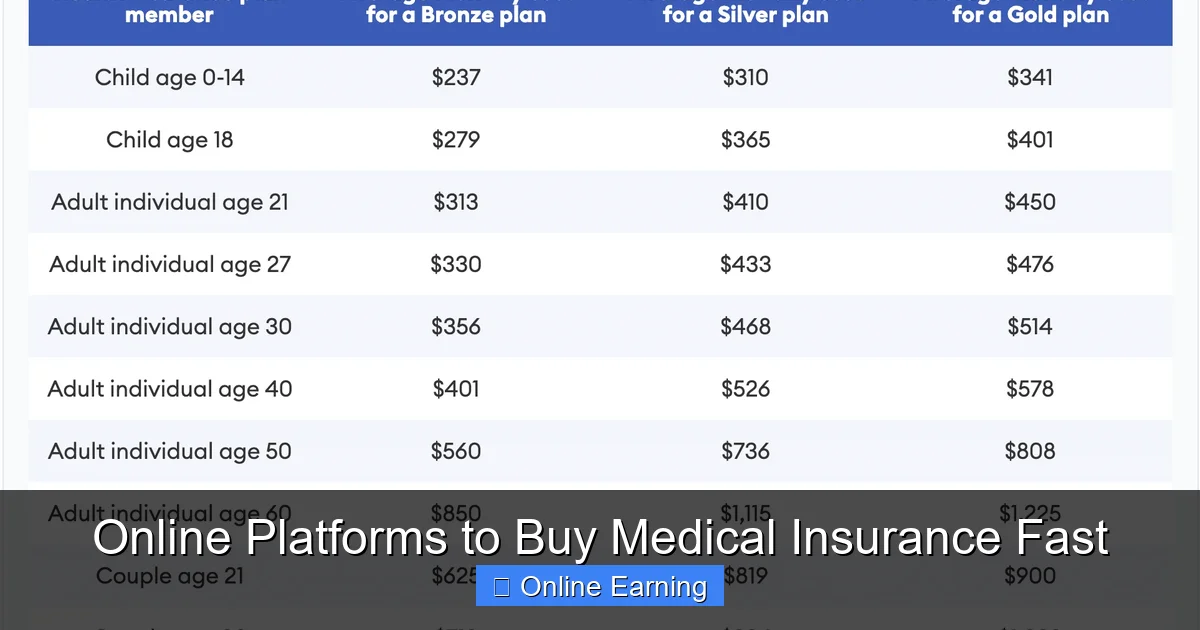

How it works: Visit healthcare.gov, create an account, answer a few health and income questions, and browse plans from over 20 insurers. You can compare coverage levels—Bronze, Silver, Gold, and Platinum—and see how much you’ll pay out-of-pocket.

Pro Tip: Use the “Savings Calculator” to estimate your premium tax credit. If you qualify, your monthly payment could drop significantly.

2. Covered California

For residents of California, Covered California is the state-run marketplace. It’s known for its robust customer support and wide range of plans, including Covered California Silver 94, which offers extra savings for low-income individuals.

This platform is especially helpful if you’re eligible for Medi-Cal or need help with enrollment during life changes like marriage or job loss. Covered California also offers in-person assistance through Navigators and Certified Enrollment Counselors.

3. HealthSherpa

HealthSherpa is a private, independent platform that aggregates plans from multiple insurers across the U.S. Unlike government sites, HealthSherpa partners with brokers and agencies to offer personalized support.

It’s ideal if you want human guidance but still prefer the speed of online shopping. You can chat with a licensed agent during the process, and they’ll help you choose the best plan based on your health needs and budget.

4. eHealth

eHealth has been around since 1997 and is one of the oldest online insurance marketplaces. It offers free, unbiased quotes from over 200 carriers and provides tools like the “Plan Finder” to match you with the right coverage.

What sets eHealth apart is its extensive customer reviews and educational resources. You’ll find articles, videos, and FAQs that walk you through every step of the process.

5. Policygenius

While Policygenius focuses on life, auto, and home insurance, it also offers health insurance through partnerships with top insurers. It’s perfect if you want a one-stop shop for all your insurance needs.

The platform uses AI-powered tools to recommend plans based on your lifestyle. For example, if you travel frequently, it might suggest a plan with nationwide emergency care coverage.

6. Zynx Health (via Partner Platforms)

While Zynx Health is primarily a clinical decision support tool, it’s often integrated into larger health tech platforms that offer insurance enrollment. These systems help healthcare providers recommend insurance plans to patients based on their medical history.

This is especially useful for individuals with chronic conditions who need specialized care. The platform can suggest plans with lower co-pays for specialists or prescription drugs.

How to Choose the Right Platform

With so many options, how do you pick the right one? Here’s a step-by-step guide to help you make an informed decision.

Visual guide about Online Platforms to Buy Medical Insurance Fast

Image source: image6.slideserve.com

Step 1: Determine Your Needs

Start by asking yourself: What’s your budget? Do you need dental or vision coverage? Are you on medication? Do you see a specialist regularly? Answering these questions will narrow down your options.

For example, if you’re on insulin, look for plans with low co-pays for diabetes drugs. If you’re expecting a baby, consider maternity coverage.

Step 2: Check Eligibility

Most platforms ask about your age, income, residency, and family size. This helps them determine if you qualify for subsidies or Medicaid.

For instance, if you’re a 28-year-old earning $30,000 a year, you might qualify for a Silver plan with a $200/month premium after subsidies.

Step 3: Compare Coverage Levels

The ACA defines four metal levels of coverage:

- Bronze: Lowest premium, highest out-of-pocket costs. Best for healthy individuals who rarely visit the doctor.

- Silver: Moderate premium and costs. Ideal if you expect to use healthcare services and qualify for cost-sharing reductions.

- Gold: Higher premium, lower out-of-pocket expenses. Great for those with ongoing medical needs.

- Platinum: Highest premium, lowest out-of-pocket costs. Best for frequent users of healthcare.

Use the platform’s comparison tool to see how each plan performs in your area.

Step 4: Read the Fine Print

Don’t skip the exclusions and limitations. Some plans don’t cover mental health, fertility treatments, or alternative medicine. Others have waiting periods for pre-existing conditions.

Look for plans with no waiting periods and broad coverage. If you have a history of asthma, for example, ensure the plan covers inhalers and specialist visits.

Step 5: Use Customer Support

If you’re confused, don’t hesitate to reach out. Most platforms offer live chat, phone support, or email assistance. Ask questions like:

- “Will my current doctor be in-network?”

- “How much will my prescriptions cost?”

- “What’s the process for filing a claim?”

Good platforms make support easy and accessible.

Tips for a Smooth Online Insurance Purchase

Even the best platforms can be confusing if you’re not prepared. Here are some pro tips to make your experience seamless.

1. Gather Your Documents

Before you start, collect these essentials:

- Social Security number

- Employer and income information

- Current health insurance policy (if any)

- Bank account details (for premium payments)

- List of medications and doctors

This saves time and ensures accuracy.

2. Enroll During Open or Special Enrollment

Healthcare.gov and most state marketplaces only allow enrollment during specific periods:

- Open Enrollment: Typically November 1 – January 31

- Special Enrollment: Triggered by life events like marriage, birth, or job loss

Missing open enrollment means you’ll likely wait until the next cycle unless you qualify for a special period.

3. Use the Subsidy Calculator

All major platforms have a subsidy estimator. Run the numbers before choosing a plan. You might be surprised how much you can save.

For example, a Silver plan costing $400/month could drop to $150/month with a premium tax credit.

4. Double-Check Network Doctors

Even if a plan looks great, make sure your regular doctor and hospital are in-network. Out-of-network care can double or triple your costs.

Most platforms let you search the provider directory by name or ZIP code.

5. Set Up Auto-Pay

Avoid late fees by setting up automatic payments. Most platforms allow you to link a bank account or credit card.

You’ll get email reminders before your payment is due, so you’re never caught off guard.

6. Review Annually

Healthcare needs change. Review your plan every year during open enrollment. Your income, family size, or health status may have changed, affecting your eligibility for subsidies or preferred plans.

Common Mistakes to Avoid

Even with the best platforms, mistakes happen. Here’s how to avoid them.

Mistake 1: Skipping the Subsidy Check

Many people don’t realize they qualify for help. Always use the subsidy calculator before choosing a plan.

Mistake 2: Choosing Based on Premium Only

A low premium doesn’t mean low costs. A $100/month plan with a $6,000 deductible could cost you $7,000 out of pocket if you get sick.

Look at the total cost of care, not just the monthly price.

Mistake 3: Not Checking the Provider Network

You might love a plan, but if your doctor isn’t in-network, it’s not worth it. Use the platform’s provider search tool.

Mistake 4: Forgetting to Update Life Changes

Marriage, divorce, birth, or job change can trigger a special enrollment period. Don’t wait—update your status to avoid coverage gaps.

Mistake 5: Ignoring Customer Reviews

Platforms like HealthSherpa and eHealth show user ratings. If a plan has 1-star reviews mentioning claim denials, consider alternatives.

Real-Life Example: Sarah’s Journey

Let’s meet Sarah, a 34-year-old graphic designer who recently moved to Denver, Colorado. She was uninsured and needed coverage fast due to a family history of diabetes.

She visited HealthSherpa and entered her details: age 34, income $45,000, two dependents. The platform showed her three Silver plans with subsidies. One plan had a $250/month premium, $1,500 deductible, and covered diabetes screenings and insulin at 90%.

Sarah chose that plan and enrolled in 12 minutes. She saved $200/month thanks to a premium tax credit. Now, she uses the mobile app to track claims and renew her policy each year.

Her story shows how fast and effective online insurance shopping can be—when you know what to look for.

Future of Online Medical Insurance

The digital insurance market is evolving rapidly. Here’s what to expect in the coming years:

- AI-Powered Recommendations: Platforms will use machine learning to suggest plans based on your health data and spending patterns.

- Integration with Wearables: Devices like Apple Watch or Fitbit may influence premium discounts for healthy behaviors.

- Blockchain for Claims: Faster, fraud-proof processing of medical claims through secure digital ledgers.

- Virtual Health Assistants: Chatbots that answer insurance questions 24/7 and help with enrollment.

These innovations will make insurance even more personalized and efficient.

Conclusion

Buying medical insurance doesn’t have to be stressful or time-consuming. With the right online platform, you can compare plans, save money, and get coverage in minutes. Whether you use Healthcare.gov, Covered California, HealthSherpa, or another trusted site, the key is to be informed, prepared, and proactive.

Remember: your health is your wealth. A good insurance plan protects you from financial ruin during medical emergencies. And thanks to digital tools, getting that protection has never been easier.

So take the first step today. Visit a reputable online platform, gather your documents, and start comparing. In just 10 minutes, you could be covered—and in control of your health future.

Frequently Asked Questions

Can I buy medical insurance online in minutes?

Yes! Most online platforms allow you to get quotes and enroll in coverage in under 10 minutes. Just enter your details, compare plans, and complete enrollment digitally.

Are online insurance platforms safe?

Absolutely. Reputable platforms like Healthcare.gov, Covered California, and HealthSherpa use bank-level encryption and follow strict privacy laws to protect your personal and financial data.

Do I need to provide medical history when buying online?

For ACA-compliant plans, you can’t be denied coverage or charged more based on pre-existing conditions. However, you’ll answer basic health questions to determine eligibility for special enrollment.

Can I change my plan after enrolling?

You can only change plans during open enrollment or if you have a qualifying life event (like marriage or job loss) that triggers a special enrollment period.

What if I can’t afford a premium?

You may qualify for subsidies through the ACA marketplace. Use the subsidy calculator on platforms like Healthcare.gov or Covered California to see how much you can save.

Can I manage my policy online after purchase?

Yes! Most platforms offer mobile apps and web portals where you can view coverage, pay bills, file claims, and update personal information—all from your phone or computer.